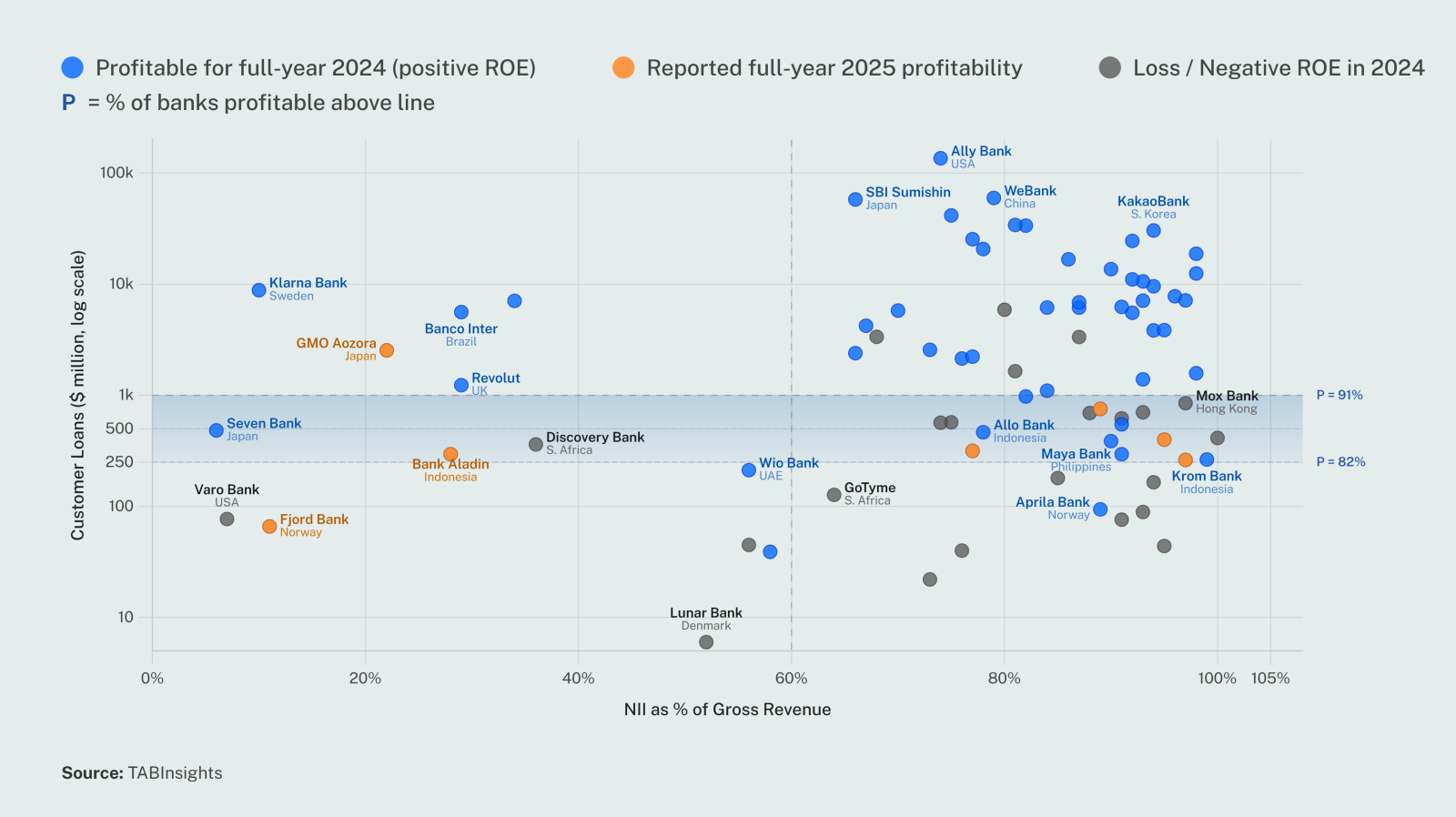

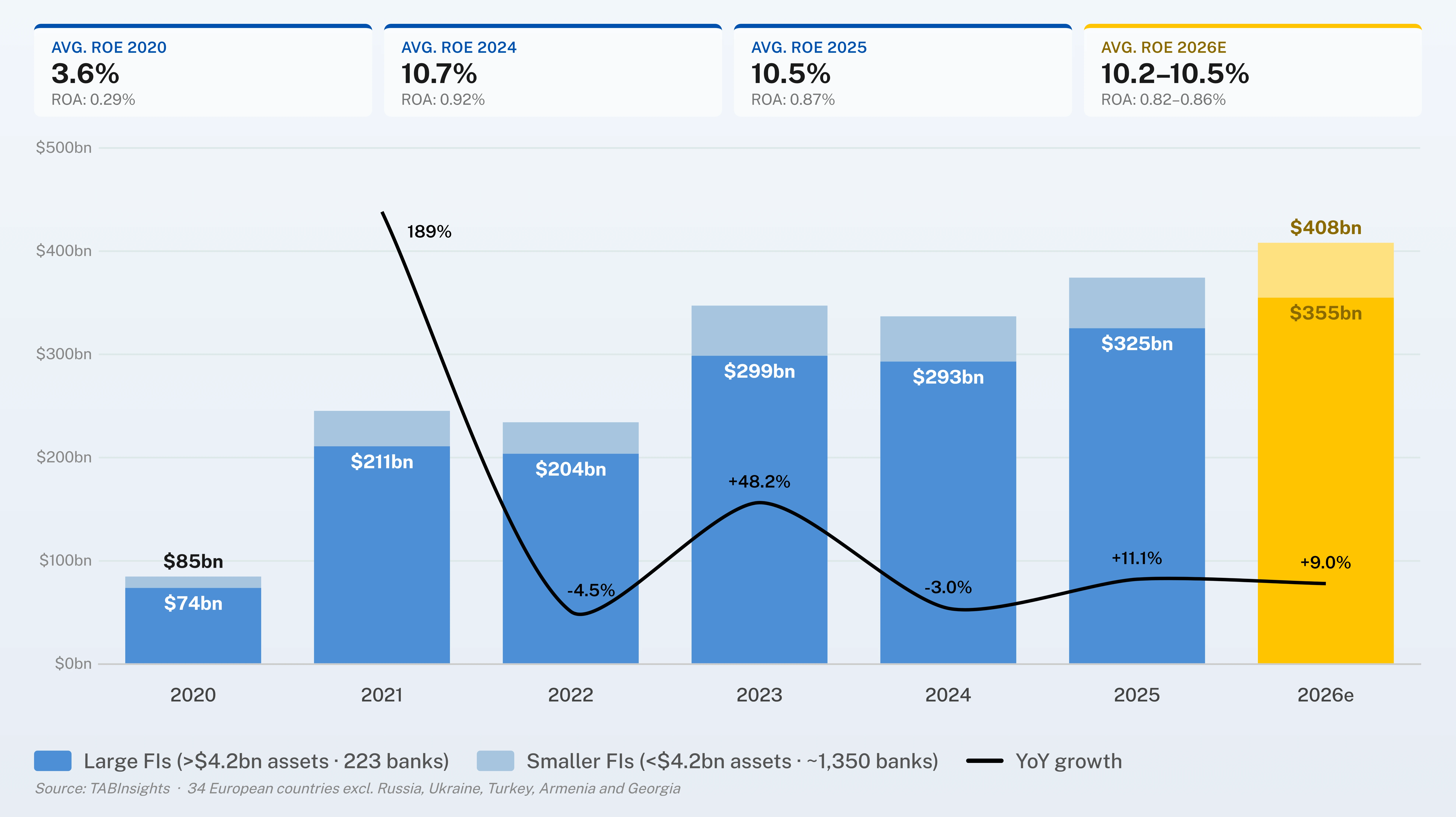

.png)

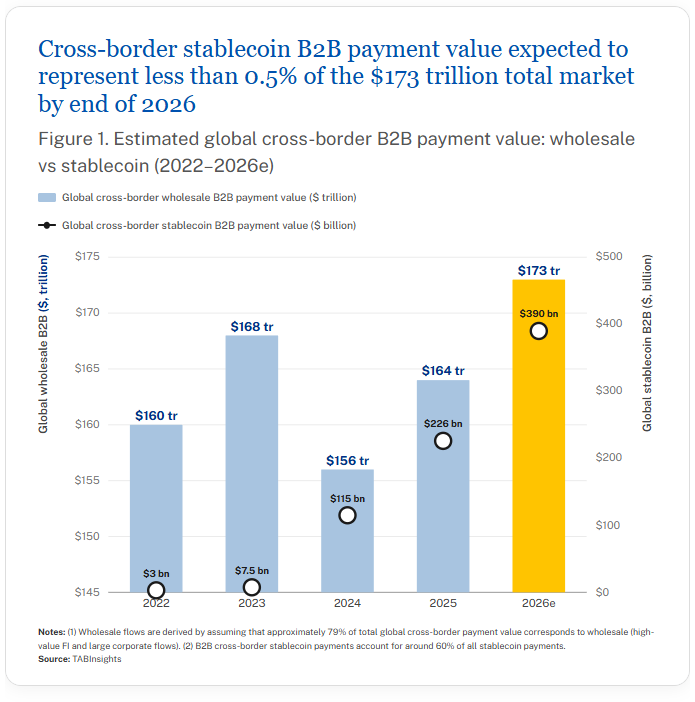

Global B2B cross-border payment volumes are on track to reach $173?trillion in 2026, driven by real-time payment networks, stablecoin infrastructure, and AI-powered routing engines. Even a modest 1% margin compression across just 20% of those flows implies roughly $346?billion in annual revenue shifting away from legacy systems, highlighting the financial stakes of this transition.

The gradual erosion of correspondent banking's dominance is playing out through a new generation of specialist platforms. Thunes routes payments across more than 140 countries via mobile wallet infrastructure, while BVNK processed an annualised $30 billion in stablecoin volumes through 2025. Airwallex, positioning itself as a full-stack financial platform for internationally expanding businesses, rounds out a cohort offering near-real-time settlement and more efficient cost structures than Swift-based chains.

J.P. Morgan’s 2026 Payments Outlook highlights a dual reality: while 60% of Fortune 500 companies plan blockchain-based payment initiatives, nearly 60% still rely on partially automated treasury operations. The key question for banks is no longer if correspondent banking revenue will erode, but which losses can be mitigated by adopting new rails, and which are structurally unavoidable.

B2B stablecoin settlement has crossed the experiment threshold, but remains below 0.5% of global cross-border wholesale payments

The industry estimates that B2B stablecoin payments will reach around $390 billion in 2026, up from $3 billion in 2022. Yet that figure represents under 0.5% of the $173 trillion total market by end of 2026. BVNK, an enterprise-grade payments infrastructure platform for stablecoins disclosed that its annualised stablecoin payment volume reached $30 billion in 2025, up 2.3x year-on-year, with Mastercard's subsequent $1.8 billion acquisition of BVNK signalling that stablecoin settlement rails are becoming permanent infrastructure.

The displacement of correspondent banking is moving along two distinct infrastructure models. Stablecoin-native platforms such as BVNK focus on smaller-ticket, wallet-based transactions and use blockchain-based rails to move value outside conventional fiat clearing entirely. Regulated fiat-native platforms such as Airwallex build proprietary networks of local accounts, direct clearing access and prefunded balances to achieve the same outcome within the conventional banking system. In both cases, the competitive advantage derives from reducing intermediaries, not from the underlying currency.

By holding local balances across over 60 markets and connecting them through its own platform rather than through a chain of correspondent banks, Airwallex achieves the same settlement speed and cost advantages as stablecoin rails. In 2025, Airwallex reported an 85% year-on-year increase in revenue and 71% growth in transaction volume, reaching $266 billion in annualised transaction volume by December. Singapore was a standout market, with revenue up 107% and transaction volume rising 93% year-on-year.

Beyond stablecoin-native and fiat-native platforms, a third cohort of established cross-border players is beginning to explore digital assets selectively. Wise is exploring how customers can use cryptocurrencies on its platforms, not as a replacement for fiat infrastructure but as a tool to improve internal liquidity and payment flows for small and mid-sized merchants. Revolut's EU-wide crypto licence under MiCA in October 2025 points in the same direction. For both, the move is an extension of existing network architecture rather than a strategic pivot away from fiat rails.

Banks are cautious on stablecoins for large corporate payments but some are already building on new rails

Most banks remain cautious on stablecoins for large corporate payments, citing cross-border regulatory fragmentation, KYC/AML compliance across jurisdictions, network congestion and pricing, bridge security vulnerabilities, legal ambiguity around accountability, and inconsistent redemption periods. The more telling divide is between institutions still monitoring the space and those already running live stablecoin or tokenised payment infrastructure, highlighting early movers versus cautious incumbents.

Banks want better interoperability across legacy infrastructure and blockchain platforms in cross-border payments to cut compliance risk, cost and settlement delays. As they monitor the stablecoin space, their immediate focus is tokenised deposits and digital asset offerings for institutional investors and corporate banking clients. Tokenised deposits are emerging as the mechanism for programmable bank money across payments, treasury management and wholesale settlement processes, enabling liquidity to move seamlessly between branches of the same institution. Proprietary blockchain networks allow continuous 24/7 settlement by representing corporate or institutional deposits as tokens on an internal ledger, streamlining internal fund transfers while maintaining regulatory and operational control.

J.P. Morgan disclosed that its Kinexys platform processed $7 billion in average daily transaction volume in 2025 and has handled over $3 trillion since launching as Onyx in 2015.

Standard Chartered has built the broadest institutional digital asset infrastructure among global systemically important banks, spanning custody, spot trading, tokenisation and settlement. Originally developed through ventures including Zodia Custody, Zodia Markets and Libearathe bank is now pulling these capabilities into its core Corporate and Investment Bank — most notably through its confirmed acquisition of Zodia Custody — signalling a shift from experimental buildout to mainstream banking infrastructure.

In December 2025, Standard Chartered went live with a tokenised deposit solution across Hong Kong and Singapore in partnership with Ant International, covering HKD, CNH, SGD and USD. The bank is now running live corporate treasury flows on that infrastructure in the Hong Kong-Singapore corridor, making it one of the first international banks to move tokenised deposits from controlled testing into day-to-day client operations. The bank has also issued a HKD-backed stablecoin for corporate clients, acting as trustee and custodian, with client holdings off-balance-sheet and principal positions on-balance-sheet.

Deutsche Bank is also actively building infrastructure to support tokenised assets and deposits, with a clear focus on near-instant settlement and liquidity efficiency. By tokenising government bonds and other regulated instruments, the bank enables near-instant collateral mobilisation and atomic payments, reducing settlement risk and operational friction. These tokenised assets remain anchored to traditional regulated payment rails, ensuring legal certainty and compliance.

Mizuho represents a regional dimension. The bank completed a proof-of-concept for tokenised deposits designed to bridge legacy core banking systems with decentralised ledgers. In October 2025, the bank joined MUFG and SMBC in a joint project to issue yen-backed stablecoins for corporate clients, enabling transfers between the three institutions under uniform standards. In addition, it is building host-to-host and multi-bank connectivity to embed tokenised and digital cash management capabilities directly into clients' ERP/treasury systems.

DBS Bank and J.P. Morgan are exploring an interoperability framework to connect their respective on-chain ecosystems, DBS Token Services and Kinexys Digital Payments, across both public and permissioned blockchains, potentially allowing institutional clients in Southeast Asia and the United States to transfer tokenised deposits across borders while maintaining value consistency.

Regulatory clarity and institutional capital are enabling the integration of DeFi and traditional finance, creating momentum to build the next generation of global payment infrastructure. Early examples from the world’s largest global and regional banks and payment networks suggest that DeFi-based payments will increasingly become a meaningful part of the global payments stack.

Correspondent banking revenues are under pressure, but new rails open fresh fee income streams

The impact on correspondent banking revenue is not uniform. Correspondent banking revenue derives from three sources: per-transaction processing fees, FX conversion margins and float income earned on nostro and vostro balances during multi-day settlement windows. Each faces a different threat profile.

Processing fees and FX margins are under direct competitive pressure — a platform that bypasses four correspondent intermediaries does not need to recover four layers of overhead, and that arithmetic does not change as the market matures. On an estimated $173 trillion market, a 1% margin compression across 20% of flows represents approximately $346 billion in annual revenue migrating away from legacy infrastructure.

Float income is categorically different: it faces permanent elimination as settlement accelerates to real time, irrespective of which rail carries the payment. This is not a digital asset displacement story — it is a structural revenue reduction driven by payment speed itself and it cannot be recovered by moving to new rails.

The partial offset from tokenised trade settlement, CBDC infrastructure and programmable FX is real. Banks building on new rails — JPMorgan with Kinexys, HSBC and Standard Chartered with its tokenised deposit architecture — will capture a portion of the fee income enabled by tokenised settlement and programmable FX Whether that capture offsets legacy margin compression in the medium term is, on current trajectories, unlikely for institutions that have not yet committed to new-rail infrastructure.

As these new settlement architectures begin to reconfigure cross-border payment flows, the competitive battleground is shifting from balance-sheet intermediation to transaction-level monetisation, where fee capture is increasingly driven by embedded, high-frequency and data-rich payment ecosystems.

Segments such as fintechs, digital platforms, and non-bank financial institutions generate high-velocity transaction flows. These create recurring fee income without significant balance sheet consumption, reducing reliance on interest income and enhancing revenue predictability.

Tokenisation and workflow integration allow fees to be captured on transactions more efficiently, supporting capital-light returns relative to traditional risk-weighted-intensive products. Banks embedding FX execution into payables and receivables workflows are already reporting a significant uplift in FX-related fees, demonstrating that automation and tokenised settlement can grow fee capture rather than simply redistribute it.

Early movers on tokenised payment rails will capture flows that laggards cannot recover

Traditional correspondent banking faces structural pressure on multiple fronts. Transaction fees and FX margins are under competitive compression from platforms bypassing correspondent chains, while float income faces permanent elimination as settlement accelerates toward real time. Banks that move early to integrate tokenised deposits, programmable FX and blockchain-based settlement infrastructure can capture fee-based, capital-light revenue streams that partially offset that erosion.

The treasury automation gap is the most immediate competitive opportunity available to incumbent banks. Banks that can offer API-native ERP connectivity, real-time multi-currency visibility, and integrated pre-payment compliance validation are competing for corporate clients still deciding which cross-border settlement platform to adopt. Platform choices will consolidate quickly as treasury teams solve the automation problem, and switching costs will rise once they do. Banks that move earliest to offer bank-grade settlement capabilities on new rails will capture both the volume migrating from legacy correspondent chains and the incremental flows generated by treasury automation and tokenisation.

Banks that embrace interoperability, 24/7 liquidity and real-time settlement are positioned to capture high-frequency cross-border flows, corporate treasury services and embedded payment opportunities. Those that delay risk losing share to fintechs, non-bank platforms and first-mover banks already leveraging digital rails. The window is closing, as adoption of tokenised and programmable infrastructure becomes a condition of relevance rather than a choice.

.png)

.png)

.png)

.png)

.webp)