Rankings

May 13

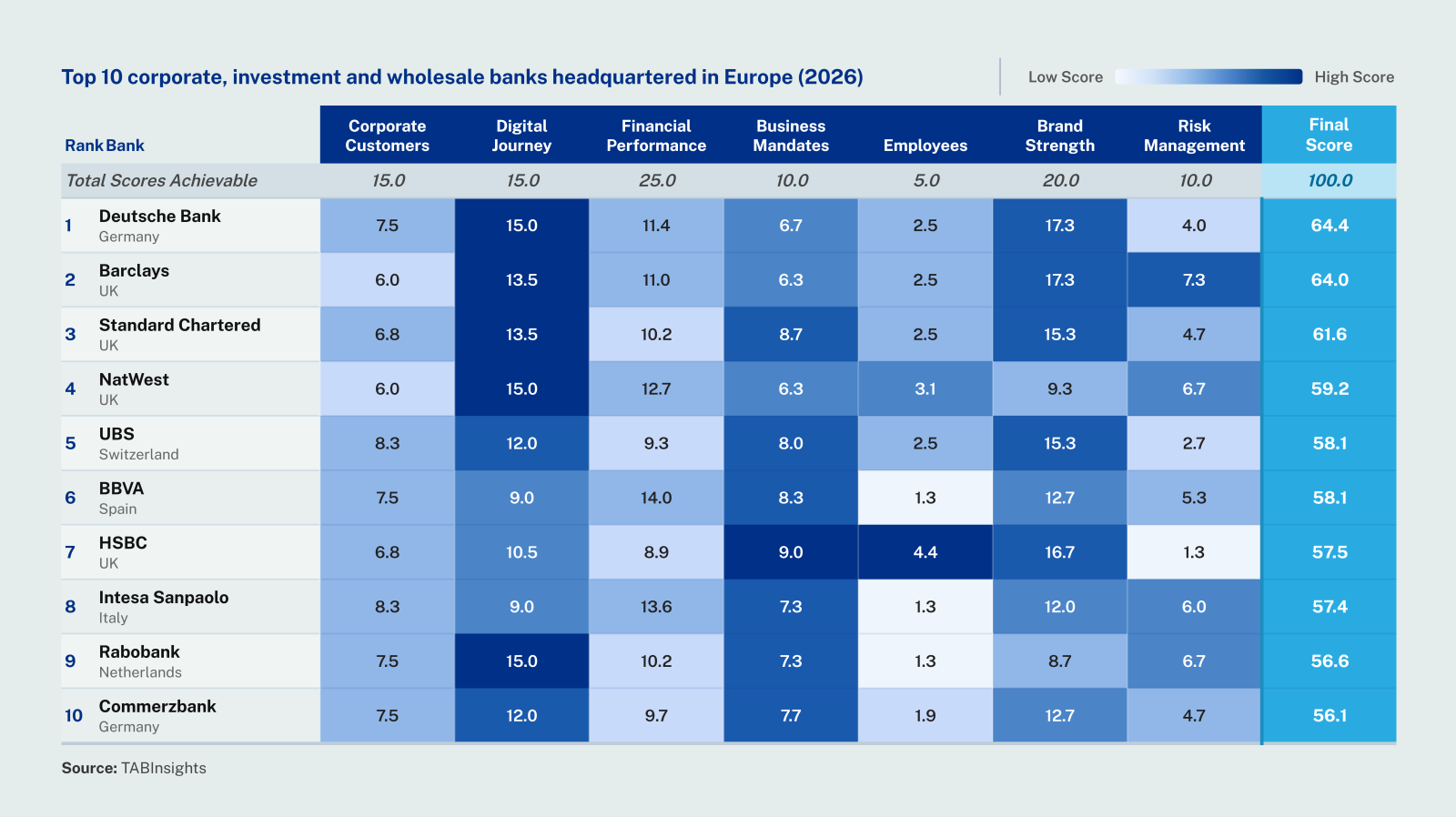

Global CIW banking has entered an execution phase, where rank movement is driven by improvement across multiple dimensions, while the efficiency gap between Middle Eastern and Western institutions widens

.png)

.png)