Research Notes

Aug 22

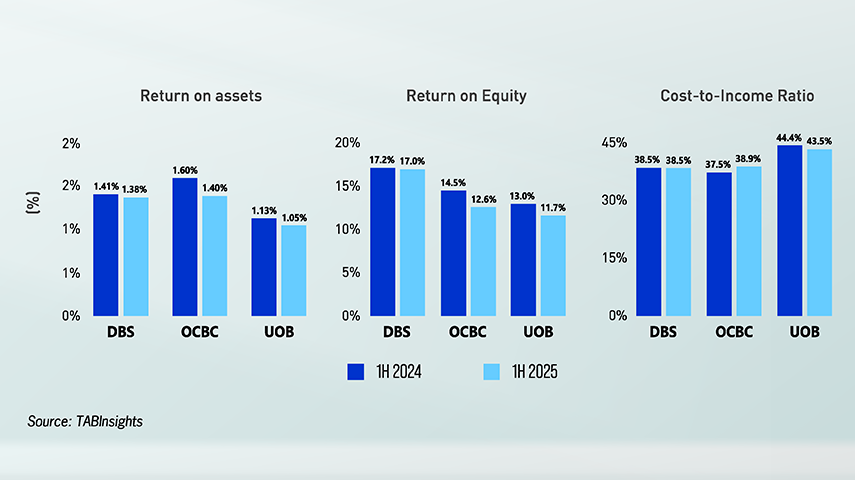

Singapore’s largest banks are shifting from margin-driven profits to growth anchored in wealth, regional connectivity and sustainable finance—building a model designed for resilience across market cycles.