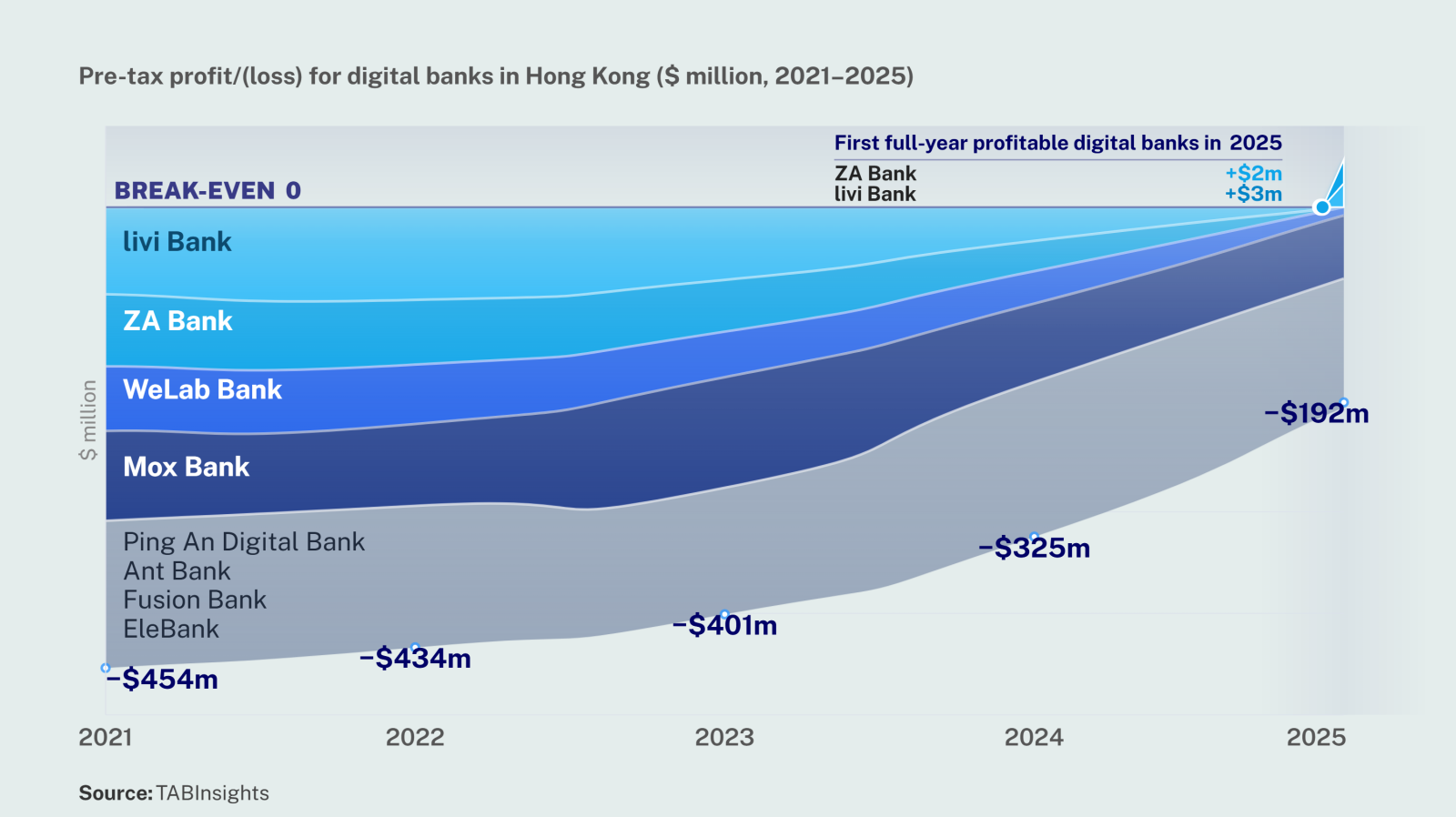

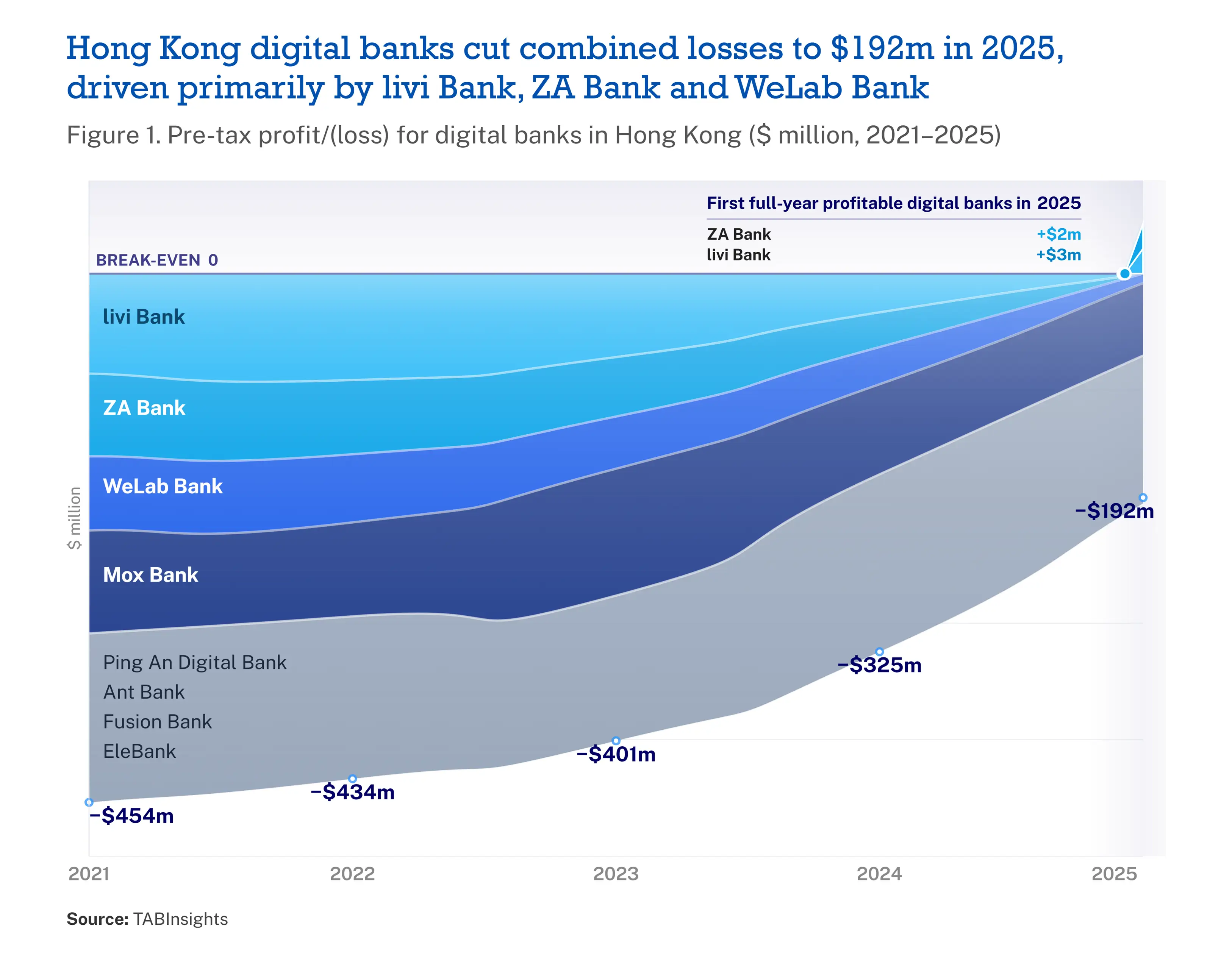

Hong Kong’s digital banks reached a turning point in 2025, with the first two players turning profitable. Six years after the launch of virtual banking licences, the improvement reflects a shift towards earnings-driven growth. Stronger deposit bases and lending expansion have supported higher net interest income, while broader product offerings across wealth management, insurance distribution and other fee-generating services have diversified revenue streams and improved income quality. Cost efficiency gains have also strengthened operating performance as scale effects began to materialise.

Aggregate pre-tax losses across Hong Kong’s eight digital banks narrowed by 58%, from HKD 3.5 billion ($454 million) in 2021 to HKD 1.5 billion ($192 million) in 2025. ZA Bank and livi Bank were the first full-year profitable digital banks in Hong Kong in 2025. WeLab Bank achieved its first monthly break-even in December 2024 and sustained profitability through the first half of 2025. Mox Bank reached break-even in early 2026, reinforcing the broader shift towards profitability across leading players. Ant Bank, EleBank (formerly Airstar Bank) and Ping An Digital Bank (formerly PAObank) continued to post widening losses over the period.

Profitability emerges among leading banks

The break-even path for digital banks in Hong Kong is taking shape, although performance continues to vary significantly across the sector. WeLab Bank and Mox Bank are expected to achieve full-year profitability in 2026, while two additional banks could reach break-even by 2028.

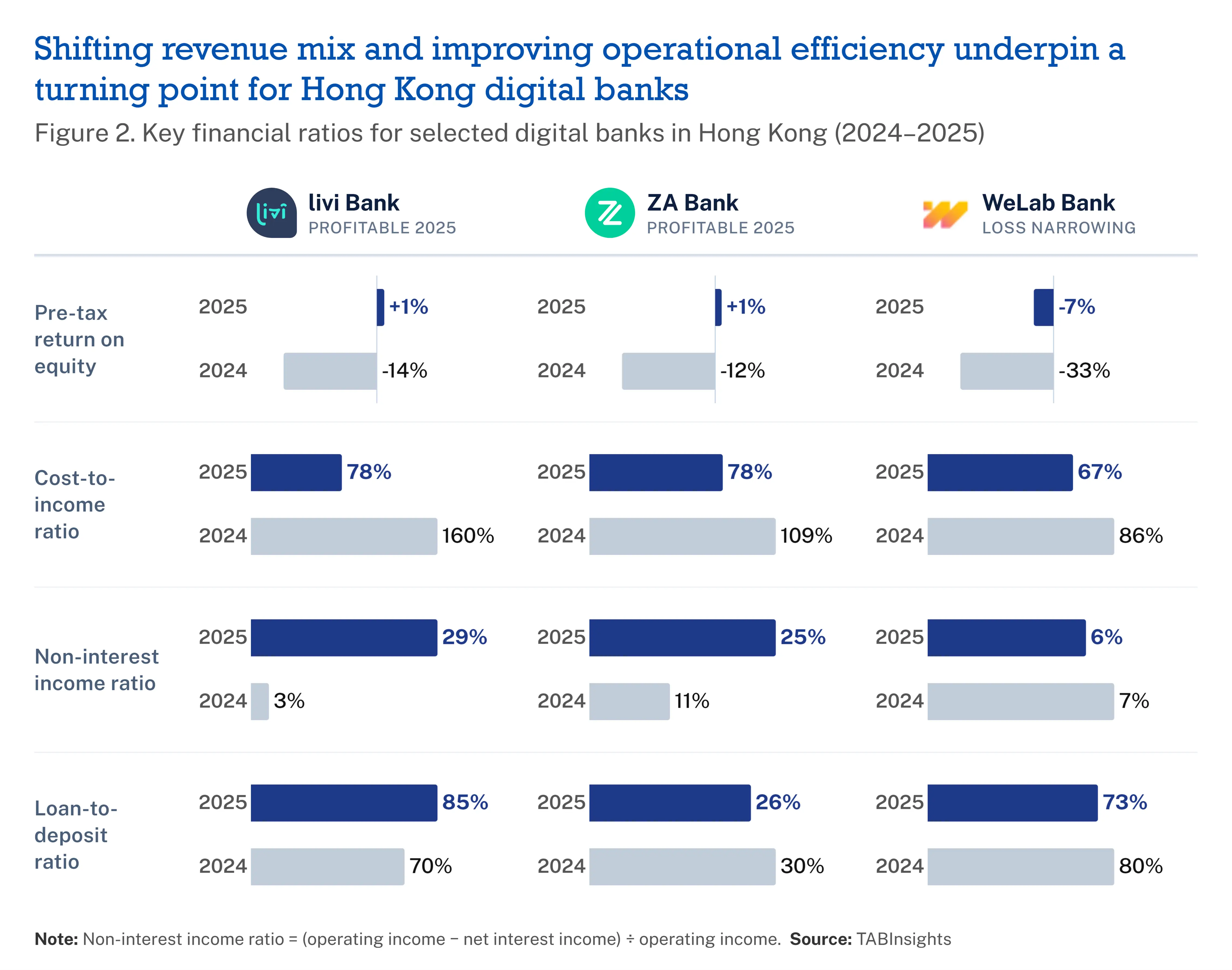

ZA Bank posted a pre-tax profit of HKD 17 million ($2.2 million) in 2025, with a pre-tax return on equity (ROE) of 0.8%, while livi Bank recorded a pre-tax profit of HKD 21 million ($2.7 million), with a pre-tax ROE of 1.1%. WeLab Bank recorded pre-impairment operating income of HKD 306 million ($39 million) but still posted a pre-tax loss of HKD 63 million ($8.1 million), mainly due to higher provisions.

These three banks have followed different trajectories towards profitability. ZA Bank’s net interest income was driven by deployment of its strong deposit base into bond and money market investments, reflecting its low loan-to-deposit ratio (LDR) and investment-led model. Non-interest income was supported by commission-based agency services, including insurance distribution, mutual funds and securities brokerage, alongside card-related fees.

livi Bank’s profitability in 2025 was supported by growth in net interest income from expanding consumer and SME lending, alongside a sharp rise in non-interest income driven by its B2B FinTech Solutions business. Embedded finance offerings to SME clients, combined with wealth management and loan-related fees, contributed to a more diversified revenue structure.

WeLab Bank’s trajectory was driven primarily by its unsecured retail lending franchise, supported by data-driven underwriting and AI-enabled credit risk management. This lending-led model underpinned strong net interest income, with an industry-leading net interest margin of 10.6%. Non-interest income was supported by wealth management activities and foreign exchange services.

Banks such as Ping An Digital Bank, Ant Bank and Fusion Bank have accumulated sizeable deposit bases but remain constrained in loan deployment, with LDRs of 36%, 22% and 22% respectively. This has limited net interest income generation and slowed progress towards profitability. EleBank showed some improvement, with its LDR rising from 30% in 2024 to 58% in 2025, but continued to record losses due to a persistently high cost base relative to income.

Net interest income drives revenue growth as fee income gains ground

Hong Kong’s digital banks remain predominantly interest-driven, with net interest income accounting for 79% to 95% of total operating income between 2022 and 2025, reflecting reliance on deposit-funded lending and investment activities. Non-interest income is gradually rising through wealth management, insurance distribution and platform-based services.

WeLab Bank generated HKD 886 million ($114 million) in net interest income in 2025, up from HKD 31 million ($4 million) in 2022 and accounting for 94% of operating income. Its LDR stood at 74%, reflecting the strength of its unsecured retail lending franchise.

Mox Bank also relied heavily on net interest income, which accounted for 94% of operating income in 2025. Net interest income reached HKD 678 million ($87 million), while its LDR increased from 38% in 2024 to 69% in 2025, driven mainly by the acquisition of Standard Chartered Hong Kong’s personal instalment loan portfolio.

Non-interest income remains secondary across the sector, although contributions are increasing among selected players. livi Bank recorded the strongest expansion in 2025, with its share of non-interest income rising from 3% in 2024 to 29% in 2025. Fee income increased more than tenfold to HKD 91 million ($12 million), driven by the expansion of its B2B FinTech Solutions business. ZA Bank recorded a non-interest income share of 25%, with fee income rising 85% in 2025, supported by cards and agency services.

Cost efficiency underpins profitability improvement

Beyond revenue growth, cost discipline has been equally critical to the profitability gains. Hong Kong's digital banks are beginning to benefit from scale effects, expanding customer bases and loan books without proportionate increases in operating expenditure.

WeLab Bank was the first digital bank in Hong Kong to record a cost-to-income ratio (CIR) below 100%, improving from 86% in 2024 to 67% in 2025. Efficiency gains were driven by its AI-powered credit risk management system and cloud-native infrastructure, supporting stronger operating leverage as the business scaled.

ZA Bank and livi Bank both reported a CIR of 78% in 2025. livi Bank's operating expenses fell from HKD 710 million ($91 million) in 2022 to HKD 254 million ($33 million) in 2025, the lowest in the sector, while operating income rose from HKD 17 million ($2 million) to HKD 327 million ($42 million) over the same period. Cost optimisation was a key factor in its move into profitability. Operating expenses declined by 41% in 2024 and a further 28% in 2025, driven largely by workforce rationalisation and compensation restructuring.

Overall, Hong Kong’s digital banks have moved into a more commercially viable phase after more than six years in operation. Narrowing losses and emerging profitability among leading players reflect improving revenue quality, stronger lending momentum and early fee income diversification. However, performance remains uneven, with further progress towards break-even dependent on sustained loan growth, deeper fee income development and continued cost efficiency gains.

.png)

.webp)