.webp)

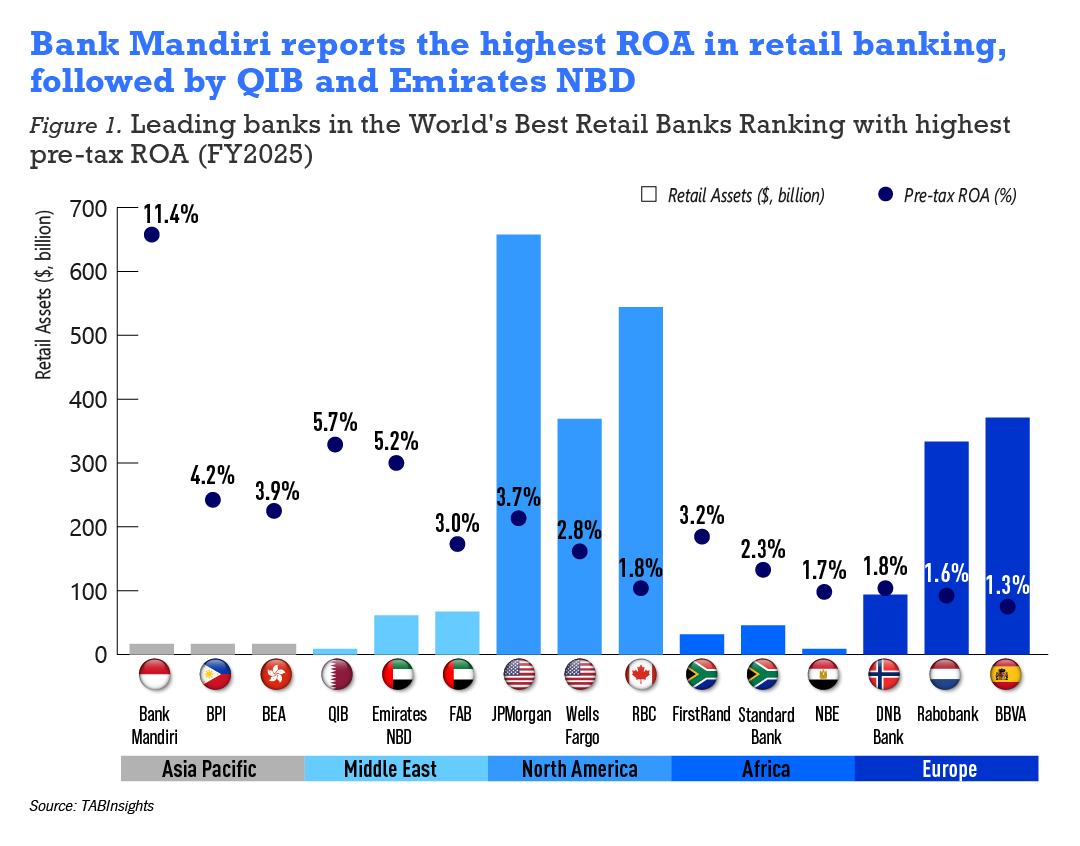

Across 100 global retail banks in FY25, asset size and return on assets (ROA) move in opposite directions. Regional leaders show that superior profitability reflects the compounding of several factors: market structure, segment mix, funding discipline and operational efficiency, rather than any single driver.

Mid-sized and regional banks cluster at the higher ROA end, while larger institutions generate lower returns per asset dollar. The relationship is not absolute, as JPMorgan Chase illustrates, but consistent enough to warrant examination.

Bank Mandiri leads Asia Pacific with an 11.4% ROA on $16.5 billion in retail assets, reflecting both structural and strategic factors. Indonesia’s high net interest margin (NIM) environment is supported by elevated rates, low credit penetration and limited foreign competition, which expand revenue capacity. Mandiri captures this through a higher-yield retail and SME mix, low-cost current account savings account (CASA) funding and digital-led cost efficiency. In comparison, Bank of the Philippine Islands delivers 4.2% ROA despite similar positioning, constrained by lower spreads and stronger competition. Bank of East Asia reports 3.9% ROA, where tighter margins increase reliance on cost discipline and risk control.

In the Middle East, Qatar Islamic Bank generates a 5.7% ROA on $8.6 billion in assets. Its 16.3% CIR, the lowest in the sample, reflects both revenue strength and cost control. Islamic profit-sharing structures support margin stability, while government-linked depositors provide stable low-cost funding and a concentrated market sustains pricing discipline. Emirates NBD achieves a comparable 5.2% ROA on $61.8 billion in assets by combining domestic pricing power with a diversified non-interest income base across trade finance, wealth management and cards.

In Africa, First National Bank (FNB) leads with a 3.2% ROA on $32.1 billion in retail assets. South Africa’s concentrated banking market supports lending yields and pricing discipline. FNB reinforces this through higher-margin retail and business banking segments and transactional income, reducing reliance on the credit cycle.

In Europe, DNB Bank records the highest ROA at 1.8% on $94.9 billion in assets, with a 40% CIR against a regional average of 54.5%. Norway’s concentrated mortgage market limits foreign competition and a Stage 1 and 2 loan classification rate of 99.3% contribute to lower operating and provisioning costs. BNP Paribas and Lloyds Banking Group, with CIRs of 60% and 54.9%, operate under different structural conditions.

In North America, JPMorgan Chase posts a 3.7% ROA on $664.7 billion in assets, maintaining higher returns despite its scale. This reflects the strength of its national deposit franchise, which provides stable, relatively low-cost funding, alongside a diversified non-interest income base across cards, wealth management and payments. Operating scale and branch network efficiency further support cost absorption. In comparison, Wells Fargo records a 2.8% ROA on a similar asset base, indicating that differences in franchise composition and revenue mix, rather than size alone, shape returns.

The data suggests that scale enables earnings volume but does not reliably produce asset efficiency. The drivers that distinguish high-ROA banks — segment concentration, cost discipline and pricing power rooted in market position — are structurally more accessible to focused, mid-sized institutions than to large universal banks managing diversified, capital-intensive portfolios. This explains why the negative correlation holds and why JPMorgan's performance is the exception, rather than the model the data supports.

View the full World's Best Retail Banks Ranking here.

.png)