In this year’s Excellence programme, retail banking executives were acutely aware of the pressing need to steer their institutions towards a swift transformation on multiple fronts, both at the front and back end, to counteract the increasing signs of disintermediation.

They are confronted with a dual challenge: the imperative to partner with ecosystems that can expand their customers base beyond traditional segments, and a growing sense of unease as platforms, big tech and fintechs solidify their presence in the retail banking landscape, ditto owning the majority of customer relationships.

Banks recognised the urgency to double down on innovation, collaboration, speed, agility and customer-centricity to secure their relevance and survival in the future. TABInsights’ conversations with multiple banks reveal an increasing realisation of the importance of understanding and meeting genuine customer needs. Delivering solutions that are not only cost-effective and fast but also highly relevant, meaningful, and personalised within a secure environment has become paramount.

However, implementing such a vision is often hindered by well-known issues: legacy culture and infrastructure within banks, and disparate data systems. These slow down the process of developing future capabilities that would enable banks to compete more effectively.

Despite adapting to changing deposit needs, banks face two key challenges to sustain their deposit business. One is the impact of digital technologies in reshaping customer preferences, with the increasing popularity of consumers transacting with their digital wallets offered by platform players. Another challenge is that with the integration of digital wallets and mobile banking applications, customers now can withdraw funds in seconds, allowing customers to access their accounts and initiate transactions directly from their smartphones.

Platforms relegate banks to back-end players

As a result, a shift in retail payments has occurred, including merchant payments, with an increasing number of transactions originating outside the bank’s realm today. Platforms, along with their digital wallets and market places, are creating closed-loop payments systems that eliminate not only the payment processors and international card networks but increasingly relegate banks to back-end deposit institutions responsible for safeguarding larger amounts. Today, platform wallets are driving an increasing share of low-frequency transactions in both the retail and micro and small and medium-sized enterprises (MSME) segments of the business.

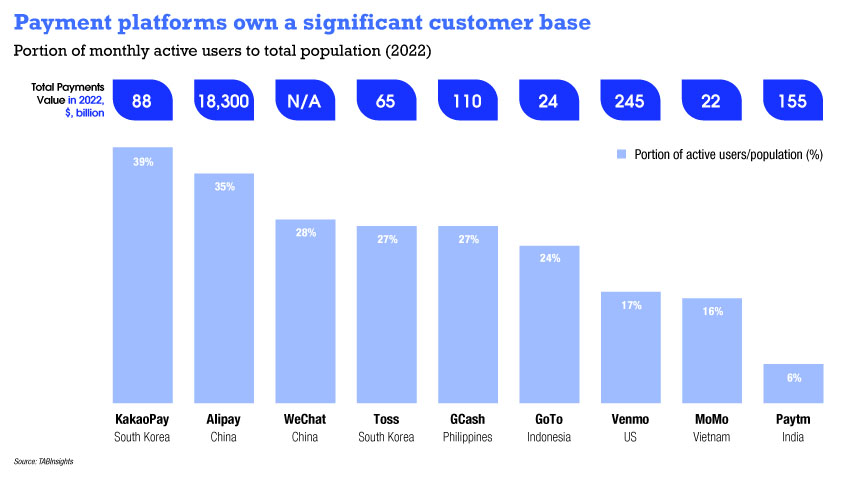

By the end of 2020, the number of users of digital wallets in Asia Pacific (APAC) stood at 1.8 billion, according to global payments platform Boku. By 2025, the number of digital wallet users is anticipated to surpass 2.6 billion.

The rise of digital wallets is gradually disrupting the traditional deposit business, offering unprecedented convenience in accessing and managing funds, as well as being part of a whole digital ecosystem. As a result, they provide users with enhanced value compared to traditional deposit accounts.

This is evident in Indonesia, where the the GoTo financial ecosystem saw remarkable adoption of its digital wallet GoPay. According to a TABInsights survey, around 85% of GoPay customers use the wallet for e-commerce purchases on platforms like Tokopedia. Additionally, 71% of users utilise GoPay for online transportation services like Gojek.

In Indonesia, India and China, e-wallets contribute 39%, 5% and 58%, respectively, to total number of payments transactions in 2022, according to central bank data. The APAC region led the global surge in digital and mobile wallet adoption, with the highest share of total e-commerce transactions of about 69% in 2022, according to Worldpay. Digital wallets are the leading e-commerce payment method in China, India, Indonesia, the Philippines and Vietnam.

Kakao Pay aims at 10 billion transactions per year by 2026

Today, the fastest growing platforms in Asia in 2022 were Indonesia’s GoTo, Philippines’ GCash, India’s Paytm and MoMo in Vietnam. They grew user bases between 21% to 38% year-on-year (YoY) in 2022. Kakao Pay, the mobile payment subsidiary of tech conglomerate Kakao in South Korea, aims to achieve 10 billion transactions per year by 2026, which would translate into every Korean over the age of 15 using Kakao Pay at least once every day to meet financial needs.

With market power, payments platforms and fintechs have gained significant influence, leading to a shift in how younger customers perceive banking. With the convenience they offer, many young customers no longer see the necessity for traditional banks. Digital wallets have successfully lobbied to increase deposit holding limits. Today, it is not uncommon for individuals to hold substantial amounts of money in wallets like Paytm and MoMo, with maximum total deposit limits of IDR 1 million ($12,000) and VND 50 million ($2,200), respectively.

Although wallets may currently be non-interest bearing accounts, there is a growing possibility that they could become the new everyday accounts, and backbenching traditional banks to become holders of longer-term deposits. This shift is driven by the emergence of open banking regimes, banking-as-a-service solutions, and the use of open application programming interfaces (API). These technologies present exciting new opportunities for any corporate entity with a large and loyal customer base to offer financial services, including deposits, in collaboration with financial partners beyond traditional banks.

Clarion call to banks to ringfence deposit business

Apple’s entry into the deposit business in April 2023, with its Apple Card savings account in partnership with Goldman Sachs, has served as a wake-up call for established incumbents. Digital banks are also capturing deposits successfully. Trust Bank in Singapore, a digital bank launched by Standard Chartered Bank (SCB) and FairPrice Group in September 2022, has attracted more than SGD 1 billion ($739 million) in deposits as of May 2023. About 95% of these deposits came from non-SCB customers, and 70% were from referrals.

The eight digital banks in Hong Kong have amassed total retail deposits of $2.7 billion between 2020 and 2022, with 83% of all deposits being captured by two banks, ZABank and Mox Bank. However, despite those numbers, their impact on the overall retail deposit market share remains marginal.

In Hong Kong, digital banks have hardly moved the needle in the last years, having a market share of 0.27% of total retail deposits. This can primarily be attributed to customers’ hesitation to transfer larger deposits into these digital banks. Customers have yet to develop the confidence to entrust these institutions with more significant funds, suggesting that digital banks still have considerable grounds to cover such as the lack of physical branches, and perceptions of long-term stability, before they can secure primary banking relationships.

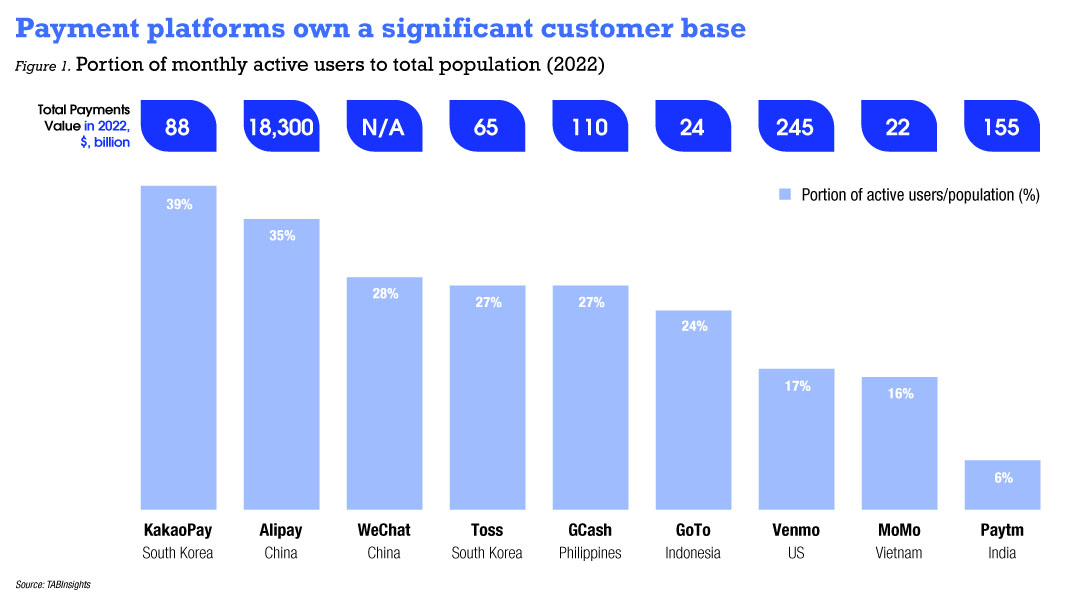

On the lending side, platforms and big tech’s immense data sets allow them to build sophisticated financial models for enhancing customer engagement, sales strategies, and gaining substantial ground in the credit sector. The latest forecast from Bank for International Settlements data predicts that globally, alternative financing by big tech and fintech grew from $796 billion in 2019 to over $925 billion by 2022, with the APAC region contributing 85% or the equivalent of $786 billion.

MSME financing has become the new battleground for banks and fintechs. The COVID-19 pandemic was not just a catalyst for adoption of financial services in the consumer space but also saw a rapid acceleration of MSME adopting digital services such as online payments, e-invoicing and e-collection services. The emergence of digital business models and their rapid adoption by MSME during the pandemic opened new avenues of growth and important value pools for non-traditional financial institutions.In China, the Greater Bay Area (GBA), comprising Guangdong Province, Hong Kong and Macau is home to over 6.6 million MSME. Together, they contributed over 55% of the region’s gross domestic product ($1.9 trillion in 2021). Yet, currently there is still about a 40% financing gap for small and medium-sized enterprises (SME) in the GBA, according to Hang Seng Bank.

Increasingly, fintechs and platforms are building capabilities to serve the SME sector by leveraging real-time cash flow monitoring for merchants and micro-entrepreneurs actively using their platforms. This innovation allows them to offer customised lending products at a larger scale, thanks to their advanced loan origination system designed for small-ticket microloans. Moreover, big data systems enable close to real-time earnings, empowering them to make informed lending decisions.For instance, Grab Financial Group provides working capital loans to its over two million merchant partners across Southeast Asia, customising its lending products at scale. Their approach involves deploying machine learning (ML) technology to determine the ideal loan quantum based on projected earnings. Technology and data science also enhance Grab’s collection strategy. It monitors which merchants are likely to repay their overdue amount, helping them to better allocate resources.

Banks spin off businesses from the edge for advantage

To address those market challenges from fintech and big tech more effectively, banks have begun spinning of certain retail banking businesses that sit on the edge of the bank’s core. They recognise that maintaining those within their legacy infrastructure no longer provides sufficient competitive advantage.

NAB Australia launched Hive in 2022, a cloud-based merchants payments portal for its merchant-acquiring capabilities, in which it will invest $100 million over the next two years to better address the needs of the MSME market in Australia. Hive will take NAB one step further into the battleground of merchant-acquiring business where fintechs such as Block, formerly Square, and Tyro have made inroads to provide seamless and frictionless ways to enable merchants to accept payments from their customers.

Banks began institutionalising their digital transformation processes as early as 2016, for example, StandChart’s Global eXellerator programme in 2016 and UnionBank’s UBX in 2018. These programmes emulated fintech-like objectives aimed at accelerating digital growth and transformation anchored on customer journey reimagination, advanced analytics and ecosystem partnerships, and piloting agile ways of working to allow for new ways of delivering digital solutions at speed. It was also the start of building fintech alliances.

Going beyond front-end process automation

Today, banks are increasingly shifting priorities, going beyond front-end process automation and digitalisation to modernise key IT and technology infrastructure. Besides focusing on cloud migration, they are building API infrastructure and microservice architecture, and automating key processes such as digital end-to-end lending and electronic know-your-customer (e-KYC).

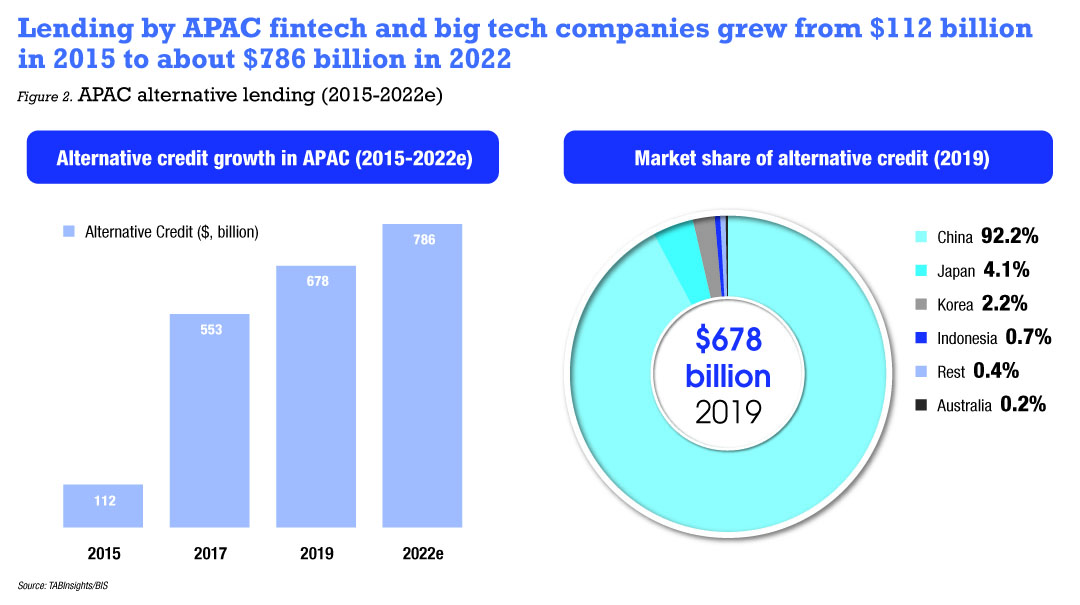

This shift is to match a bank’s internal capabilities with the speed and agility, as expected by customers. Modernising the technology stack has become a primary focus for leading banks, with a clear emphasis on adopting a cloud-first approach. This strategy involves the migration of existing and new applications from on-premises infrastructure to the cloud, covering a wide spectrum of systems, tools, products, and applications, including terminal and core systems.This shift is also visible in how banks reprioritise investments into productivity, growth and digital transformation versus compliance, risk and branch infrastructure. Based on insights from The Asian Banker’s Excellence programme, banks reprioritise investments into productivity, growth and digital transformation in the range of $200 to $500 million over a five-year period, but overall technology spend has rapidly risen since the outbreak of the pandemic by about 20% to 30% between 2020 and 2022.

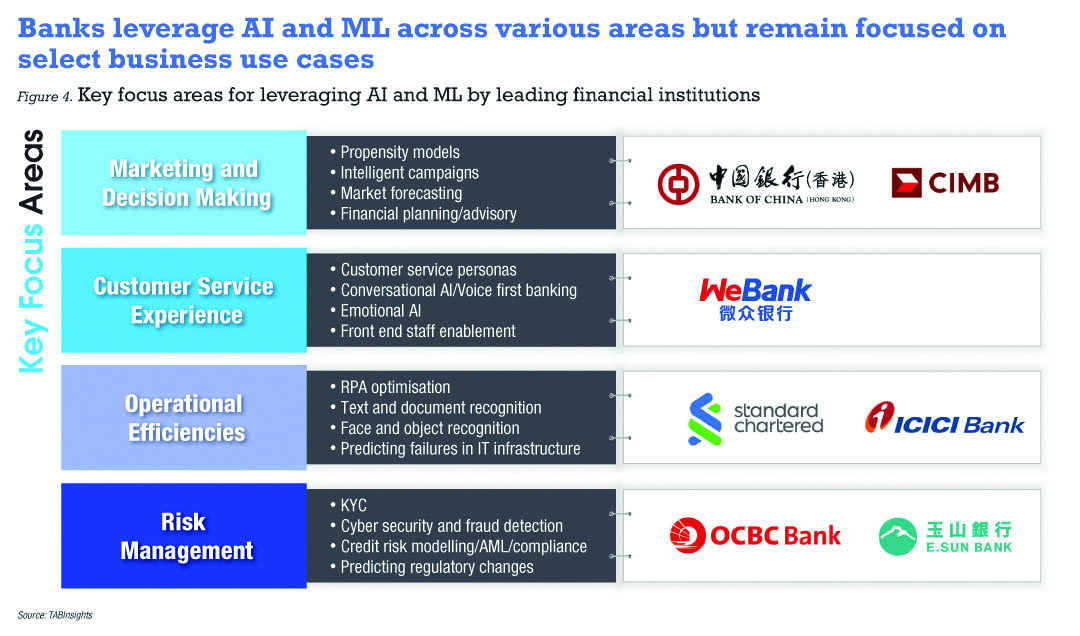

The increasing need for personalised, relevant, immediate, and interactive customer communication at scale, all within a secure and trusted environment, is catalysing the adoption of artificial intelligence (AI) and ML applications. These technologies have significant implications for financial institutions in four key areas: marketing and decision making, operational, efficiencies, customer experience, and fraud and credit underwriting. On average, banks have built between 50 to 100 AI/ML models, while leading banks have deployed more than 200 models in retail banking.

AI and ML use cases

AI and ML models are now being utilised not only for fraud detection and prevention, but also in a broader range of use cases that directly impact the customer experience. They also support better customer insight, improved propensity modeling for growth and better credit decisions. These models also empower banks to achieve cost and time efficiencies.

However, banks face challenges when it comes to scaling advanced AI and real-time capabilities beyond selected use cases, hindering their ability to generate substantial business benefits throughout the organisation. Meanwhile, the data architecture in many banks is not truly real-time. The ability to monetise data will be the key differentiator, but data integration, resilience and governance remain a challenge for the entire industry.

In customer service, generative AI has redefined the benchmarks, bringing conversational capabilities to customers, and highlighting substantial opportunities for financial institutions to elevate their services. Predominantly, chatbot applications in finance leverage rules and intents for task automation and call-centre expense reduction. While marketed as a customer experience booster, it primarily serves as a cost-saving mechanism for most banks.

Traditional banking chatbots frequently encounter difficulties with intent recognition and context retention. For straightforward inquiries, intent recognition rates vary from 60% to 80%, but these rates drop below 50% for complex queries, notably for ‘non-English-speaking’ bots. Moreover, most chatbots struggle to retain and apply context from earlier conversation exchanges. So far, only 14% of banks in APAC have adopted the GPT-3 model for their conversational AI interfaces, with a significant portion from China.

In conclusion, banks have begun focusing on modernising their technology and IT infrastructure to match the speed and agility customers expect at the front end when interacting with them.

Regulators still lean towards banks for being the primary institution in safeguarding customers deposit, but a rising segment of customers now view digital wallets as their primary tool for everyday transactions. Platforms and super-apps—not traditional banks—are dominating customer engagement and increasingly own the customer. This puts banks in a back-office role, providing traditional services of risk management, wealth and advisory and long-term safekeeping of larger customer funds.

.png)

.webp)