The wealth management industry is potentially undergoing a structural reconfiguration, driven not by digitisation but by a shift in the client interface layer. Around 200 million people now ask ChatGPT personal finance questions each month, according to OpenAI's announcement alongside its 15 May release. More than 75% of Perplexity users also ask financial questions. The scale is what matters. The natural language interface that hundreds of millions already trust is now being connected directly to their financial lives.

Through a read-only Plaid connection to more than 12,000 institutions including Chase, Schwab, Fidelity, American Express and Capital One, the model can read balances, transactions, holdings and recurring payments and then reason across them through conversation. The account aggregation services that once scraped this data are becoming obsolete. What has changed is that AI platforms are beginning to hold the conversation around it.

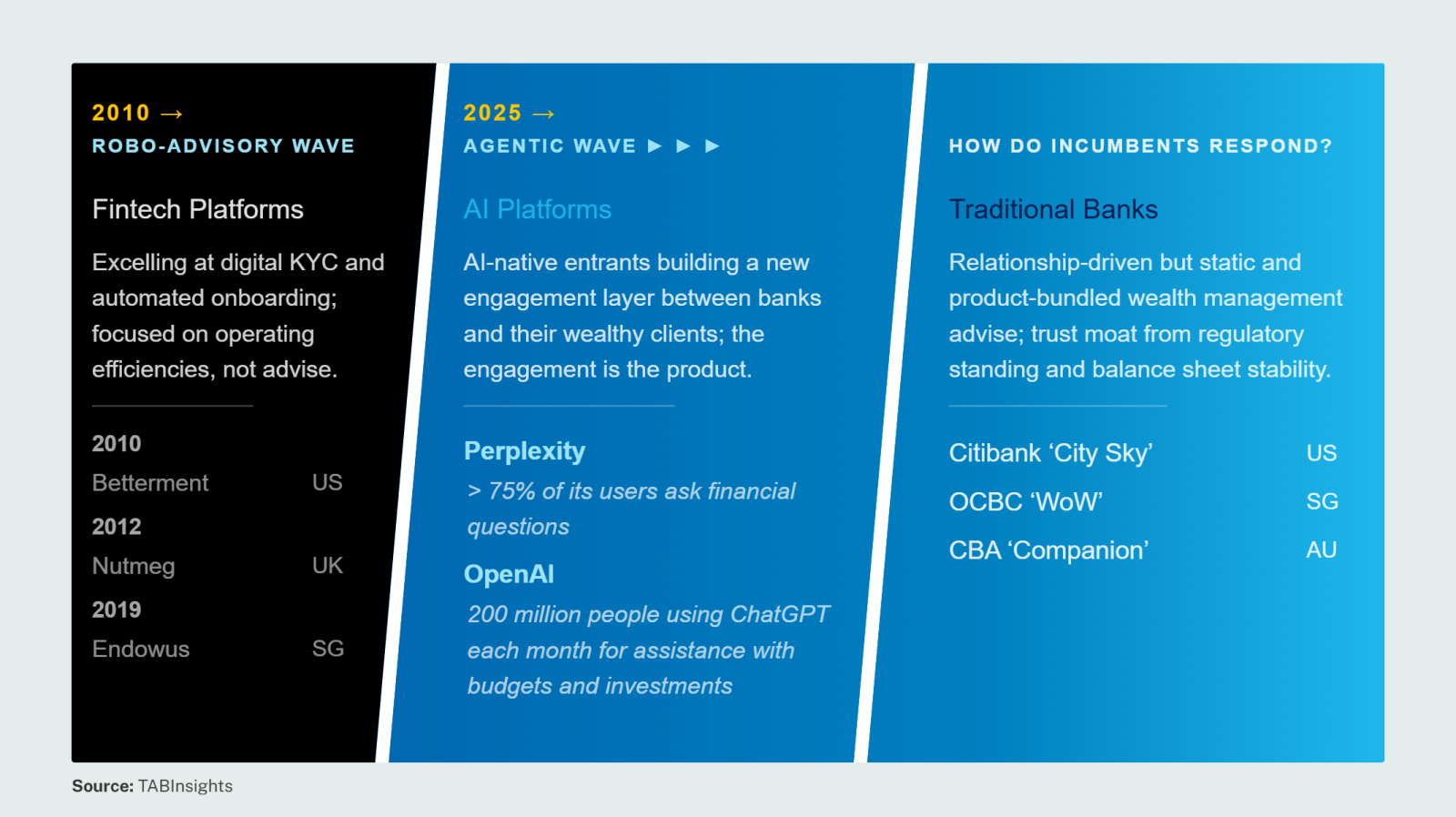

The industry has moved beyond the 2010 robo-advisory wave, which focused on onboarding efficiency and rules-based portfolio allocation, into a 2025 era of agentic AI, where platforms increasingly interpret, aggregate and act on a client's entire financial life. This shift is not merely technological but relational. The centre of gravity is moving from product distribution to conversational control of financial decision-making.

Historically, banks successfully defended their wealth franchises against robo-advisers, which rose to prominence from 2010 onwards. These platforms struggled to meet the complex needs of private banking clients. Their strength lay in operational efficiency rather than advice, with a competitive proposition built on lower costs and lower assets-under-management (AUM) entry thresholds.

Robo-platforms excelled at frictionless onboarding and low-cost portfolio construction, but they struggled to build on these advantages. They failed to deliver the advice customers wanted, improve investment decisions or meaningfully connect investors' goals and financial circumstances to tailored recommendations.

After more than a decade in the market, robo-advisers remain small in AUM compared with banks and are unlikely to survive in their current form unless they reposition around higher-value advisory capabilities. That is precisely the gap AI-driven platforms are now beginning to fill.

From robo-platform limitations to agentic capabilities in wealth management

The agentic AI wave represents a fundamentally different proposition. Unlike robo-advisers, AI-native platforms are increasingly capable of synthesising multidimensional financial data, including income, liabilities, spending behaviour, market exposure and macroeconomic signals, into continuously updated financial narratives. Rather than producing portfolio recommendations at fixed intervals, these systems deliver adaptive, always-on financial guidance. The implication is structural. The interface through which individuals manage their financial lives is shifting from the banking app to the AI layer.

The key disruption lies in what Emmanuel Daniel describes as the transition from a model in which the product is the focus to one in which the conversation itself becomes the product.

Traditional shortcomings of the banking advisory model

Banks are structurally exposed to this shift for three reasons.

First, banks have traditionally found it difficult to separate advice from product distribution, making genuine impartiality challenging. Traditional financial institutions have been trying to figure out how to reconcile fiduciary advice with pushing a product. Second, legacy advisory models are episodic rather than continuous. Relationship managers (RMs) typically engage with clients quarterly or semi-annually, creating delays in responding to changes in markets, tax regimes or client cash flows. AI systems, by contrast, operate continuously, updating recommendations in real time as new information becomes available.

Third, banks lack a unified data architecture capable of modelling the full complexity of clients' financial lives. While internal systems capture account-level information, they rarely integrate external behavioural signals, holdings across multiple institutions or significant life events into a coherent, continuously updated view.

The result is a widening information gap, with platforms such as OpenAI, Perplexity and Claude increasingly able to provide clients with a more complete, real-time picture of their finances than the institutions that actually hold their assets.

The emerging competitive response from banks

Banks are not passive in this transition, but their responses diverge into two strategic approaches: containment and integration.

The containment model is evident in institutions developing proprietary AI assistants within closed banking environments. Citibank's City Sky and OCBC's WoW, for example, allow affluent clients to query their financial positions and explore investment scenarios through conversational interfaces embedded within the bank's ecosystem. These tools are designed to extend advisory capacity, particularly for affluent and upper-affluent customers, where responsiveness and availability are critical to retaining relationships. The objective is to preserve the primary interaction layer within authenticated banking environments, reducing reliance on external AI platforms.

Leading banks are also embedding intelligence directly into their core banking interfaces, anticipating that the native banking app will evolve into a conversational, agentic environment at the centre of customer engagement. This trend is no longer confined to wealth management but is extending across the broader retail banking market. The Commonwealth Bank of Australia (CBA) is pursuing this direction through Companion, a conversational AI tool currently being tested with employees and selected business banking customers. Customers can ask natural language questions about spending, budgeting, home ownership and business cash flow, with AI generating responses in real time using live customer data.

The integration model, meanwhile, embeds bank data into third-party AI environments under controlled conditions. BBVA has agreed to allow ChatGPT users to access their banking data securely, while Grasshopper Bank enables business customers to connect read-only account data to Claude through the open Model Context Protocol (MCP), subject to explicit customer consent.

Across both approaches, banks are seeking to protect data sovereignty, maintain regulatory compliance and remain relevant as customers increasingly expect AI-powered access to their financial information.

At the same time, banks are using AI internally to scale human advice. DBS Singapore has increased the number of client meetings RMs can conduct from around four to six per week to between 10 and 15, enabling the bank to assign dedicated wealth managers to selected emerging affluent customers.

The wealth management value chain is being reorganised

The wealth management value chain is once again being reshaped around a new hierarchy, moving from intelligence to conversation and ultimately to execution.

In this emerging landscape, banks are likely to face growing competition from players such as OpenAI as wealth management shifts away from branch-based relationship management towards AI-enabled platforms. This creates a strategic dilemma. Banks will need to collaborate with leading AI providers to improve and streamline client services while simultaneously preparing to compete with those same platforms as they expand into core advisory activities. Even if banks retain custody of assets and responsibility for execution, the greater risk is the gradual loss of influence over the client relationship and the decision-making process, as advice, intent formation and product discovery increasingly migrate to AI-native interfaces outside the traditional banking channel.

Subscribe for regular insights.

.png)

.webp)