Global retail banking is navigating a complex operating environment, shaped by slowing interest rate cycles, rising cost pressures, increased digital competition and shifting customer expectations. In response, banks are adapting their business models in three consistent ways: deepening their retail deposit bases to reduce funding costs and create cross-selling opportunities, investing in digital infrastructure to automate processes and shift more revenue towards retail fee income, and deploying artificial intelligence (AI) tools to improve operational efficiency and credit decision-making — with digital channels such as payments, cards and wealth products becoming primary drivers of fee income diversification.

The 2026 TAB Global World’s Best Retail Banks Ranking provides a data-driven assessment of how the world’s top 100 retail banks are executing against these objectives. Based primarily on publicly reported results for the first half (1H) of 2025, with comparative data from 1H24, the rankings evaluate banks across seven key dimensions: retail financial performance, retail focus, digital capability, brand strength, digital sales, customer experience and risk management. This assessment highlights trends in revenue growth, funding structures, cost management and digital engagement, providing insights into how banks are responding to an evolving landscape.

Top 10 banks favour digital depth over breadth

Bank of China (Hong Kong) (BOCHK) leads the TAB Global World’s Best Retail Banks Ranking 2026, scoring 61.9 out of 100. BOCHK’s financial results include 16.6% revenue growth in 1H25, a 2.6% return on assets (ROA), and a cost-to-income ratio (CIR) of 36.8%. The results are closely linked to structural reforms within Hong Kong’s banking sector under the Hong Kong Monetary Authority’s Fintech 2025 agenda, which has facilitated open APIs, sandbox experimentation and wider digital adoption across both retail and corporate banking. BOCHK’s involvement in initiatives such as Project Ensemble, a sandbox for wholesale central bank digital currency and tokenised assets, has enhanced its payments and settlement infrastructure, streamlined transfers and enabled digital onboarding for customers.

Despite only 36% of its customers being digitally active, BOCHK’s digital channels now account for 65% of retail sales — a ratio that reflects engagement quality over sheer user volume. The Greater Bay Area (GBA) Wealth Management Connect scheme has further expanded the bank’s digital wealth platforms, deepening relationships with mass affluent and high-net-worth customers across Hong Kong, Macau and mainland cities while boosting fee income. A stable local deposit base underpins both lending and wealth advisory activities. Together, these factors drive BOCHK’s scores in financial performance, sales management and risk metrics.

Emirates NBD and First Abu Dhabi Bank (FAB), ranked second and third respectively, illustrate how large Gulf banks are leveraging deposit growth, current account and savings account (CASA) ratios, and AI-enabled digital ecosystems to strengthen their retail positions. Emirates NBD saw 19.3% growth in retail deposits in 1H25, alongside a CASA ratio of 57%, providing a low-cost funding base that supports lending and fee income. Over 98% of new customers are onboarded digitally, with more than 90% of transactions handled through digital channels. AI-driven personalisation and analytics have further enhanced credit decisioning and increased cards and fee income.

FAB follows a similar path, combining a retail deposit franchise with AI-enabled lending and debt management platforms that provide real-time portfolio insights to support pricing and risk segmentation. AI agents across operations, customer service and finance workflows have reduced manual processing and supported consistent credit decisions, reinforcing FAB’s positions in risk management and sales management.

JPMorgan Chase scores strongly in sales management and brand strength, serving over 66 million American households through its mobile app. Hyper-personalisation from spending data sustains its competitive metrics at scale. In 1H25, Chase reported a CIR of 53.1%, marginally up from 52.9% in 1H24.

DBS reported 30% of revenue from fee income in 1H25, up from 26% in 2024, maintaining consistent brand positioning and sales discipline during its transformation. NatWest achieved 16.5% revenue growth in 1H25, reducing its CIR from 54.6% to 45.4%.Kuwait Finance House (KFH) rounds out the top 10, scoring highly in risk management through its RiskGPT platform, developed with Microsoft, which reduces credit evaluation times from days to under one hour. Its digital-only Tam bank has driven 13% growth in personal finance and enabled real-time onboarding, demonstrating how Islamic retail banks are using digital channels to deepen customer engagement.

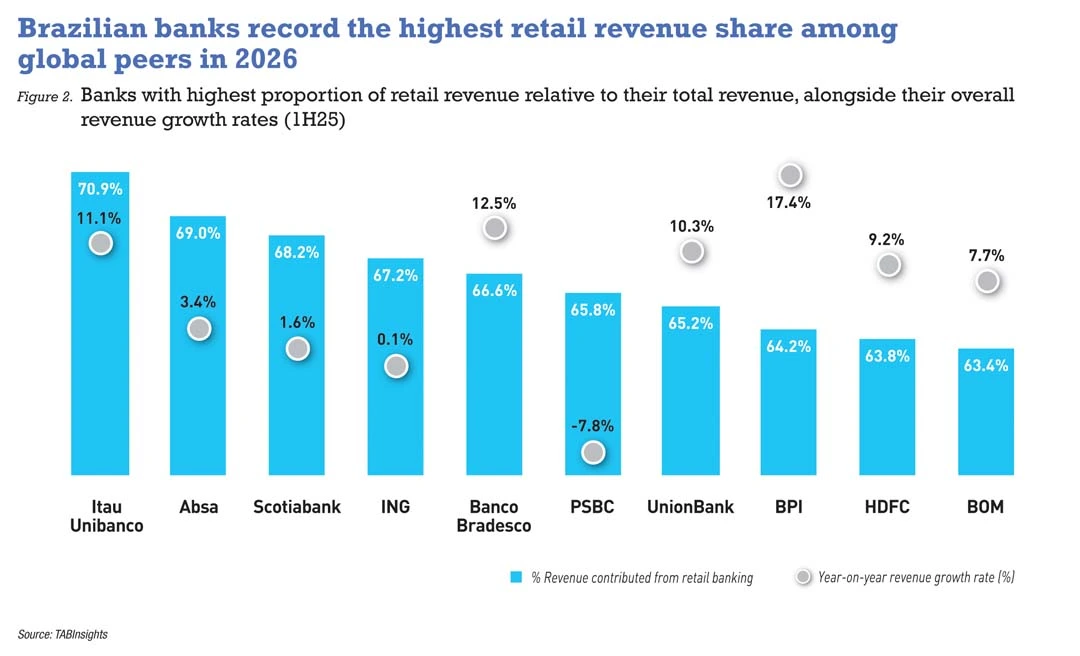

Retail revenue share splits along growth and margin lines

The retail focus score measures the proportion of each bank’s total book accounted for by retail customers — an indicator of sensitivity to deposit dynamics, consumer credit trends and cross-selling depth. High retail revenue share combined with growth signals successful monetisation; high share with declining growth may point to structural margin pressure.

Itaú Unibanco leads the retail-focused cohort, recording 70.9% of revenues from retail banking and 11.1% year-on-year (YoY) growth in 1H25, supported by long-term investment in cloud infrastructure and data platforms. The bank has migrated around 60% of its workload to Amazon Web Services, cutting deployment cycles from months to days and reducing customer-impacting incidents by 98% — enabling more frequent product releases without compromising stability. This agility underpins a retail model that blends loans, cards, payments and wealth products within a “super app” environment, allowing the bank to capture more fee income as customers consolidate financial activity within a single ecosystem.

Banco Bradesco shows a similar pattern, with a retail revenue share of 66.6% and 12.5% growth. High domestic interest rates have supported margins, while continued investment in digital channels has shifted more customer activity to self-service and remote advisory, reducing unit costs as volumes rise. This combination of retail specialisation, fee-driven income and digital scalability underpins the high retail revenue shares recorded by Brazilian institutions in the rankings.

Postal Savings Bank of China (PSBC) demonstrates how macroeconomic and policy factors can weigh on retail growth even within a heavily retail-oriented franchise. Despite 65.8% of revenues from retail, YoY growth fell 7.8%, reflecting margin compression from interest rate reductions and cautious household sentiment. The pressure is prompting Chinese banks to reexamine their mix of loan growth, deposits and fee-based activities, and to accelerate digital initiatives that support revenue diversification beyond traditional interest income.

Philippine banks UnionBank and BPI illustrate how a young, mobile-first customer base and rapid adoption of digital payments can support both retail focus and growth. UnionBank’s 65.2% retail revenue share and 10.3% growth, alongside BPI’s financial performance, demonstrate how digital channels are becoming the primary distribution layer for everyday banking, payments and wealth solutions. In India, HDFC Bank’s 63.8% retail revenue share and 9.2% growth reflect a resilient position in a competitive market, where private sector banks are leveraging UPI, data-driven credit and branch-light expansion to sustain growth while managing funding costs and asset quality.

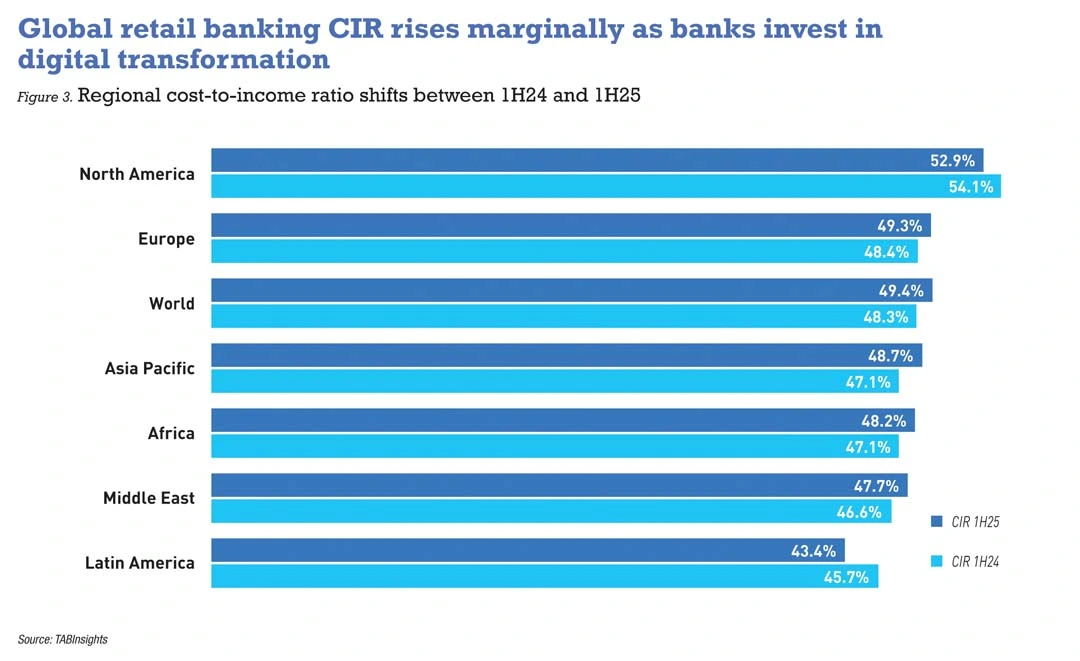

Regional CIR shifts reflect divergent investment cycles

Cost discipline is crucial to retail banking competitiveness. The global average CIR increased from 48.3% in 1H24 to 49.4% in 1H25, with regional patterns showing both improvements and increases. In North America, CIR decreased from 54.1% to 52.9%, driven by efficiency programmes and AI-led automation at large institutions — JPMorgan Chase, for example, maintained its CIR at around 53% through the period.

In Europe, CIR edged up from 48.36% to 49.34%, largely due to higher staff expenses, legacy system transformation and regulatory compliance. NatWest is a notable exception: its $1.6 billion investment in AI, process simplification and cloud migration reduced its CIR from 54.6% to 45.4%. ING and Rabobank benefit from direct banking and digitally intensive models, though flat or modest retail revenue growth in some markets reflects ongoing competitive and rate pressures.

Latin America recorded the largest CIR improvement, from 45.70% to 43.40%, driven by digitalisation and the ability to extract more value from high-rate environments. Itaú Unibanco held a CIR of 46.2% despite continued investment in AI-driven credit management and cloud infrastructure. In Singapore, DBS similarly uses AI and machine learning to reduce costs while growing revenue, attributing around $746 million in economic value to its AI initiatives as of end-2025.

In the Middle East, Africa and Asia Pacific, modest CIR increases reflect major investment cycles in progress. Banks such as Emirates NBD and FAB are scaling AI across multiple functions, while DBS, OCBC and Indian private-sector banks modernise systems and expand digital distribution. Qatar Islamic Bank (QIB) achieved the lowest CIR in the ranking at 16.85% in 1H25, down from 17.04% in 1H24, driven by cost management and digital efficiencies.

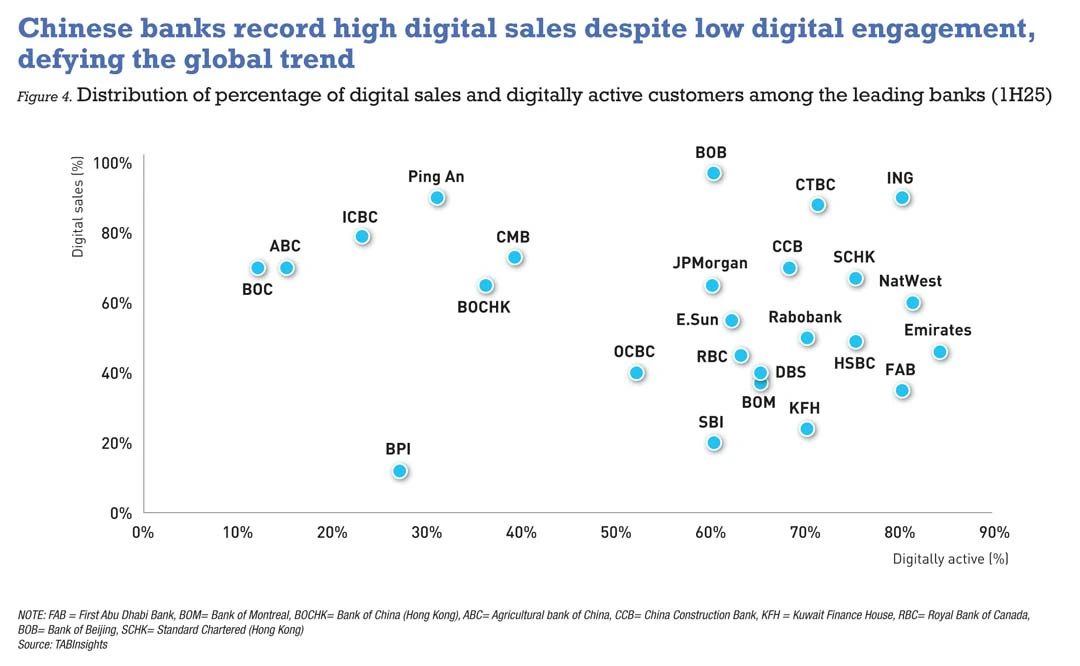

Digital capability connects deposits, engagement and revenue mix

Digital capability is evaluated through the percentage of digitally active customers and the proportion of digital sales. Banks that score highly on both measures typically show a closer link between deposit growth, customer engagement and fees and commission income relative to pure interest income.

Emirates NBD’s 84% digitally active customer base and FAB’s 80% support cross-selling across cards, personal loans, wealth products and payments — turning deposit accounts into platforms for deeper engagement rather than mere funding sources. Standard Chartered and DBS report similarly strong digital metrics, underpinned by sustained investment in AI and data platforms that personalise interactions and automate service journeys.

A broad positive correlation between digital activity and digital sales is evident across the rankings. ING, with 80% digitally active and 90% digital sales, and CTBC Bank, with 71% digitally active and 88% digital sales, represent highly digitalised retail franchises where most new product acquisition occurs through mobile and online channels — reducing acquisition costs and allowing banks to shift uptake toward higher fee, lower-capital products.

Chinese banks present a more nuanced picture. China Merchants Bank reports only 39% digitally active customers yet achieves 93% digital sales, driven by high adoption of digital payments and wealth platforms. The pattern suggests some institutions prioritise digital integration in specific high-volume journeys, such as payments and investment subscriptions, rather than universal adoption across the full customer base.

Regional strategies reflect divergent starting points

The Middle East is a rapidly rising region in the rankings, with Emirates NBD, FAB and KFH combining strong low-cost deposit bases with heavy investment in AI-driven systems, while Qatar and Saudi Arabia are expanding their retail sectors through institutions such as QIB, Mashreq and Al Rajhi, supported by government-led digital inclusion initiatives including Vision 2030.

In Asia Pacific, Hong Kong consolidates its role as a fintech hub while Singapore leads in digital banking through DBS and OCBC. India’s mobile-first population is driving expansion in digital payments and credit via UPI, though financial literacy and credit infrastructure gaps remain constraints.

Latin America stands out for its retail focus and operational agility. Itaú Unibanco and Banco Bradesco leverage integrated “super app” ecosystems and cloud migration to improve efficiency. In Africa, Absa and Standard Bank are balancing infrastructure investment with profitability, focusing on inclusion in high-growth, cost-sensitive markets.

European banks continue to face margin compression, regulatory costs and competition from digital disruptors, though direct digital models such as ING’s provide structural resilience. North American banks maintain strong competitiveness on the strength of brand scale and customer relationship management, despite rising technology investment costs.

Digital investment widens the gap between leaders and followers

The TAB Global World’s Best Retail Banks Ranking confirms the interconnections between revenue mix, cost control and digital engagement across global retail banking. Banks with CASA ratios above 55% generate higher retail fee income from cards, wealth products and payments, as stable deposits support effective cross-selling. Retail-dominant institutions such as Itaú Unibanco and Banco Bradesco convert these primary relationships into diversified revenue streams through digital platforms integrating lending, payments and advisory services.

Global CIR rose from 48.3% to 49.4%, continuing the pattern where technology investments have begun to outweigh early efficiency gains. Latin America recorded the largest improvement , falling to 43.4% alongside cloud infrastructure adoption. North America and Europe saw modest CIR increases to fund AI-driven personalisation and automation, while the Middle East and Asia Pacific saw rises amid digital ecosystem expansion.

Banks with over 80% digital sales record stronger sales management performance and higher fee income contributions than those with under 65%. Chinese banks exemplify this by concentrating digital investment in payments and wealth management rather than pursuing broad adoption across all customer segments.

The 2026 data introduces a tension: digital capability leaders now experience faster increases in CIR than peers. Where digital adoption correlated with uniform CIR declines in 2025, banks at the forefront of transformation this year face AI and cloud costs that temporarily outpace efficiency benefits. JPMorgan Chase, Emirates NBD and Standard Chartered Hong Kong, once top performers, now trail BOCHK, which maintains lower CIR through more targeted digital investment.

Emerging markets such as Latin America and Africa currently benefit from lower CIR but face convergence risks as scaling digital ecosystems demand heavier technology spending. Whether accelerating retail fee income can offset these rising costs remains an unresolved dynamic in the evolution of retail banking.

View the full World’s Best Retail Banks Ranking here

.png)

.webp)