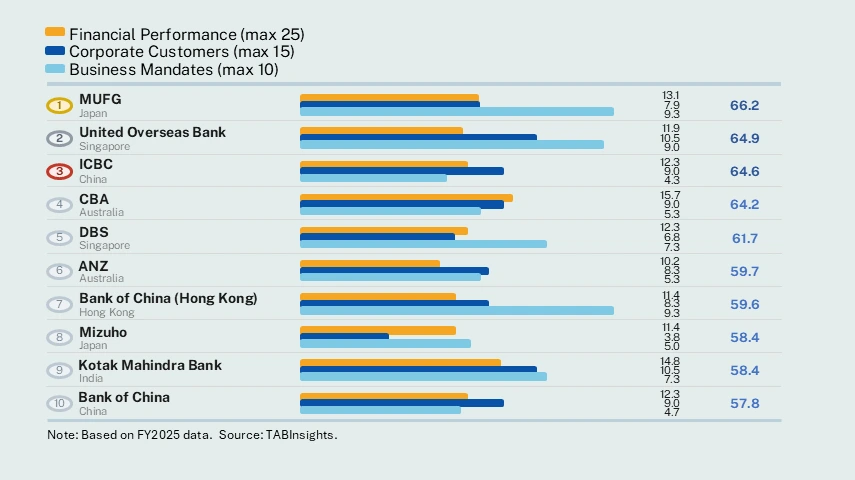

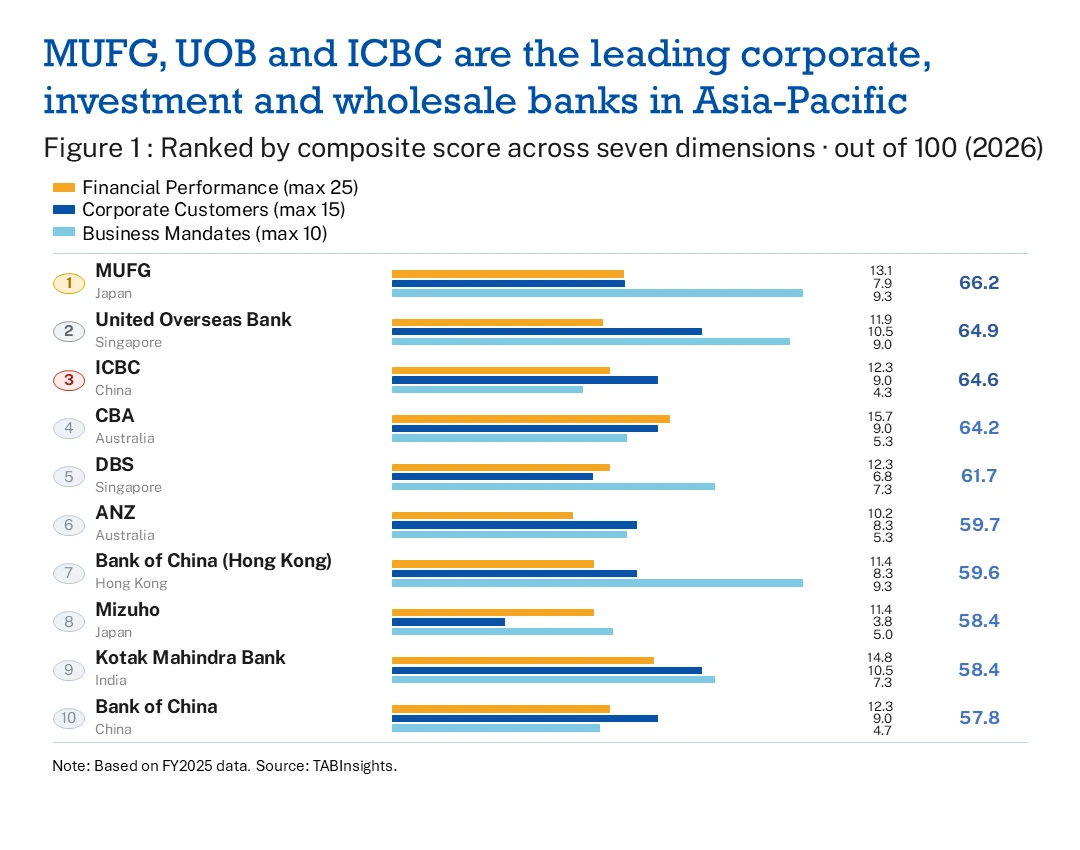

Japan's largest financial group emerged as the top-ranked institution in the Asia Pacific (APAC) region in the 2026 TABInsights World's 100 Best Corporate, Investment and Wholesale (CIW) Banks Ranking, driven by advances across financial performance, risk management and brand reach rather than strength in any single dimension. APAC institutions collectively account for 38% of global CIW revenue in the 2026 ranking, the largest regional share globally, reflecting the region's sustained weight in institutional banking. The ranking evaluates banks across seven dimensions: corporate clients, digital journey, financial performance, business mandates, employees, brand strength and coverage, and risk management.

Mitsubishi UFJ Financial Group (MUFG) claims first place in the APAC ranking, supported by a network spanning more than 50 countries. The result reflects cumulative strength across the ranking's seven dimensions — particularly brand strength, geographic coverage and risk management — rather than financial performance alone. Its cost-to-income ratio (CIR) improved from 58% in FY2024 to 53% in FY2025, a meaningful shift for a Japanese bank where structurally elevated cost bases have historically constrained efficiency relative to ASEAN peers, and one that signals operational restructuring rather than a transient adjustment. Revenue grew 4%, with transaction banking accounting for 49% of total CIW revenue, underscoring the group's ability to drive revenue growth and improve cost efficiency simultaneously.

United Overseas Bank (UOB), Singapore's anchor institutional bank and the Southeast Asian counterpart to MUFG's regional advance, holds second place with a perfect score in the digital journey dimension and a CIR of 27%. Its UOB Infinity platform deepens corporate client adoption across ASEAN, though revenue declined 7% in FY2025 reflecting broader Singapore market conditions, against a four-year compound annual growth rate (CAGR) of 10% between FY2021 and FY2024. A pre-tax return on assets (ROA) of 1.4% and non-performing loan (NPL) ratio of 1.7% confirm that franchise quality sustained returns through the revenue pressure.

The Industrial and Commercial Bank of China (ICBC) follows in third place, supported by the largest corporate online and mobile banking customer base in China at nearly 18 million customers and strong scores across business mandates and brand coverage. Revenue grew 5% in FY2025, while pre-tax ROA moderated from 1.3% to 1.0%, reflecting interest margin compression and slower corporate lending growth characteristic of China's large state-owned banking sector. The results reflect the ranking's multi-dimensional structure, where client franchise scale and brand coverage offset pressure on financial returns.

Commonwealth Bank of Australia (CBA) advances to fourth place on improving financial performance and corporate client metrics. Revenue grew 7% in FY2025, reflecting CBA's sustained reallocation toward higher-margin wholesale and business banking, where a 12% year-on-year expansion in business lending and AI-driven automation of credit processes materially reduced segment-level operating costs relative to income. DBS records a pre-tax ROA of 1.7%, the highest among the top five, advancing on the strength of a diversified ASEAN institutional franchise and improving financial performance across its corporate banking platform.

Bank Mandiri is the only APAC institution in 2026 to record improvement in revenue growth, profitability and asset quality within a single reporting period. The Indonesian bank delivers the strongest rank improvement in the region, underpinned by sustained investment in its Kopra by Mandiri wholesale platform, which covers cash management, trade finance and value chain solutions for corporate and institutional clients. CIW revenue grew 20% in FY2025 and pre-tax ROA improved from 2.2% in FY2024 to 2.3% in FY2025, while the NPL ratio fell from an already low 0.6% to 0.4%, reflecting active portfolio discipline rather than the correction of prior deterioration.

Beyond the top 10, India's four ranked institutions record the lowest average CIR among the APAC countries at 20%, with HDFC Bank at 17%, State Bank of India and ICICI Bank each at 19%, and Kotak Mahindra Bank at 25%. Yet HDFC Bank and Kotak Mahindra Bank both fell in the global ranking, indicating that CIR level alone does not determine ranking trajectory. A bank that optimises cost without investing comparably in digital capability and coverage will see its relative position erode even as absolute efficiency metrics remain strong. Their performance illustrates that operational efficiency must be paired with strategic investment to translate into ranking gains.

The 2026 results establish a consistent pattern: multi-dimensional improvement extends competitive lead; single-dimension gains give ground. The structural question for 2027 is whether mid-tier APAC banks can replicate the conditions that produced the Mandiri and MUFG results. Both institutions operated from positions of relative balance sheet strength and strategic autonomy, following investment across coverage, digital capability and cost discipline. For institutions where state ownership structures limit flexibility in capital allocation, or where domestic market concentration reduces the competitive pressure to invest across dimensions, the ranking gap is likely to widen before it narrows.

.png)

.png)

.webp)