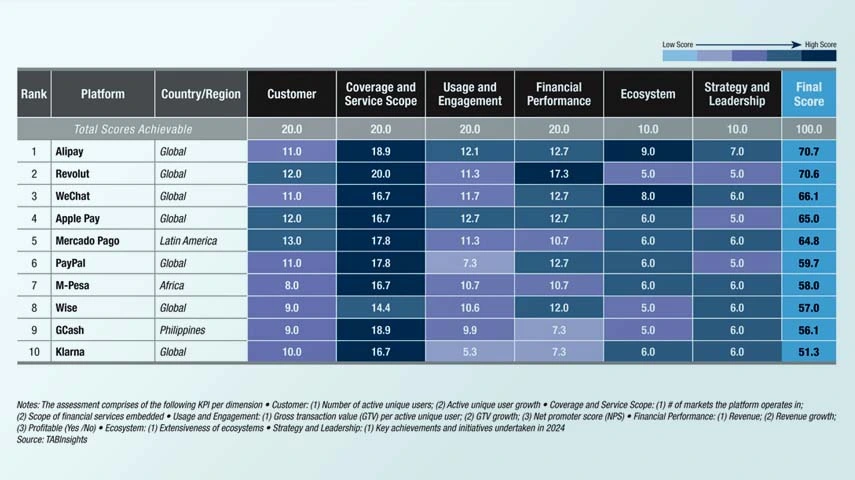

Alipay and Revolut maintain the top two positions in the 2026 TABInsights World’s Best Financial Platforms Ranking. Alipay operates at vast scale with a large user base and extensive ecosystem, while Revolut has achieved strong growth through customer expansion, deeper engagement, diversified revenue and ongoing market expansion. Financial platforms including WeChat, Apple Pay, Mercado Pago, PayPal, M-Pesa, Wise, GCash and Klarna are also among the top 10.

Platforms are evaluated across six balanced scorecard dimensions: customer, coverage and service scope, usage and engagement, financial performance, ecosystem integration and strategy and leadership. Key metrics include active users, transaction value and revenue, along with their growth, as well as market coverage, service breadth and ecosystem scale.

Ecosystem integration and financial inclusion drive continued growth

Financial platforms continue to experience robust growth, reflected in rising customer bases, market penetration, transaction volumes and values, and revenue. This growth is driven by multi-service offerings that deepen engagement and enable cross-selling, technologies that automate operations and support smarter decision-making, accelerated digital adoption that increases platform usage, and expansion into new markets and partnerships that broaden reach and strengthen networks.

In emerging markets, financial platforms extend access to underserved populations. Platforms such as GCash, TrueMoney and Grab in Southeast Asia, M-Pesa in Africa and Mercado Pago in Latin America reach large segments of unbanked or underbanked users by integrating multiple financial services within mobile applications. In mature markets, integrated ecosystems and advanced financial products deepen engagement and increase transaction frequency.

Revolut exemplifies this growth, expanding from 26.2 million customers in 2022 to more than 70 million across 40 markets by early 2026. Transaction value rose 58% and revenue grew 95% in 2023, followed by continued strong growth in 2024 with transaction value increasing 52% and revenue rising 72%, supported by diversified services and multi-market expansion. Despite this scale, market penetration remains around 15% of the adult population, indicating significant growth potential.

AI and data-driven ecosystems reshape platform economics

Artificial intelligence (AI) is increasingly embedded in platform operations, improving unit economics and enabling scalable growth. Customer support, onboarding and dispute resolution are increasingly automated, allowing user bases to expand without proportional increases in operating costs. Revolut applied generative AI, limiting customer support cost growth to 5% in 2024 despite a 38% increase in its customer base, while also deploying AI tools for financial crime monitoring and compliance. Similarly, Mercado Pago’s AI Assistant handled over 9 million customer interactions in the fourth quarter of 2025, resolving 87% without human intervention. Klarna integrated AI across internal operations, automating tasks equivalent to 853 full-time roles while maintaining stable costs amid revenue growth.

AI also supports product expansion within platform ecosystems. Data from payments, merchant activity and digital interactions enables platforms to extend credit, insurance and investment services with more precise risk assessment.

Ecosystem integration underpins the economic model of financial platforms. Payments typically serve as the entry point, attracting large user bases and merchant networks. Platforms then expand into lending, investment, insurance and merchant services, using transaction and behavioural data to support cross-selling. These services generate diversified revenue streams including lending spreads, transaction fees, subscriptions and value-added merchant services.

Alipay illustrates this approach. Through Alipay+, the platform connects more than 40 digital wallets and banking applications, supporting cross-border payments and linking merchants, consumers and financial institutions across more than 100 markets. AI-driven payment technologies further extend this ecosystem.

Cloud-native infrastructure and API-based architectures support this model, enabling financial services to be embedded into commerce, mobility and digital marketplaces. Modular systems allow platforms to integrate multiple financial services into third-party applications while maintaining real-time data processing and risk monitoring.

Ecosystem-based competition intensifies

Competition among financial platforms is increasingly ecosystem-based rather than product-based, as platforms integrate multiple services to deepen engagement, while partnerships, mergers and alliances expand capabilities and distribution.

Structural differentiation is becoming more pronounced. Large platforms benefit from scale and ecosystem integration, specialised providers compete in niche areas and mid-sized platforms face increasing pressure from technology, compliance and ecosystem investment requirements. Capital markets are also placing greater emphasis on sustainable profitability and disciplined unit economics.

Competition in Southeast Asia and Latin America is particularly intense due to large unbanked populations and rapidly expanding digital economies. Southeast Asia hosts a dense ecosystem of platforms, including Grab, Sea, GoTo, GCash, Maya, TrueMoney, DANA, Touch ‘n Go and MoMo, competing across payments, lending, investments and other financial services. Digital banks are rapidly expanding in both regions, adding further pressure to the competitive landscape. In Latin America, Mercado Pago faces strong competition from digital banks and platforms such as Nubank, PicPay, Inter, Neon and Ualá, alongside new entrants including Revolut.

Local adaptation and partnerships drive global expansion

Leading platforms balance global operating standards with tailored local strategies in their expansion. Strategic partnerships and ecosystem integration accelerate market entry. Alipay collaborates with local wallets and merchants across Southeast Asia, Europe and Latin America to support cross-border and local payments. PayPal maintains a unified global payment network while adapting to regional regulations and consumer preferences. Wise provides standardised cross-border transfers and low-cost foreign exchange services worldwide, supported by local currency infrastructure and regulatory compliance.

In emerging markets, financial services expand inclusion through local adaptation. Platforms such as M-Pesa in Africa and Mercado Pago in Latin America offer mobile accounts, payments, credit and other services tailored to underserved populations, adjusting to local needs and driving broad adoption.

Regulatory compliance supports sustainable growth

Regulatory compliance has become a strategic capability for financial platforms. Platforms operate within complex frameworks covering payments, lending, Buy Now Pay Later (BNPL) services, digital identity, data protection and cross-border transactions. Compliance increasingly shapes product design, risk management and long-term strategy.

In the US, regulators focus on AI transparency, algorithmic decision-making and real-time Anti-Money Laundering (AML) and Know Your Customer (KYC) monitoring. The European Union enforces frameworks including Payment Services Directive 3 (PSD3), the Digital Operational Resilience Act (DORA) and the AI Act, requiring stronger ICT risk management, incident reporting, third-party oversight and AI accountability. Digital identity solutions, such as the European Digital Identity Wallet, are reshaping KYC processes, while extensions to the GDPR reinforce privacy and algorithmic governance.

Asia-Pacific regulatory approaches vary. China supervises lending, wealth management and banking partnerships for platforms such as Alipay and WeChat. India promotes RegTech adoption and regulatory sandboxes for platforms including PhonePe and Paytm. Southeast Asian platforms such as Grab, DANA and TrueMoney face licensing and operational requirements across payments and digital lending.

Platforms embedding compliance into product design and deploying RegTech solutions for monitoring and reporting are better positioned to manage legal and reputational risk while sustaining innovation and growth.

Top financial platforms reflect diverse strategies and business models

Alipay, Revolut, WeChat Pay, Apple Pay, Mercado Pago, PayPal, M-Pesa, Wise, GCash and Klarna rank among the top 10 financial platforms. Other financial platforms such as PhonePe and Paytm in India, DANA in Indonesia, PayPay in Japan, Toss and Kakao Pay in South Korea and MoMo in Vietnam are also accelerating the use of digital financial services across their respective markets.

These platforms adopt strategies shaped by technology, user engagement, regional dynamics and regulatory environments. Their operating models differ, with some embedding financial services into daily life through comprehensive ecosystems, others focusing on global payments and cross-border infrastructure, while regional platforms scale digital finance in local markets.

Alipay and WeChat embed financial services into everyday digital ecosystems

Alipay operates as a comprehensive financial super-app, offering extensive financial and AI-driven services with a strong global presence. Its international expansion through Alipay+ supports 1.5?billion consumer accounts and 150?million merchants across more than 100 markets. Launched in 2025, AI Pay enables users to complete purchases through AI agents across apps, mini-programs and smart devices. In early 2026, AI Pay processed over 120?million transactions in a single week, becoming the first AI-native payment solution to reach this scale. Meanwhile, Alipay Tap! exceeded 100?million daily transactions, reflecting rapid adoption of AI-driven payments in China’s intelligent digital payment ecosystem.

WeChat leverages its social ecosystem to anchor a major digital financial platform. With over 1?billion monthly active WeChat Pay users and 1.2?billion daily transactions, it supports peer-to-peer transfers, merchant payments, and mini-programs for wealth management, insurance, and cross-border services. WeChat mini-programs attract over 946?million monthly users across commerce, travel, and utilities, while partnerships with licensed financial institutions ensure financial products are distributed within regulated frameworks.

Revolut, Wise, Klarna, Apple Pay and PayPal expand cross-border and embedded financial services

Revolut, Wise, Klarna, Apple Pay and PayPal are transforming cross-border payments and embedded financial services through scalable, technology-driven models. They prioritise international transactions, multi-currency accounts, embedded finance and ecosystem integration, enabling efficient financial experiences for consumers and businesses.

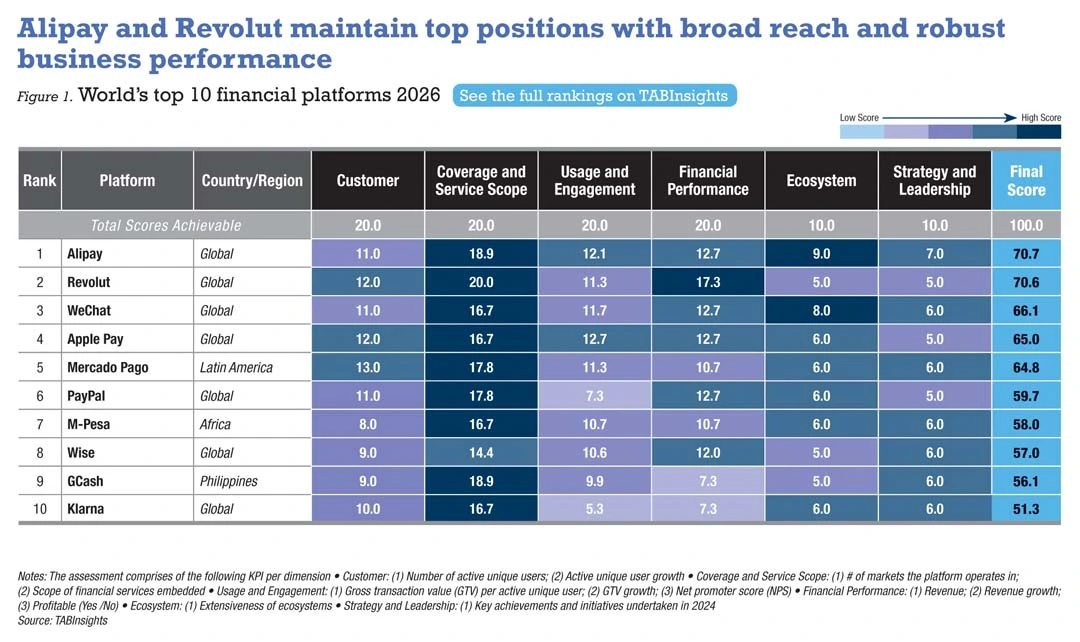

Revolut remains second in this year’s ranking, supported by its market presence, diversified revenue streams and integrated product ecosystem. In 2024, monthly active users grew 42% in the retail segment and 56% in business banking. Transaction value reached $1.3?trillion in 2024. Revolut recorded the highest transaction value per user at $24,342, while transaction value per active user is even higher, estimated at above $30,000. Revenue grew 72% to $4?billion, with a net profit margin of 26%. Card payments, interest income, foreign exchange, subscriptions and wealth management all posted strong growth, with business banking contributing around 15% of total revenue.

Revolut’s strategy focuses on international expansion, becoming primary provider for users and strengthening security and operational reliability. The platform operates in around 40 markets, targeting growth from 70 million to 100 million users by mid-2027 and entry into 30 additional markets by 2030. Regulatory complexity, compliance costs, competition and cryptocurrency restrictions pose ongoing challenges.

Wise operates an efficient, low-cost model focused on international transfers and multi-currency accounts. Its ecosystem includes debit cards, business payments, investment products and the Wise Platform infrastructure for banks and financial institutions. Active customers increased 21% to 15.6 million in the financial year (FY) 2025, while cross-border transaction value rose 23% to $185 billion, supporting 16% underlying income growth. Compared with four years earlier, both active customers and transaction value more than doubled.

Klarna has evolved from a pure BNPL provider into a broader financial platform, with active consumers growing from 84 million in 2023 to 118 million in 2025 and active users of financial services beyond payments doubling to 15.8 million, generating $107 per user annually compared with $30 for typical BNPL users. In 2024, it achieved its first full-year profit since 2019, supported by cost reductions, AI-driven operations and tighter risk management. Despite this growth, profitability remains uneven as the platform balances rapid expansion with sustainable growth.

Apple Pay and PayPal leverage network effects and transaction data to expand services. Apple Pay emphasises ecosystem-driven adoption and efficiency, while PayPal faces market saturation, slower user growth and fee compression. Apple Pay operates in 89 markets with over 11,000 banking partners, offering Apple Cash, Apple Card and installment financing to deepen user engagement and broaden financial offerings while maintaining a low-risk, scalable model. PayPal connects 439 million active accounts across PayPal, Venmo and Xoom, with merchant solutions, savings, invoicing and embedded finance offerings, processing $1.8 trillion in payment volume in 2025.

Mercado Pago, M-Pesa and GCash expand digital finance in regional markets

Some of the most influential platforms are concentrated regionally, scaling rapidly by responding to local regulation, consumer behaviour and financial access gaps. Mercado Pago, the fintech arm of e-commerce giant MercadoLibre, has expanded rapidly across Latin America. Monthly active users grew from 45.8 million in the fourth quarter of 2023 to nearly 78 million by the fourth quarter of 2025. Total payment value increased 34% in 2024 and 41% in 2025 to $278 billion, with revenue growing 25% in 2024 and 46% in 2025 to $12.6 billion. Assets under management rose sharply to nearly $19 billion in 2025 as savings and investment services expanded. Credit portfolios advanced 74% in 2024 and 90% in 2025 to $12.5 billion, primarily through credit cards, requiring close risk monitoring amid macroeconomic volatility.

M-Pesa, operated by Vodacom and Safaricom, remains Africa’s largest mobile financial service. Across all markets where M-Pesa and Vodacom’s VodaCash platform operate, transaction value reached $450.8 billion in FY2025, up 18.3% year-on-year. The platform served 87.7 million mobile financial services customers, with revenue increasing 17.6% in FY 2025, supporting Vodacom’s Vision 2030 goal of expanding to 120 million customers.

GCash is the leading financial platform in the Philippines, with over 81 million active users. Around 90% of users are from lower socio-economic segments. It has expanded its financial services to include savings, credit, investments, insurance and cross-border services. GCash has also expanded internationally, providing payments in over 50 countries and digital financial services to overseas Filipinos in 16 markets.

Looking ahead, ecosystem integration, AI and technological innovation, geographic expansion and financial inclusion will continue to drive growth of financial platforms. Multi-service offerings and automation enable platforms to scale efficiently, deepen engagement and diversify revenue. Local adaptation and regulatory compliance remain essential for sustainable expansion.

View the full World’s Best Financial Platforms Ranking here

.png)

.webp)