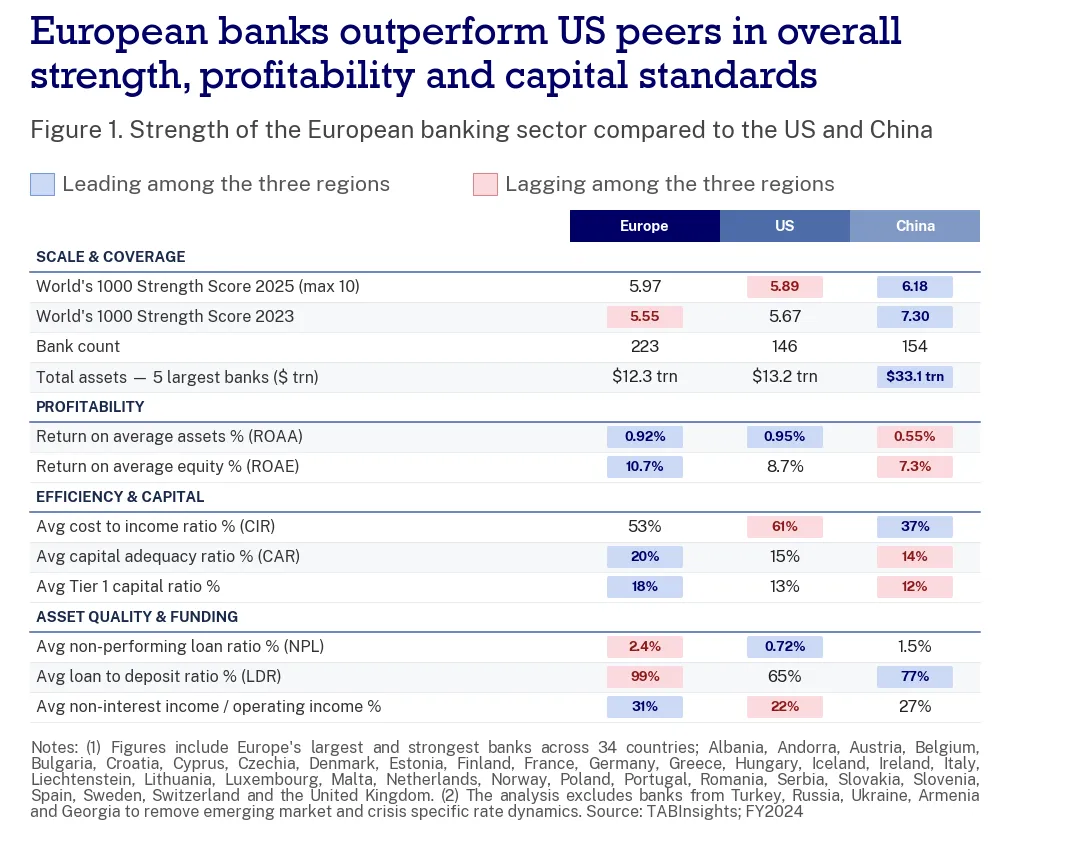

European banks saw asset growth accelerate for the second consecutive year, from a weighted average of 1.9% in 2023 to 2.9% in 2024, with 2025 expected at 4.2%. Resilient macroeconomic conditions across the continent supported this expansion: the euro area economy expanded by an estimated 1.4% in 2025, after recovering from subdued growth of 0.8% in 2024, according to IMF and European Commission projections. While some industry sectors remain under pressure — notably automotive and industrial manufacturing, where weak export demand and elevated energy costs have weighed on margins, unemployment across the euro area remained near historic lows at approximately 6.2%, and headline inflation continued its gradual descent towards the ECB’s 2% target. At the same time, fears of a broader economic shock from US trade policy failed to materialise in a more meaningful way.

2025 was the year the European banking sector finally deployed its rebuilt strength into balance sheet growth

Banking sector credit growth, based on the more than 200 European banks in the dataset, accelerated from 1.1% year-on-year in 2023 to 2.4% in 2024, with 2025 expected to reach 3.3%, supported by volume growth despite narrower lending margins.

The largest European banks have closed much of their gap with US peers since 2020. The top 50 largest European banks lifted their median return on equity (ROE) from 3.6% in 2020 to a peak of 11.4% in 2023, easing to 10.0% in 2024 — ahead of the top 50 US banks, whose median ROE rose from 5.3% in 2020 to 9.5% in 2024.

The continent’s leading institutions have undergone a structural transformation in how they are capitalised, managed, and valued. The price-to-book ratio, which spent more than a decade below one, has risen sharply, now approaching 1.5x. The STOXX 600 Banks sub-index rose 67% in 2025, its strongest annual performance since 1987, according to STOXX data, outperforming the broader European market for a second consecutive year.

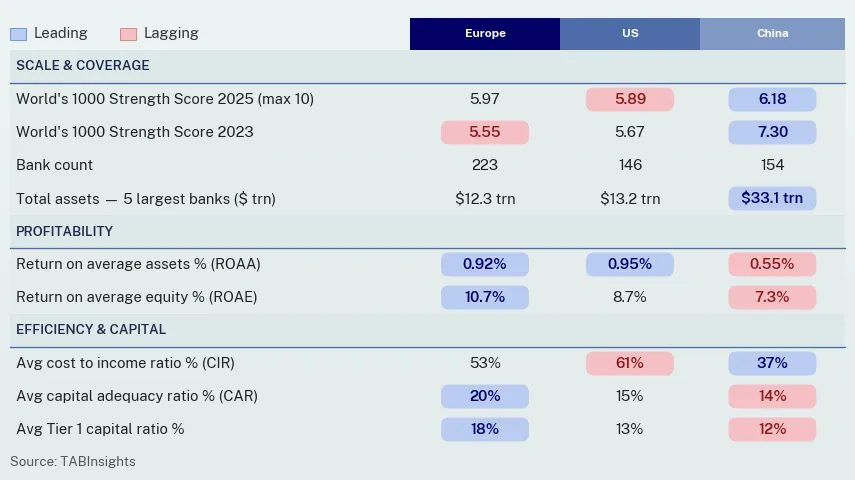

The renewed strength is also reflected in the World’s 1000 Largest and Strongest Banks Ranking. As a region, the European banking sector lagged the US and the Chinese market in overall strength in 2023 but has overtaken the US in 2024 and is closing the gap to China.

Capital discipline and shareholder returns have been the most visible drivers of this turnaround in European banking performance. European banks have rebuilt their capital bases to levels well above regulatory minimums, generating sustained surpluses that are now being returned at scale through dividends and buybacks. Payout ratios have risen to approximately 54% of earnings in 2025, up from 51% the prior year, according to the ECB, reinforcing investor confidence that profitability may be more durable than transient.

The accumulation of excess capital created pressure on bank management teams to deploy surpluses beyond buybacks into organic growth and acquisitions and created the conditions for a new wave of consolidation. Cross-border M&A accelerated sharply in 2025, with deal value reaching EUR 17 billion ($18.7 billion), a fivefold increase from EUR 3.4 billion ($3.7 billion) in 2024, according to Dealogic. That said, headline deal value overstates the degree of real integration taking place in European banking. Consolidation has occurred, but largely within national borders. Out of the top ten M&A deals in European banking in 2025, only two were cross-border. UniCredit’s (Italy) pursuit of Commerzbank (Germany) remains the only true large-scale cross-border play on the table, and its ongoing effort to make the case for a takeover. UniCredit sees Commerzbank as the missing piece of becoming a pan-European banking champion. Germany is Europe’s largest corporate banking market and owning both HypoVereinsbank (HVB) and Commerzbank would create a domestic market leader of EUR 1.46 trillion ($1.7 trillion) in assets and 35 million customers in Europe, capable of competing with the largest European and American banks at scale. UniCredit is Commerzbank’s largest shareholder and currently holds a direct stake of 26.8%. The Italian bank has become increasingly assertive in its pursuit of a takeover since 2024 and is taking its case directly to shareholders.

For all the renewed momentum, financial fragmentation remains the defining constraint. The ECB, in its consultation response to the European Commission on EU banking sector competitiveness, is a reminder that national ring-fencing of capital and liquidity, enforced through host-country supervisory requirements and legal entity structures, effectively prevents banking groups from deploying resources freely across borders.

Cross-border barriers remain high. Intra-EU service trade costs, including in the financial sector, are roughly equivalent on average to an ad valorem tariff of around 95% compared to domestic trade. The scale gap with US peers is the clearest expression of this shortcoming. The top eight US banks command 55% of domestic banking assets, against 41% for their euro area equivalents, a structural disadvantage that compounds over time as American institutions deploy greater resources into technology, talent, and global expansion.

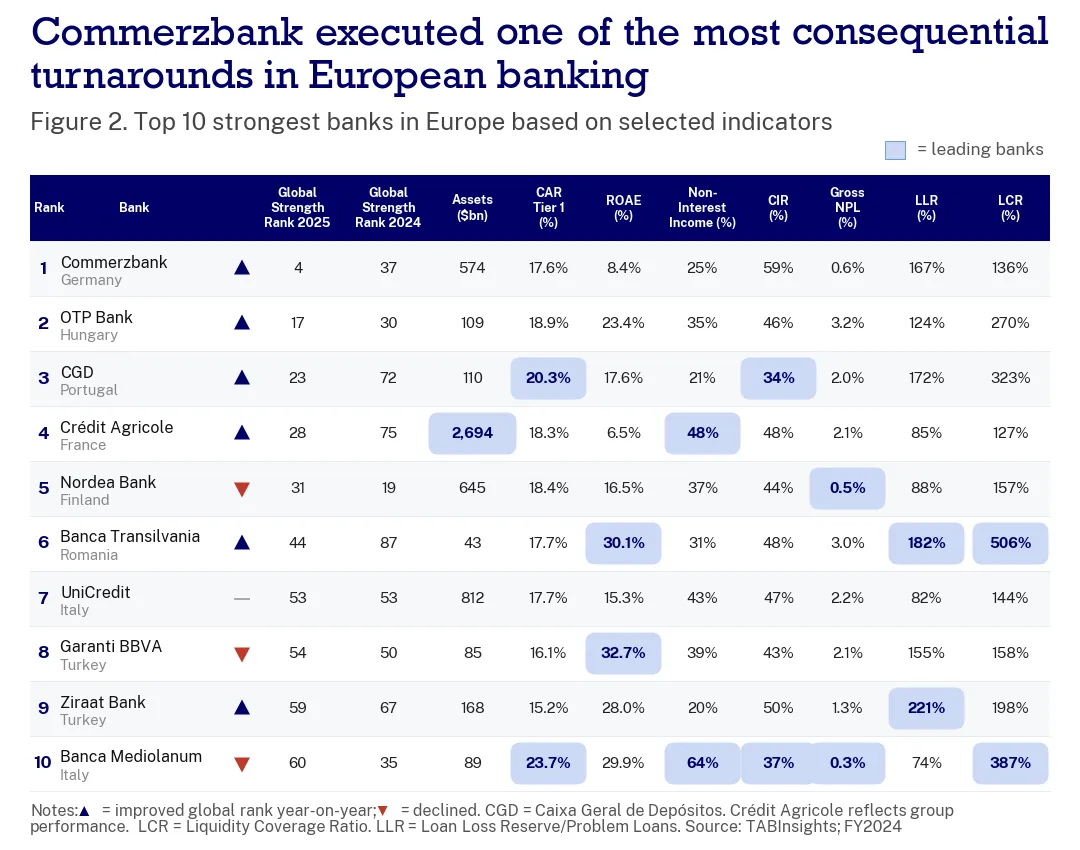

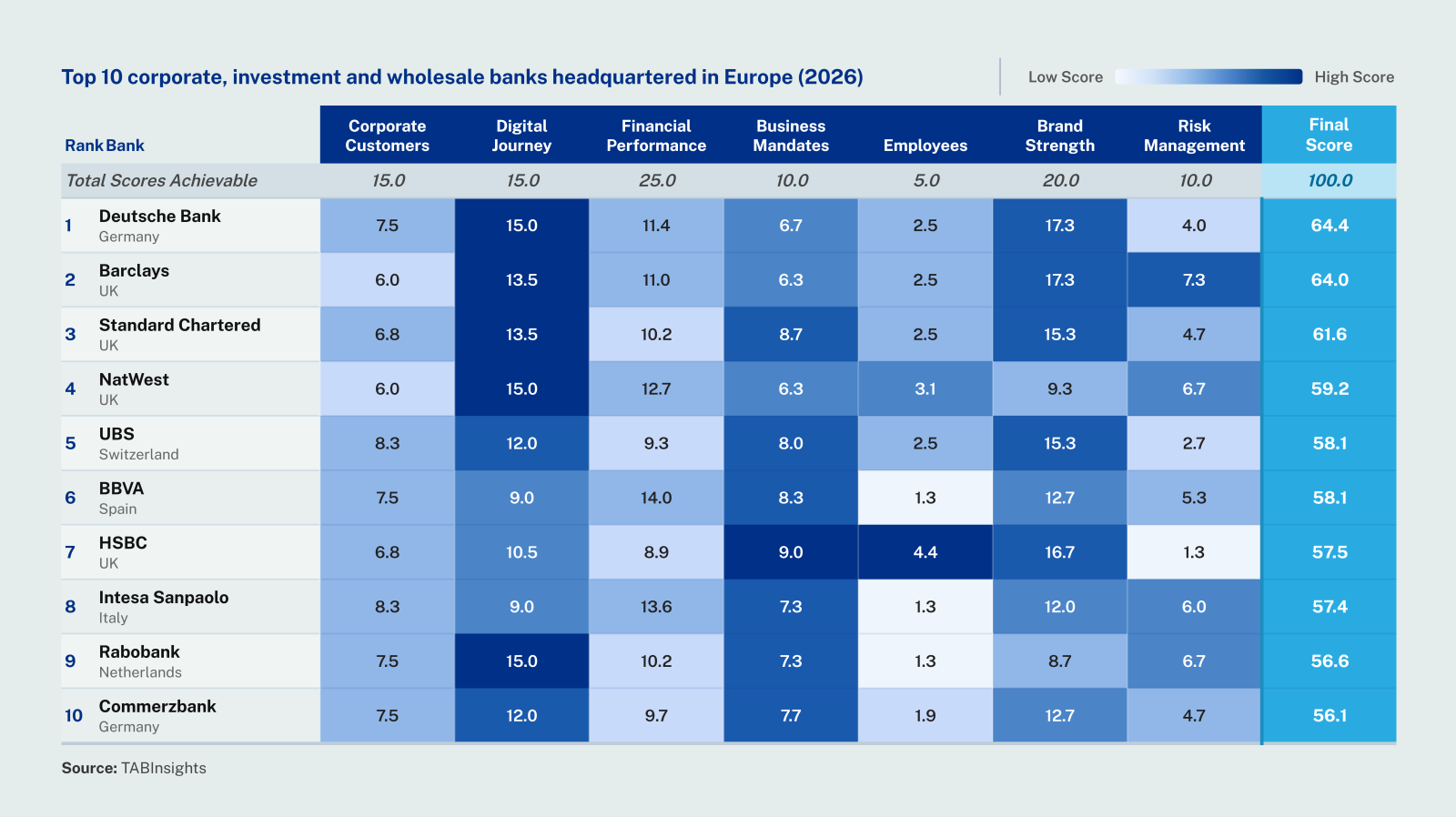

Within this broader reshaping of European banking, Commerzbank has delivered one of the sector’s most consequential turnarounds, rising to the #1 position among Europe's strongest banks and #4 in the World's 1000 Strongest Banks Ranking — a result built on four years of restructuring, revenue diversification and capital return.

Back in 2020, Commerzbank entered this decade with an impaired business model, a negative ROAE, a cost structure among the heaviest in European banking and a German government still holding a crisis-era stake that signalled market scepticism about its long-term viability. The inflection came in FY2022, when the ECB's rate-hiking cycle began transmitting through Commerzbank's retail and SME-oriented loan book, providing the income momentum that its restructuring programme had cleared the ground to capture.

By FY2023, the transformation was already delivering sustained results. Net profit rose by 59% to EUR 2.2 billion ($2.4 billion), the bank’s strongest result in fifteen years, and by FY2024 it had risen a further 29% to reach EUR 2.8 billion ($3.1 billion), with revenues climbing to EUR 11.2 billion ($12.1 billion). Asset quality throughout remained exceptional, with an NPL ratio of 0.64% against a European sector average of 2.4%. In FY2025, the return on tangible equity (ROTE) hit 10% before restructuring expenses, its highest level since the global financial crisis.

The bank’s ‘Momentum’ strategy targets a net result of EUR 4.2 billion ($4.5 billion), a ROTE of 15%, and a CIR of 50% by 2028. Consistent with that ambition, Commerzbank's board rejected UniCredit's EUR 35 billion ($37.8 billion) exchange offer in April 2026, reaffirming its standalone strategy — the clearest possible signal that management views the transformation as complete enough to compete independently. Yet, the profitability of Commerzbank remains the lowest among Europe’s top 10 banks. By comparison, JPMorgan Chase reported profitability of 20% in 2025.

“The history of Commerzbank is a story of continued operating underperformance “, said the CEO of Unicredit, Andrea Orcel in a conference call with analysts, accusing the bank that 2025 results have been propped up by temporary tailwinds and financial engineering.

The dilemma Commerzbank is facing illustrates why improved performance alone cannot substitute for structural reform towards building larger banking groups in Europe. Limited cross-border integration and consolidation, hindered by regulatory, governance, and shareholder challenges as well as domestic and political interests, were highlighted by the ECB as a key factor in preventing banks from fully reaping the benefits of the ‘Single Market’. But easing cross-border merger rules alone is unlikely to be enough.

Comments by Germany’s Federal Chancellor Friedrich Merz show the political contradictions at the centre of this debate. Speaking at the annual reception of the Association of German Banks in Berlin in April, and without naming UniCredit directly, he said: “Large-scale financing and IPOs can often only be delivered and supported by the biggest banks. Yes, we need large banks in Europe. But let me also say very clearly, given the current situation: this does not mean that every form or type of takeover in Germany is welcome. We firmly reject hostile, aggressive conduct.” Germany still holds roughly a 12% stake in Commerzbank, down from a controlling position after the global financial crisis in 2008.

European banking enters 2026 in better shape than at any point since the global financial crisis (GFC). The sector’s ascent in the World’s 1000 Largest and Strongest Banks Ranking, surpassing the United States in FY2024 and closing the gap with China, reflects the result of a multi-year transformation in capital quality, cost discipline, and earnings resilience that the data in this analysis consistently confirms across 223 institutions across 34 countries from 2020 to 2024. Yet the sector is now facing a convergence of pressures: NIM normalisation, a CIR reversal already underway from its FY2023 trough, and a system-level fragmentation that no individual institution’s balance sheet strength can resolve. On the demand side, Eurozone-only credit data published by the ECB for January and February 2026 suggest that monthly credit growth on both the consumer and corporate side is holding up, but banking executives are nervous about the full-year outlook.

Towards a more integrated European banking union

The ECB's April 2026 consultation response provides the most operationally specific blueprint for completing the banking union since the European Deposit Insurance Scheme?(EDIS) negotiations collapsed in 2022. EDIS is the proposed third and still-missing pillar of the European banking union. It would create a single, pan-European fund guaranteeing bank deposits of up to EUR 100,000 ($180,000) across all eurozone member states. Its nine recommendations target the structural constraints: unlocking an estimated €230 billion ($248 billion) in trapped subsidiary liquidity, treating cross-border intra-group exposures on equal terms with domestic ones, and establishing a clear EDIS implementation timetable to eliminate the sovereign-bank doom loop constraining pan-European consolidation.

Geopolitical headwinds have lent this roadmap towards a more integrated banking union a strategic urgency that a decade of regulatory negotiation failed to deliver. The case for completing the banking union is no longer purely conceptual; Europe increasingly regards this as a matter of strategic autonomy, as dependence on US payment infrastructure and US investment banks in European repo and foreign exchange markets, all represent vulnerabilities that geopolitical stress has made visible. If successful, the European banking sector would emerge as a genuinely integrated financial system capable of competing with other major regional banking sectors on equal terms — deploying capital freely across borders, consolidating at scale and financing Europe’s infrastructure and digital transformation needs from a single, deep and liquid market.

.png)

.webp)