Digital banks in their early years often prioritise customer acquisition at the cost of unit economics. Revenue typically begins with subscriptions, deposits and interchange fees before diversifying as the product set matures, and it is at this stage that the economics begin to compound towards profitability. Webank, Revolut and Nubank have each followed this arc. But for most digital banks that lack this ability to scale globally, regionally or even locally, the path to profitability is far more challenging.

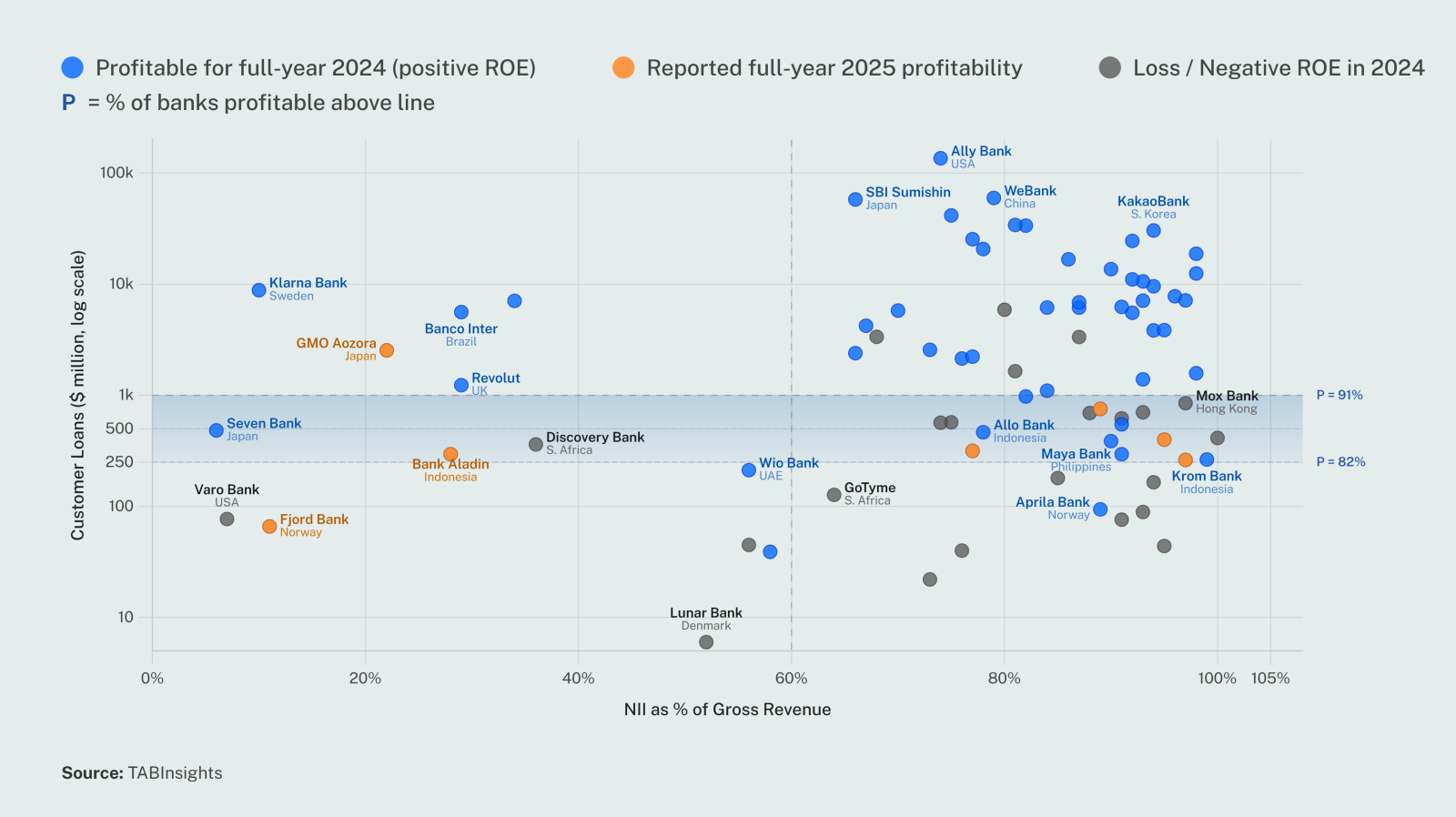

Across the World’s Top 100 Digital Banks, loan book size is one of the key drivers of sustained profitability. Banks with loan balances above $250 million and net interest income contributing at least 60% of revenue are measurably more likely to be profitable; those below that threshold are generally not, regardless of how long they have been in the market or how broad their product range may be.

The relationship is not linear. In the World’s Top 100 sample (Figure 1), 82% of banks with loan books above $250 million are profitable. At $1 billion, that figure rises to 91%. The $1 billion mark is where a digital bank’s lending business reaches sufficient scale to cover its cost base, absorb credit losses and generate sustainable returns.

The profitable cohort carries a substantive lending business, though almost entirely concentrated in consumer finance. Only a handful — Kakao Bank in South Korea and Ally Bank in the US among them — have built diversified portfolios that extend into mortgages or corporate credit.

Among banks with loan books between $250 million and $1 billion and net interest income (NII) above 60% of total income, most of the unprofitable ones as of 2024 are based in Singapore, Hong Kong and Taiwan. Digital banks in Hong Kong and Singapore have been operating since 2020 and 2022 respectively, while most Taiwanese digital banks launched in 2021.

Several have since crossed into profitability between 2025 and 2026. In Hong Kong, ZA Bank and livi Bank achieved full-year profitability in 2025. WeLab sustained quarterly net profits through at least H1 2025, although did not report a full-year net profit for FY2025. LINE Bank Taiwan reported its first monthly pre-tax profit in December 2025, while Trust Bank Singapore reached the same milestone in March 2026. Green Link Digital Bank (GLDB), a digital wholesale bank in Singapore, also indicated it turned profitable in 2025, four years after launch.

Outside Taiwan, Hong Kong and Singapore, Discovery Bank South Africa — in the market since 2018 — posted its first profitable period in the second half of 2025. GMO Auzora Bank Japan reported its first full-year net profit in 2025, eight years after launching in 2018. Aladin Bank and Superbank in Indonesia both reported earnings turnarounds in 2025. Superbank, majority-owned by Grab, the Southeast Asian super-app that bundles transportation, delivery and financial services, is being fully integrated into the platform. In Europe, Fjord Bank Norway, active since 2019, reported its first positive net income in 2025.

Below the $250 million threshold, most banks have yet to build a substantive lending book. Instead, they park deposits in high-quality liquid assets, primarily central bank reserves. GoTyme South Africa, for example, had a loan book of SAR 2.25 billion ($128 million) as of June 2025, six years after launching in 2019, with 52% of its financial instruments allocated to government bonds and treasury bills.

Time is necessary, but not sufficient for profitability

A vintage analysis adds a time dimension. Digital banks in the 13-years-plus cohort cluster almost uniformly as profitable and at large loan book scale, while the three-to-six-year brackets contain the highest concentration of loss-making institutions. As LINE Bank Taiwan, Yillion Bank in China and Discovery Bank South Africa each illustrate, time in the market and loan scale are correlated, but neither alone is sufficient.

The typical breakeven window is three to six years, though timing depends on market conditions and operating context. The outliers — Webank China, Kakaobank South Korea, OakNorth UK, Judo Bank Australia, Maya Bank Philippines — reached full-year profitability within 2.5 to 3.5 years. Each benefited from structural advantages that are not easily replicated: a concentrated addressable market, embedded platform distribution, or a regulatory regime that accelerated lending growth.

The gap between profitable and loss-making digital banks widens, increasing pressure on banks seven years and older

Each year of profitability funds further product expansion and lending capabilities, deepening revenue per customer and raising the barrier to competitive entry. The loss-making cohort, by contrast, faces a materially tighter funding environment than earlier entrants did. Rising customer acquisition costs, combined with low activation rates, have closed off the growth-first route to profitability that earlier cohorts relied on.

Yillion Bank in China and Italy’s illimity Bank had previously reported positive earnings, but both returned to losses in 2024 and 2025. Discovery Bank in South Africa, launched in 2018, became profitable in the second half of 2025. Meanwhile, N26 in Europe, Lunar Bank in Denmark, Varo Bank in the US and CIMB Philippines, all launched between 2015 and 2018 and now in the market for more than seven years, have yet to achieve consecutive full-year profitability.

Building a bank at scale without first establishing the controls needed to operate it

N26’s decade of losses was not a growth problem. It was a governance and business model failure, driven by management decisions that regulatory intervention made irreversible until 2024. N26 accumulated €1.025 billion ($1.1 billion) in losses between 2015 and 2024. The proximate cause was Germany’s Financial Supervisory Authority (BaFin), which imposed a 32-month customer onboarding cap (October 2021 to June 2024) after systematic failures in AML suspicious-activity reporting. N26 drew a combined €13.45 million ($14.4 million) fine between 2021 and 2024. The cap was not merely a growth constraint. It landed as the ECB raised rates from −0.5% to 4.0%, the window in which deposit-funded NII should have rescued N26’s unit economics. Capped at 50,000–70,000 new customers per month against an organic run-rate of 170,000-plus, N26 missed out on hundreds of millions of euros in annualised NII at peak rates.

Competitively, the cap handed Revolut an uncontested three-year window. By 2024, Revolut reported revenue of $4 billion against N26’s $471 million — an eight-fold gap that did not exist in 2019.

The underlying business and governance model was already structurally fragile before BaFin intervened, and that fragility traces directly to decisions made by co-founders Valentin Stalf and Maximilian Tayenthal. Their prolonged focus on registered user scale over monetisation quality produced a freemium architecture in which roughly half of ten million registered accounts generated no revenue, holding blended annual revenue per user at approximately €92 ($98), barely viable against the compliance and servicing cost of a fully licensed EU bank. The decision to expand into the US, Brazil and the UK without the regulatory infrastructure to sustain those markets produced costly retreats from all three. The founders’ retention of special veto rights over strategic decisions, backed by a governance structure that concentrated control in their hands, delayed the course corrections that investors and regulators were demanding.

Its revenue model was fragile too. Premium subscription revenue contributed only around 15% of total income, while interchange from a free-tier majority remained thin. By contrast, Revolut’s subscription turnover reached $541 million in 2024, a 74% year-on-year increase, roughly 14% of its $4 billion total revenue, but at an absolute scale nearly four times the entirety of N26’s premium fee income. Across Premium, Metal and Ultra plans, 45% more users adopted paid tiers. Aggressive product tiering, not registered user accumulation, is the decisive monetisation variable in digital banking. N26’s failure to convert its customer base into paying subscribers at comparable rates left it structurally weakened.

N26’s loan book at end-2024 was €3.14 billion ($3.4 billion), larger in absolute terms than Revolut’s $1.2 billion but composed predominantly of low-yield Dutch municipal bonds and Dutch mortgages rather than higher-margin consumer credit. Revolut’s lending book, though smaller, is almost entirely unsecured consumer and SME credit generating significantly wider spreads. The divergence runs deeper than size. Revolut has built a high-margin, diversified lending engine; N26 anchored its balance sheet in low-risk, low-return fixed income. That structural choice partially explains why N26’s NII recovery, while real, remained constrained even as ECB rates peaked.

These structural weaknesses now threaten N26’s long-term viability. BaFin imposed fresh sanctions in late 2025, halting Dutch mortgage lending, adding capital requirements, and appointing a new special monitor, triggering a rupture between founders and investors. Co-founder Stalf stepped down as CEO; Tayenthal followed by end-2025. A bank built on a model its own founders were unwilling to restructure until forced to do so was never positioned to succeed. Former UBS Group chief operations and technology officer Mike Dargan was appointed sole CEO in December 2025, with a planned April 2026 start date subject to BaFin approval.

Yillion Bank’s losses reflect risks from platform-dependent growth, weak governance and regulatory pressure in China’s digital banking sector

Yillion Bank, a Chinese digital bank founded in 2017, has grown to more than $5.6 billion in total assets and an estimated 45 million users. Yet its recent performance shows how deteriorating market conditions can expose major structural weaknesses. After remaining profitable through 2023, the bank fell into a net loss in 2024 and 2025, hit by a combination of revenue decline, weak risk controls, governance failures linked to its largest shareholder, and tighter external regulation.

Net losses increased from RMB 590 million ($83 million) in 2024 to RMB 1.48 billion ($207 million) in 2025. The larger 2025 loss was largely deliberate: management disposed of legacy bad loans, raised provisions, and wrote down risky assets to reset the balance sheet. The deeper problem, however, was structural. Yillion’s growth model depended heavily on external platforms, primarily Meituan, for customer acquisition. When cooperative volumes shrank, service fees to Meituan dropped 93% between 2021 and 2024, and the bank had no independent channel to fall back on. The non-performing loan ratio jumped from 1.61% in 2023 to 2.77% in 2024, forcing impairment losses of RMB 1.47 billion ($206 million) in that year alone, before easing to 1.78% in 2025. Governance failures and regulatory pressure added to the strain. Its major shareholder, Zhongfa Group, a Chinese private investment conglomerate whose aggressive real estate expansion eventually turned into a debt crisis, contributed directly to Yillion’s operational instability, with four bank presidents in seven years causing persistent strategic inconsistency. New internet deposit rules cut cheap funding and narrowed net interest margins further.

The window for loss-making institutions to close the gap is narrowing

By the time TABInsights releases the 2026 ranking, more than 66% of the top 100 digital banks are projected to be full-year profitable. The sector's centre of gravity is further shifting to return expectations. Institutions that have not crossed the $250 million loan threshold and profitability within five to seven years of commercial operation face growing pressure to justify continued independent investment.

.png)

.webp)