Research Notes

Jun 27

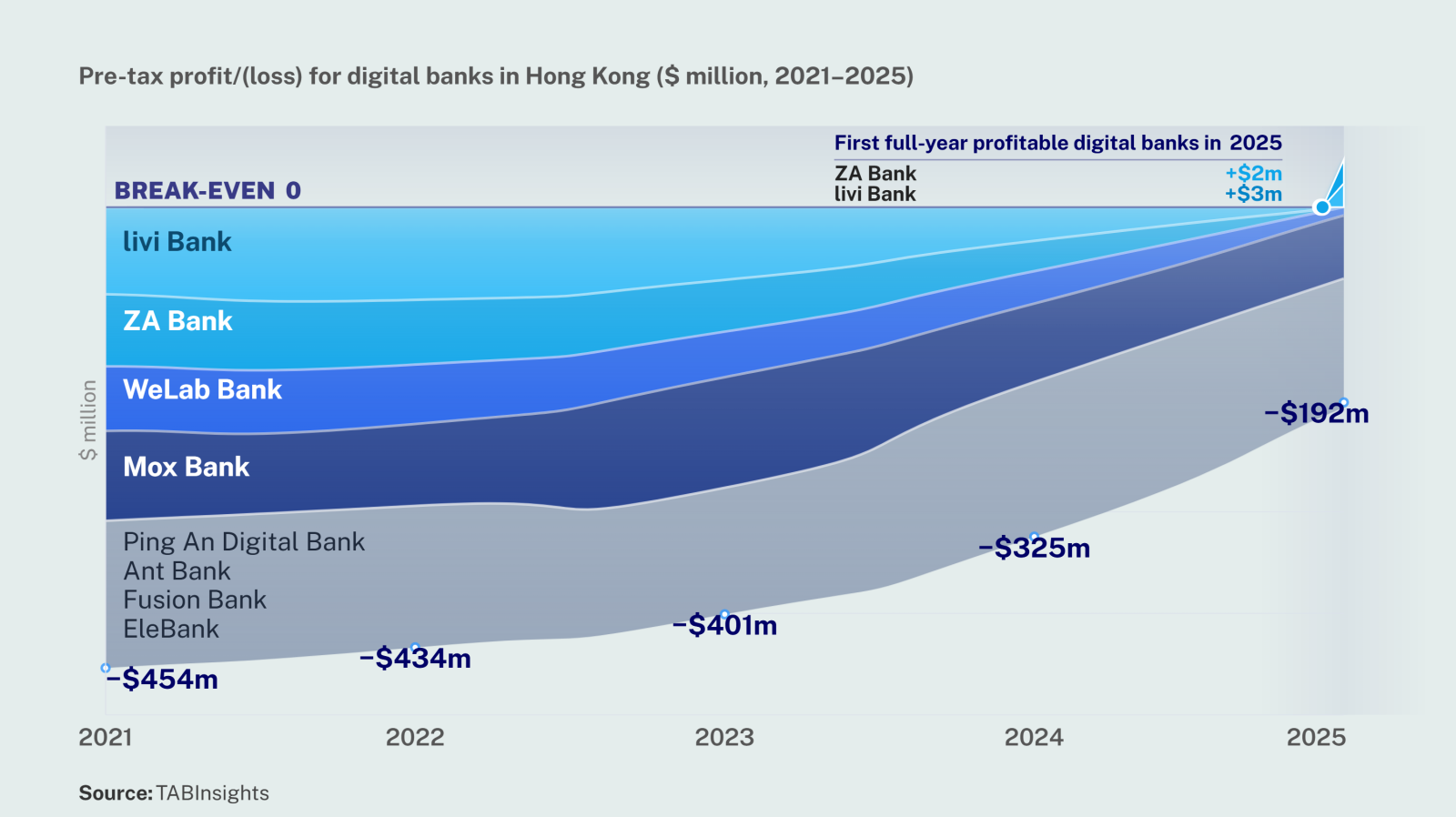

A year after Hong Kong issued eight digital banking licences, Mox and ZA Bank have emerged as the early leaders. Together with WeLab, the three banks account for 86% of all virtual banking deposit in Hong Kong.

.png)