- Nigeria’s mobile wallet penetration in 2020 reached 9.2% and is expected to reach 18.9% in 2025

- Softbank’s investment in OPay will be used to enter more markets across Africa

- OPay has the potential to evolve into a full-scale digital bank

OPay, a fintech founded in Nigeria, launched its mobile payments platform in Lagos in 2018. The company has since expanded its offerings to allow users to pay for utility bills, make real-time money transfers to banks and other users for free, chat on the app, perform offline banking transactions, and open a savings account with any of OPay’s saving products with up to 15% interest returns per year.

Mobile wallet penetration to reach 19% by 2025

Telco-led mobile wallets have had a leading presence in Nigeria for many years. However, its flourishing fintech sector has led to rapid growth of its mobile payments market. Mobile payments company Boku reported that mobile wallet penetration in Nigeria is expected to increase from 9.2% in 2020 to 18.9% in 2025. Mobile wallet transaction volume is expected to increase from 4 billion in 2020 to 7.5 billion in 2025. Moreover, mobile wallet transaction value is expected to increase from $45 billion in 2020 to $72.5 billion in 2025.

As of 2020, OPay is valued at $2 billion and revenues reached $38 million. The company raised $570 million in funding and has built a network of 300,000 offline agents to serve as physical bridges to its financial services. It serves around 10 million Nigerians and processes around 20% of total point-of-sale (POS) payments. OPay’s monthly transactions grew 4.5 times to over $2 billion in December 2020. OPay claims to process about 80% of bank transfers among mobile money operators in Nigeria and 20% of the country’s non-merchant POS transactions. As of 2021, the company’s monthly transaction volume has exceeded $3 billion. Moreover, in terms of processed transactions by OPay’s mobile wallet, it is expected to have a compound annual growth rate of 10% over the next five years.

OPay has developed an easy-to-use mobile wallet that will bring increased financial inclusion to Africans. User can open an OPay account with a valid phone number and active email address. If the user does not have a bank account, they can still use and fund their OPay wallet by visiting an OPay agent and providing them with the OPay number so that the deposited amount can be transferred to the wallet. The accessibility OPay provides is an advantage compared with a traditional bank account where a customer needs to apply, wait for a bank teller, be approved to get an ATM card, and then register for online banking.

Furthermore, OPay customers get three free bank transfers daily. Succeeding transfers cost NGN 15 ($0.036). A 3% service fee is charged when a transaction is initiated and is automatically deducted from the account balance. OPay’s attractive offering is providing Africa the push towards increased financial inclusion through digital innovation.

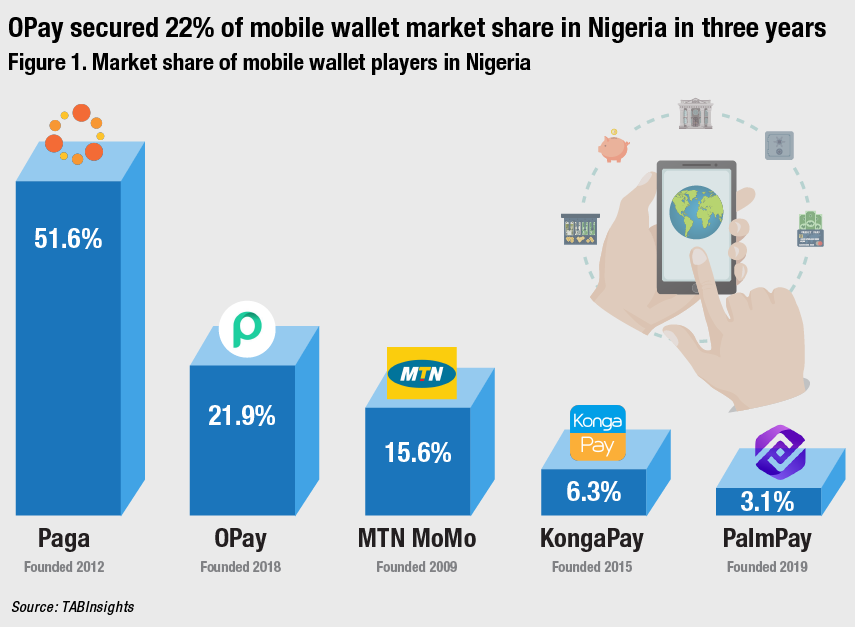

OPay has 15 million active users in the markets where it operates, including Nigeria, Kenya and Tanzania. The company processes 100,000 transactions per day on average. In Nigeria alone, its users have saved over $3 billion in the last four years through credit-linked savings accounts from their mobile wallets and via small loans from lenders that use its platform to lend to its customers. OPay’s market share in the Nigerian market is at 21.9%, surpassing MTN Momo, KongaPay and PalmPay.

OPay has managed to carve out a significant share of the mobile money market in Nigeria since its operations started in 2018. Mobile payments platform Paga, which launched in 2012, holds a majority market share of 51.6% of the Nigerian market and has over 17 million users. It has processed $8 billion worth of transactions in the last four years. However, OPay has minimal transaction requirements. On OPay, the basic transaction limit is NGN 50,000 ($121.63) before the customer will be required to supply additional information, which is the same for Paga’s Level 1 customers. Paga’s Level 2 customers that have their names, phones, addresses and ID card information on file can transfer up to NGN 200,000 ($551) per day.

Like Paga, OPay also uses both online and offline agents to deliver payments solutions to as many people as possible. Although Paga processes more transactions, OPay has more offline penetration at 40,000 agents, compared with Paga’s 15,000 transacting offline agents.

OPay offers bank-mobile payment duality whereby the customer’s account number is also their phone number. Paga also allows users to receive money from any bank in Nigeria. Users are, however, assigned a separate account number. Moreover, in July 2021, OPay launched the OPay debit card, allowing customers to earn cashbacks, withdraw cash, and make fast and straightforward funds through online and offline channels.

Softbank penetrates African payments space with OPay investment

Softbank’s investment in OPay for a 30% stake at its post-money valuation of $2 billion is the largest so far in Africa. SoftBank founder, Masayoshi Son, said that the investment in OPay would give them a competitive advantage over other companies in the payments business that might try to enter Africa in the coming years. “The company is confident of its potential to bring financial inclusion and improve the lives of people on the continent through the use of mobile phones and other technology,” explained Son.

He also said that SoftBank will be able to learn a lot from OPay on how to manage financial services across the continent. With Son's plans to expand SoftBank into the African continent, this investment could lead to opportunities in the future.

OPay’s rapid growth in Nigeria provides a very strong foundation in the years to come to further expand its business. Each of the mobile money startups in Nigeria have employed slightly different products and go-to-market strategies as they have scaled.

As OPay looks to the future, it has possible strategies to pursue for growth including geographic expansion and financial inclusion. Earlier this year OPay launched in Egypt, Africa’s second largest economy. OPay faces major competition in Egypt from Fawry, an Egyptian mobile money and payments company that recently went public and has a market capitalisation of around $1.8 billion.

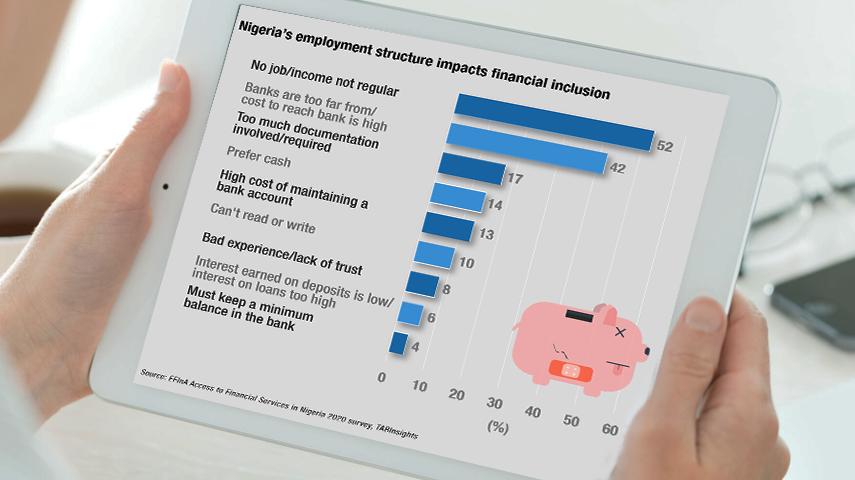

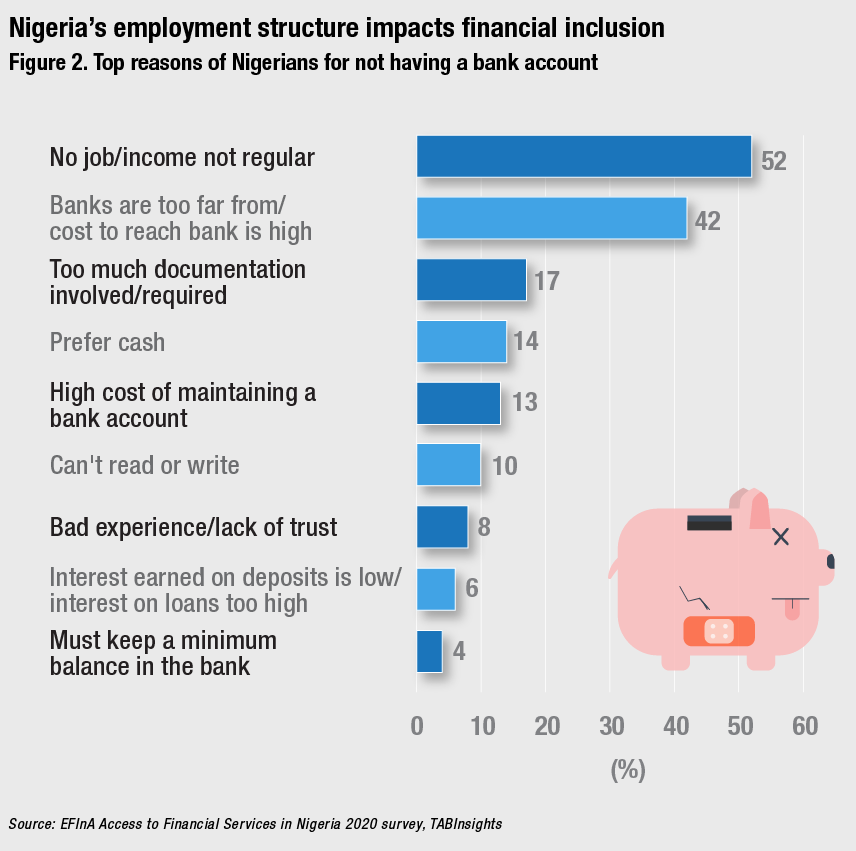

Only 45% (47.7 million) of Nigeria’s population are banked. The most prominent reasons for not having a bank account include people’s attitude or perception towards banks, poor accessibility to banking services, and irregular or low income. Nigerians who are willing to open a bank account need to submit a valid identification such as a national ID or passport, proof of address from utility bills and NGN 5,000 ($12) deposited in the account. However, around 66% of the adult population live in rural areas, unemployment reached 27.1% in the second quarter of 2020, and around 40% of the population live in poverty.

Growth in digital financial services, agent networks and mobile phone ownership (now at 81%) highlights the opportunity to drive faster financial inclusion growth through digital financial services such as mobile money and which showcases the huge potential of mobile wallets in the country.

Evolving into a full-scale digital bank

OPay has the potential to expand into a full-fledged digital bank due to its large user base. Kuda Bank, a digital banking startup in Nigeria, raised $55 million in funding at a $500 million value. Kuda claims to have 1.4 million users, compared with OPay's estimates of 2 million mobile money wallets with balances and 10 million Nigerians served directly or indirectly.

However, Nigeria's financial regulators have recently initiated an aggressive crackdown on fintech companies in the country, enacting a slew of new rules and laws. The Central Bank of Nigeria is yet to create a specific licensing regime for digital banks. This may pose a challenge to any hopes OPay may have to become a digital bank in Nigeria.

OPay is well positioned for significant expansion in Nigeria and new markets in Africa in the coming years given the rapid growth of its payment volume in Nigeria and its $400 million funding. As financial inclusion continues to increase in Africa, mobile money products such as OPay are key to integrating the unbanked into the financial system. OPay can build on its momentum in Nigeria to continue to expand its mobile payments offerings and eventually the potential to include a full-scale digital banking platform.

.png)

.webp)