Rankings

Feb 21

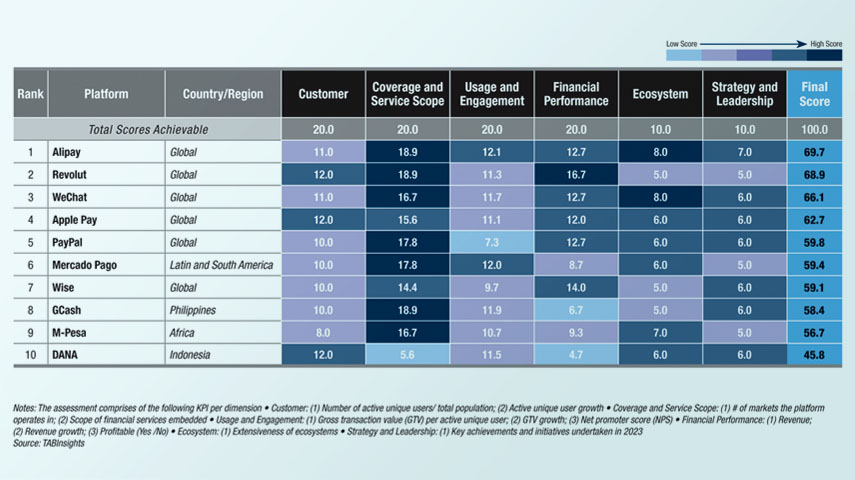

Asia is leading in financial platform development and adoption, with Alipay building a vast ecosystem and global reach, while Revolut excels in user acquisition and financial performance.

.png)

.png)