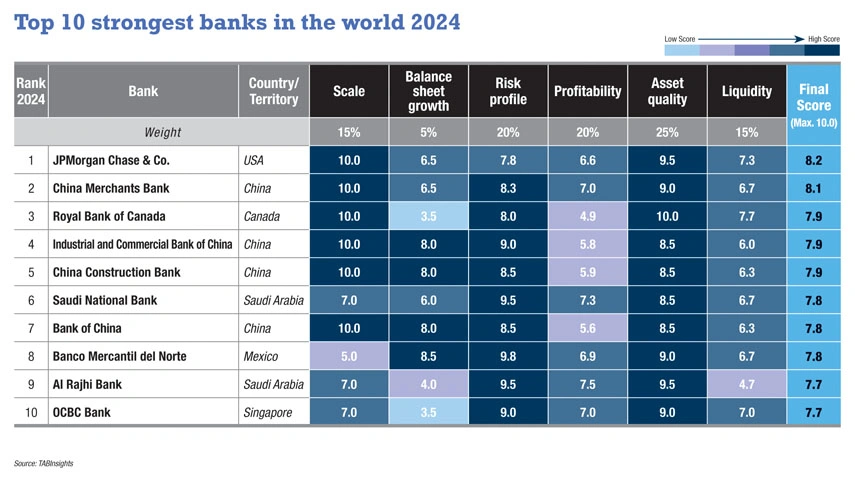

JPMorgan Chase, China Merchants Bank, and Royal Bank of Canada hold the top three positions in the TAB Global 1000 World’s Strongest Banks ranking for 2024. The ranking encompasses 1000 banks from 99 countries, territories, and special administrative regions, evaluating their performance in the financial year (FY) 2023, with a cutoff date set at the end of March 2024.

The TAB Global 1000 World’s Strongest Banks ranking evaluates the 1000 largest banks in the world based on their balance sheet strength. This ranking employs a detailed and transparent scorecard to assess banks and financial holding companies base on six criteria related to balance sheet performance: scale, balance sheet growth, risk profile, profitability, asset quality, and liquidity, encompassing 14 specific factors.

.jpg)

The ranking covers 440 banks from Asia Pacific, 217 from Europe, 179 from North America, 70 from the Middle East, 46 from South America, 29 from Africa, 12 from Central America, and seven from the Caribbean. Among the top 100 strongest banks globally, 40 are from Asia Pacific, 28 from Europe, 16 from the Middle East, 14 from North America, and two from South America. Notably, the strongest banks in Canada, China, Finland, Hong Kong, Indonesia, Mexico, Saudi Arabia, Singapore, Sweden, the United Arab Emirates (UAE), and the United State (US) occupy positions in the top 20 globally.

Top 10 strongest banks in the world

The top 10 strongest banks in the world include four Chinese banks, two from Saudi Arabia, and one each from Canada, Mexico, Singapore, and the US. These banks have achieved excellence across most dimensions, especially scale, risk profile, and asset quality.

.jpg)

JPMorgan Chase claims the top spot globally with a score of 8.2, rising from 31st place in last year’s ranking. The bank had a strong year, marked by notable advancements across most dimensions. Its loan growth accelerated from 5% in FY2022 to 17% in FY2023, driven by the acquisition of First Republic, an increase in new accounts, and higher revolving balances. Additionally, the bank saw enhanced profitability, with net profit increasing by 32%. Its return on assets (ROA) improved from 1% in FY2022 to 1.3% in FY2023, while the cost-to-income ratio (CIR) dropped from 59.6% to 53.7% Furthermore, its capital adequacy ratio (CAR) strengthened, rising from 16.4% in FY2022 to 17.7% in FY2023, with asset quality and liquidity remaining robust.

China Merchants Bank ranks second globally, achieving a score of 8.1, up from fifth place in the previous year. Compared to JPMorgan Chase, the bank scores higher in risk profile and profitability while trailing in asset quality and liquidity. Its profitability remained robust in 2023, with a ROA of 1.4%, a CIR of 34.9%, and a non-interest income to total operating income ratio of 36.7%. The bank achieved steady balance sheet growth through consistent business expansion while demonstrating prudent risk management, evidenced by a non-performing loan (NPL) ratio of 0.9% and a high provision coverage ratio. Its capitalisation position steadily improved over the past few years, reaching a CAR of 17.9% in 2023.

Royal Bank of Canada places third globally, showing improvements in risk profile and liquidity, although its balance sheet growth and profitability declined compared to the previous year. Its profitability was slightly reduced, with ROA dropping from 0.8% in FY2022 to 0.7% in FY2023, and the CIR edging up to 58.7%. Despite this, the bank led in non-interest income to total operating income among the top 10 strongest banks, at 51.3%. Additionally, it strengthened its CAR from 15.7% in FY2022 to 17.6% in FY2023 and maintained solid liquidity with a liquid assets-to-total deposits ratio of 55.4% and a liquidity coverage ratio (LCR) of 131%. In risk management, the bank continued to excel, holding the lowest NPL ratio among the top 10 banks at 0.4%, despite a slight increase from 0.3% in 2022.

Saudi National Bank rises from 22nd place last year to 6th this year, making it the strongest bank in the Middle East. The bank demonstrated impressive profitability, reporting a ROA of 2% and a CIR of 30%. Furthermore, it maintained a strong capital and liquidity position, with a CAR of 20.1% and an LCR of 258%. Its asset quality also improved, with the NPL ratio decreasing from 1.6% in FY2022 to 1.2% in FY2023. In comparison, Al Rajhi Bank excelled in profitability and asset quality, boasting an ROA of 2.1%, a CIR of 27.2%, and an NPL ratio of 0.7%. However, it fell short of Saudi National Bank in terms of balance sheet growth and liquidity.

Other banks within the top 10 strongest worldwide include Industrial and Commercial Bank of China, China Construction Bank, Bank of China, Banco Mercantil del Norte, and OCBC Bank. All three Chinese banks score well in scale, balance sheet growth, risk profile, and asset quality. OCBC Bank advances from 36th last year to 10th this year, reflecting better performance in profitability, capitalisation, and asset quality.

Overall strength

The global banking sector demonstrated enhanced performance in FY2023, as indicated by the increase in the weighted average strength score of the top 1000 banks, which has risen to 6.89 out of 10 from 6.78 in the previous year.

North American banks continue to lead in terms of overall strength, with a weighted average score of 7.05. This was followed by banks in Asia Pacific at 6.98, and the Middle East at 6.92. Middle Eastern banks show notable improvements this year, outperforming the global average. In contrast, banks in Europe, South America, and Africa are lagging behind, with average scores of 6.73, 6.22, and 5.56, respectively, remaining below the global average.

The 1000 banks in the ranking reported a weighted average ROA of 0.81% in FY2023, up from 0.75% in FY2022, benefiting from higher interest rates. Banks in Africa, Europe, and the Middle East experienced improvements in ROA, while those in North America, South America, and the Asia Pacific saw declines. Africa led with the highest average ROA, followed by the Middle East and South America, while Asia Pacific recorded the lowest at 0.73%.

The ROA for banks in markets such as Hong Kong, India, Indonesia, the Philippines, Singapore, and Thailand improved, whereas China and Vietnam saw declines. The average ROA of Chinese banks fell from 0.82% in FY2022 to 0.75% in FY2023, primarily due to narrowed interest margins.

The average CIR for the 1000 banks was 49.7% in FY2023, slightly better than the 50.6% recorded in FY2022. All regions saw improvements in their CIR, except North America, where the average CIR gradually rose from 59.3% in 2019 to 61.9% in 2023. In North America, the CIR increased in the US and Canada, while Mexico experienced a decline. Banks in the Middle East had the lowest average CIR at 32.9%, followed by those in Asia Pacific, while North America and Europe lagged in cost efficiency.

Overall asset quality remained stable in FY2023, with the average NPL ratio steady at 1.6%. North American and Middle Eastern banks reported improvements, while South America and Africa experienced significant increases in their NPL ratios. The NPL ratios in Asia Pacific and Europe remained unchanged at 1.4% and 2.2%, respectively.

Most markets maintained stable levels of capitalisation and liquidity. However, banks in countries such as Bangladesh, Lebanon and Vietnam underperformed in capitalisation. European banks achieved the highest average score in liquidity, assessed through three indicators, liquid assets-to-total deposits and borrowings ratio, LCR, and net stable funding ratio (NSFR). The average liquid assets-to-total deposits and borrowings ratio for the 1000 banks was stable at 39%. Additionally, the average loan-to-deposit ratio remained relatively stable at 82%, while the average equity-to-assets ratio rose slightly from 7.4% in FY2022 to 7.5% in FY2023. More banks have disclosed LCR and NSFR, offering greater insights into liquidity risk profiles and improving transparency.

North America

Overall, North American banks achieve superior scores in terms of scale and asset quality compared to banks in other regions. Canadian banks continue to demonstrate the highest level of strength globally, although their lead has narrowed significantly. Canadian banks prioritise stability over risky ventures, relying on steady deposits for profits. They operate under stringent regulations, including stricter capitalisation and underwriting standards, which have resulted in reduced exposure to risk compared to their US counterparts.

The average score of Canadian banks has declined due to softer performance in balance sheet growth, profitability, and asset quality compared to the previous year, while banks in the US and Mexico saw improvements in their average scores. Three Canadian banks hold positions among the top 30 strongest banks in the world, down from six in the previous year.

Despite JPMorgan Chase being the strongest bank in the world, the average score for US banks overall ranks below that of their Canadian and Mexican counterparts. US banks record lower average scores in balance sheet growth, risk profile, profitability, and liquidity. Only five US banks are positioned within the top 100 strongest banks globally, with JPMorgan Chase and Bank of America among the top 10 strongest banks in North America.

.jpg)

Asia Pacific

Compared to North American banks, Asia Pacific banks excel in balance sheet growth, risk profile, and profitability but fall behind in scale, asset quality, and liquidity. This year, 39 Asia Pacific banks are ranked among the top 100 strongest banks globally, down from 48 last year.

China achieves the highest average score in the region, followed by Singapore, Hong Kong, and Indonesia, all scoring above 7. Meanwhile, markets such as Australia, Malaysia, Thailand, the Philippines, and Vietnam have average scores of 6.7, 6.6, 6.4, 6.1, and 5.1, respectively.

Chinese banks surpass those in Hong Kong, Singapore, and Indonesia in scale, balance sheet growth, and asset quality. In contrast, banks in Hong Kong, Singapore, and Indonesia excel in risk profile, profitability and liquidity. Four of the top five strongest banks in Asia Pacific are from China, with China Merchants Bank lea-ding the region. The strongest banks in Singapore, Indonesia, and Hong Kong—OCBC Bank, Bank Mandiri, and Bank of China (Hong Kong)—rank 10th, 16th, and 17th, respectively.

.jpg)

Middle East

Middle Eastern banks demonstrate notable improvements, achieving higher scores in all six areas, particularly in profitability, balance sheet growth, and risk profile. They outperform banks in other regions in terms of profitability, with an average score of 7.1 compared to the global average of 5. Additionally, these banks show strong performance in risk profile despite their relatively smaller size. Four banks from the region hold positions among the top 20 strongest banks in the world, up from two in the previous year.

Saudi Arabia attains the highest ave-rage score in the Middle East, reaching 7.5, followed by Israel, Egypt, and the UAE at 7.2, 7.0, and 6.9, respectively. Despite receiving relatively lower scores in scale at 5.5, Saudi Arabian banks excel in other dimensions, especially in risk profile and asset quality. UAE banks outperform Saudi Arabian banks in scale, balance sheet growth, profitability, and liquidity, but their average score in asset quality is the second lowest in the region. The average score for Qatari banks stands at 6.6, below the regional average of 6.9, largely due to underperformance in asset quality and liquidity.

The top 10 strongest banks in the region comprise four Saudi Arabian banks, two Kuwaiti banks, two UAE banks, and one each from Egypt and Israel. Al Rajhi Bank, Riyad Bank, and National Commercial Bank are the top three strongest in the region, all from Saudi Arabia. Mashreqbank, Kuwait Finance House, and Qatar National Bank, the strongest banks in the UAE, Kuwait, and Qatar, rank fourth, seventh, and 12th in the region, respectively.

.jpg)

Europe

European banks, on average, excel in risk profile and liquidity compared to banks in other regions. However, they lag in balance sheet growth, and their average scores in profitability and asset quality are also relatively low.

Countries such as Finland, Turkey, the UK, Italy, Sweden, and Switzerland receive scores above the regional average of 6.7, while France, Spain, Germany, and the Netherlands fall below this threshold. French banks demonstrate better performance in asset size and balance sheet growth compared to their UK counterparts but underperform in all other dimensions. Similarly, Spanish banks surpass UK banks in balance sheet growth and profitability but underachieve in other areas.

Sweden’s Skandinaviska Enskilda Banken and Finland’s Nordea Bank are the only European institutions to make it into the top 20 strongest banks globally. In total, 28 European banks rank among the top 100 strongest banks in the world, an increase of two from the previous year. The strongest banks from Italy, Germany, the UK, France, Spain, and the Netherlands rank 35th, 37th, 46th, 77th, 123rd, and 170th globally, respectively.

South America

South American banks excel in liquidity and profitability, scoring above the global average, but fall short in other areas. Brazil achieves the highest average score in the region at 6.7, followed by Argentina, Uruguay, and Peru.

While Brazilian banks experience a decline in their average profitability score compared to last year’s evaluation, they improve in other dimensions, such as risk profile and liquidity. The top 10 strongest banks in the region comprise four from Brazil, three from Argentina, and one each from Chile, Colombia, and Peru.

Africa

Banks from Africa achieve higher average scores in balance sheet growth compared to all other regions, but their average scores in scale and asset quality lag behind those of banks in other regions. Mauritius, South Africa, and Nigeria attain the highest average scores in Africa, with 6.8, 6.0, and 5.5, respectively. Mauritius has only one bank, Mauritius Commercial Bank, in this year’s rankings, placing 178th globally.

Overall, South African banks outperform Nigerian banks in scale, risk profile, and liquidity, while Nigerian banks score higher in balance sheet growth, profitability, and asset quality. The strongest banks in South Africa and Nigeria, FirstRand and Zenith Bank, rank 260th and 410th globally. In 2023, Mauritius Commercial Bank demonstrates superior capitalisation, asset quality, and profitability compared to FirstRand.

To view rankings, click here: https://tabinsights.com/ab1000/strongest-banks-in-the-world

.png)

.webp)