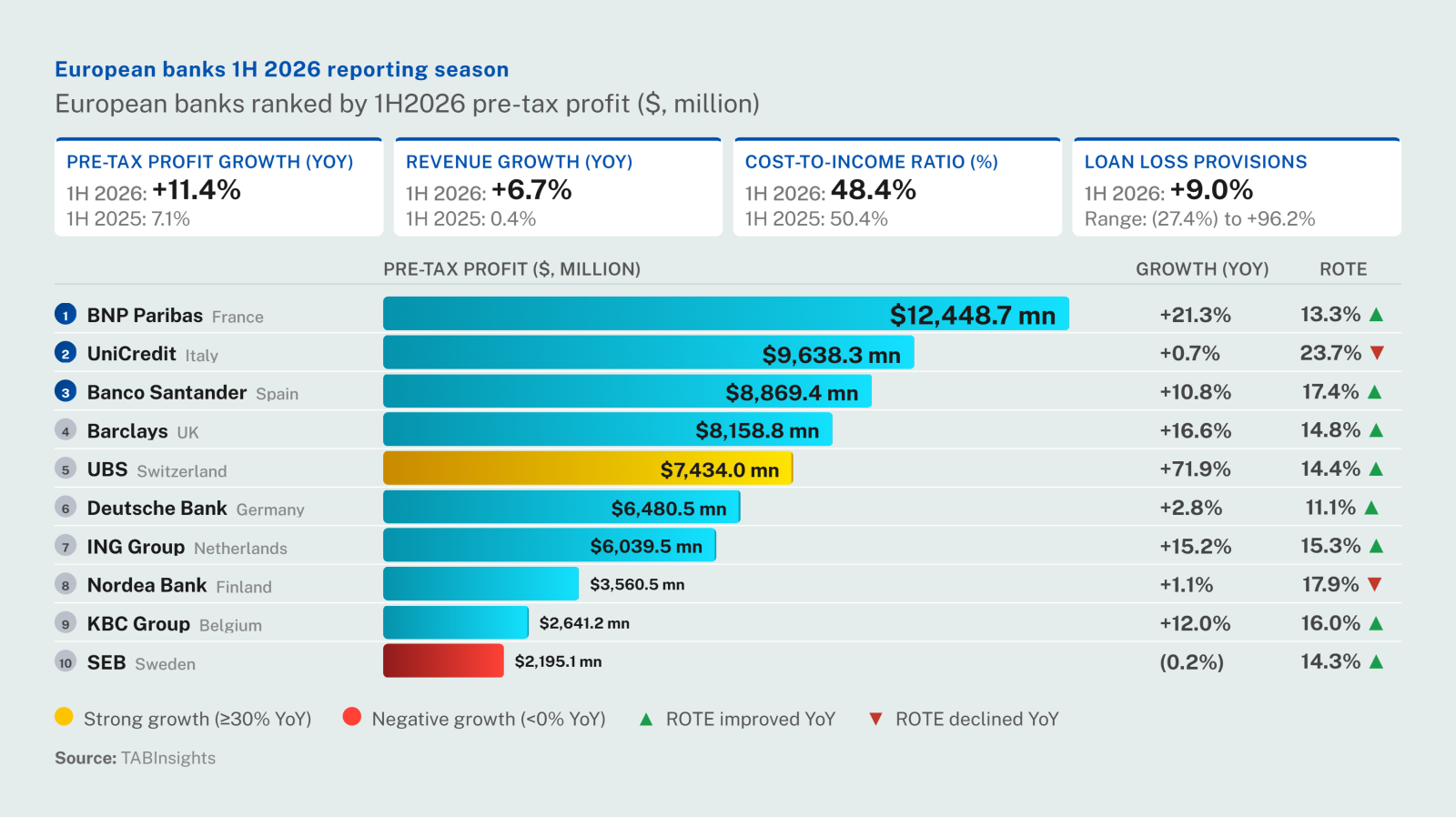

Bank Results Aug 07

Europe’s largest banks by country showed surprising resilience in the first half of 2026, with broad-based growth across their business segments. UBS, Barclays and BNP Paribas stood out, although part of their results were boosted by corporate-centre gains, treasury performance and exceptional items. Strong earnings prompted several banks to raise their full-year guidance and reconsider mergers and acquisitions