The development of novel digital currencies and the human values that their systems represent are beginning to fundamentally transform the intertwined canvas of international finance, globalised economies and fragmented social structures, giving rise to the spectre of the planet-wide borderless society that transacts with the future of money.

The emergence of various fiat currencies, central bank digital currencies (CBDC), and cryptocurrencies that each represent different sets of objectives or priorities established by the issuing body, authority, decentralised autonomous organisation or just Codebase, are altering the current money landscape, permanently. The growing pains of crypto and indeed the trainwrecks of major crypto initiatives have not deterred the rise of decentralised finance and the creator economy from pursuing a privacy-based system that operates outside of the purview of governments and centralised authorities. This in a nutshell is the ongoing narrative of the future of money. The really exciting aspect of this is the convergence of traditional finance (TradFi) and decentralised finance (DeFi), led by some of the most high-profile institutions in the field.

Larry Fink, CEO of asset management giant BlackRock, said last year that the tokenisation of securities is “the next generation for markets.”

Tokenisation of securities—next generation for markets.

Indeed, it’s a lot more than that, and they are not the only ones.

JPMorgan and Goldman Sachs are among the financial behemoths that have expanded into tokenisation. The Onyx Digital Assets network of JPMorgan enables the tokenisation of traditional assets including US Treasury and money-market products. In November 2022, the company used the Polygon blockchain to trade tokenised cash deposits. JPMorgan is also, according to Bloomberg and other credible sources, in advanced stages of the development of a new blockchain-based solution for cross-border transactions. They are reportedly currently waiting for the green light from US regulators and will then first launch this facility for corporate clients to speed up payments and settlements.

In January, Goldman Sachs’ Digital Asset Platform went live. It was created using Canton, a private, permissioned blockchain system. The first token issued by the tokenisation platform was a Euro 100-million ($107,338 million), two-year digital bond. In 2021, Franklin Templeton introduced a money market fund that used a public blockchain to record transactions, and last year, Hamilton Lane partnered with digital asset securities company Securitize to offer three of its funds as tokenised feeder funds.

Clearly then, the trend of blending, combining and extending traditional and decentralised finance is the grand canvas underpinning the massive movement of money around the world.

Role of the public sector

The Bank for International Settlements (BIS) plays a crucial role within the existing international financial system by offering liquidity to global markets via its reserve currency and banking services. The proliferation of cryptocurrencies and other blockchain-based technologies is persistently causing disruptions in conventional banking systems, prompting the BIS to adopt a proactive approach in addressing this growing trend.

The partnership of BIS with Ripple that focuses on cross-border payments, aims to enhance the velocity and effectiveness of international money transfers. The BIS is now also investigating the potential applications of these emerging technologies in various domains, including but not limited to, smart contracts, secure data storage, and distributed ledgers.

Central banks are currently adjusting to remain a significant participant in the financial convergence between TradFi and DeFI. They are considering the potential of CBDC as a viable solution for delivering secure, efficient, and cost-effective payment services to both consumers and companies. The aim is to reduce operational expenses by eliminating intermediaries and minimising reliance on middlemen.

In the simplest of terms, a CBDC is essentially a digital banknote which could be used by individuals as retail CBDC or rCBDC or between institutions as wholesale CBDC or wCBDC to settle financial trades.The significance of central banks in the advancement of CBDC is crucial, as they serve as risk managers entrusted with the responsibility of evaluating the possible hazards associated with these technologies. Central banks have the additional responsibility of ensuring that the implementation of any CBDC aligns with established regulatory frameworks. They are accountable for managing liquidity, safeguarding security, and upholding user-privacy related to CBDC. Further, central banks play a crucial role in preserving the banking sector’s ability to issue loans and credit, especially during times of crisis, and they need to ensure that CBDC implementations do not jeopardise that.

Alternative avenue for accessing banking services

Central banks are considering the use of CBDC as a means to modernise monetary policy frameworks. The objective is to harness the potential of digital currency in order to reduce transaction expenses, enhance operational effectiveness, and facilitate more direct consumer engagement. The implementation of CBDC could potentially assist central banks in achieving their goals pertaining to the promotion of financial inclusion. This could be accomplished by offering an alternate avenue for individuals who lack access to conventional banking services.

To move the needle on this front, the BIS Innovation Hub (BISIH) has, over the last three years, conducted 12 CBDC projects that cover retail and wholesale, both in a domestic and cross-border context. Distributed ledger technologies (DLT) were used in most of the experiments.

Central banks can address potential challenges posed by private sector innovations, particularly fintech companies, by ensuring that their solutions are designed with scalability and interoperability as fundamental principles. This means that a central bank’s CBDC must be able to readily connect to existing payment systems and networks, as well as scale up as necessary when new payment and settlement-related services are added. In addition, the CBDC should be designed for seamless integration with both existing and emerging technologies such as application programming interfaces (API) and DLT. This will enable central banks to maintain control over their payment systems while taking advantage of fintech solutions’ increased speed and efficiency. To this end, the BISIH developed the mBridge Ledger, one of the 12 projects mentioned, a cross-border wholesale CBDC platform based on a novel blockchain, to facilitate real-time, peer-to-peer, cross-border payments and foreign exchange transactions using CBDC. In addition, it ensures compliance with jurisdiction-specific policy and legal requirements, as well as governance requirements.

On the platform, a pilot involving actual corporate transactions centred on international trade was conducted with the participation of central banks, commercial banks, and their customers from four jurisdictions, demonstrating that it is feasible to seek a customised multi-CBDC platform solution to address the limitations of the current cross-border payment systems. The initiative will continue to develop and test the technology, while adding more liquidity, compliance, and connectivity features, with the goal of bringing the platform closer to a production-ready state. In the subsequent phases of the initiative, additional use cases, participants, and legal and governance framework development are anticipated.

Additionally, it is essential to consider the impact that CBDC may have on central banks. For example, they could facilitate faster payments and new types of transactions such as direct investments in financial instruments. This could provide central banks with new opportunities to conduct monetary policy in a more efficient manner. Indeed, some experts have argued that the implementation of a CBDC could assist central banks in gaining greater control over the money supply and interest rates.

Where CBDC projects are today

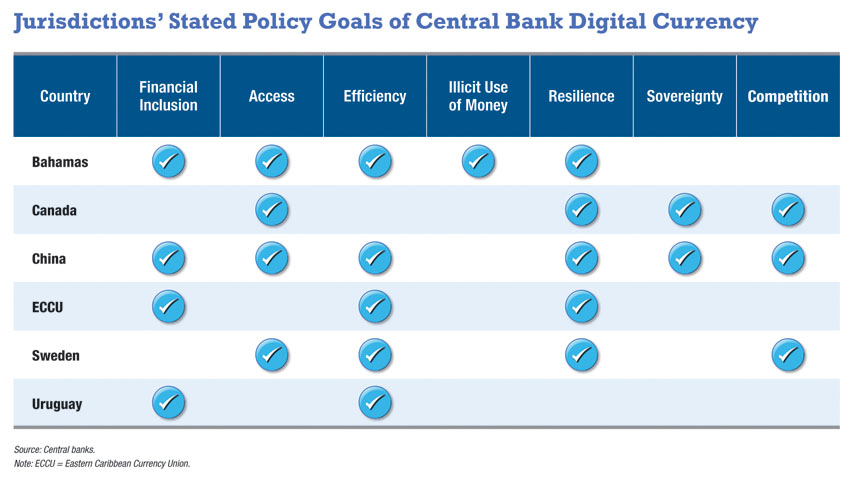

The International Monetary Fund (IMF) has studied different countries’ CBDC policies and designs. The outcomes were summarised in a report that essentially concluded that CBDC have different design and architectural considerations based on each country’s goals, needs and financial and monetary environment. IMF managing director Kristalina Georgieva stressed that the report’s key lesson is that there’s no one-size-fits-all. Here’s a round-up of the prominent examples of CBDC projects today, from around the world.

Americas

Bank of Canada: The bank has not found a pressing case for a digital currency given the present state of the Canadian payments system. However, it continues to build the technical capacity to issue a CBDC, and monitor developments that could increase its urgency.

Central Bank of the Bahamas, Sand Dollar: The Sand Dollar was officially launched in October 2020. In late 2021, there were around 20,000 active Sand Dollar wallets in a population of about 400,000, and functions are continuously being developed.

Eastern Caribbean Central Bank, DCash: No decision has been made to formally issue DCash. In March 2021, the bank launched a pilot program to successively extend DCash throughout the countries of the Eastern Caribbean Currency Union and run the program for 12 months. Given its rapid adoption, the bank is now considering transitioning to an official CBDC launch.

Banco Central de Uruguay, e-peso: After ending a pilot in 2018, the bank has changed leadership and has opted not to pursue a second pilot due to other priorities and a lack of resources. Potentially, a second pilot will be launched in the future.

Asia

People’s Bank of China, e-CNY: No formal decision has been taken to launch the e-CNY. The bank runs a pilot in parallel in different regions. By October 2021, there were over 123 million e-CNY wallets registered with individuals and about 9.2 million wallets held by firms—a rapid increase from approximately six million active e-CNY wallets in April 2021. In a population of nearly one and a half billion, the share of e-CNY users is now approaching 10%.

Europe

Sveriges Riksbank, e-krona: No decision has been made to issue the e-krona. The Riksbank has developed a proof of concept and is exploring technological and policy angles of CBDC. A government inquiry is investigating the role of the state in the digital payments system, including the potential role of CBDC.

European Union: On 28 June 2023, the European Commission published a draft regulation to establish a framework facilitating the possible introduction of a digital euro and a legislative proposal to strengthen the legal tender status of Euro cash, both of which were welcomed by the European Central Bank (ECB). Its governing council will decide in the autumn whether to move to the next phase of the digital-Euro project.

The potential implications for financial stability, international payment systems and monetary policy have caused experts to ask questions about what form CBDC should take, how it could be implemented, and the legal and regulatory frameworks that need to be in place. These questions are being discussed at both the national level by governments and central banks, as well as at the international level through organisations such as the BIS and ECB.

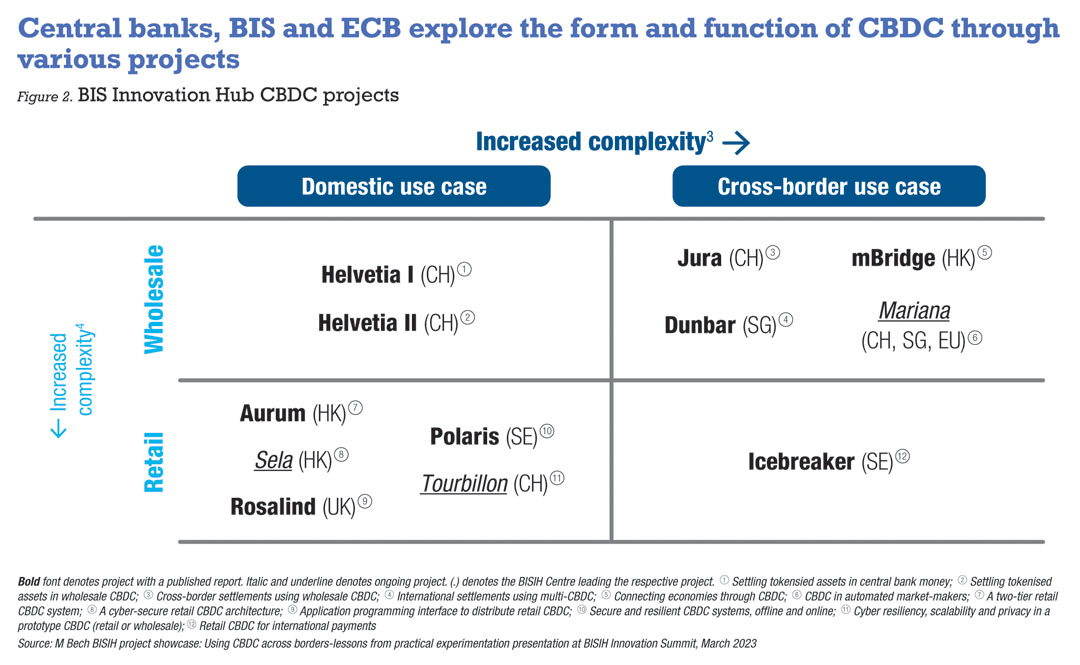

CBDC have other use too such as automated market-making. The BISIH released a report earlier this year on CBDC activity they undertook. The chart below from this report summarises the landscape.

Aurum and Helvetia were the first two projects that were undertaken. Helvetia tested how tokenised assets can be settled in central bank money by leveraging a fully-regulated digital platform based on DLT that was demonstrated in Switzerland as the SIX Digital Exchange. This was done while Aurum prototyped a retail CBDC wallet that emulates the current two-tiered framework for bank note issuance in the Hong Kong Special Administrative Region.

A second wave of initiatives investigated how to achieve faster, cheaper, and more transparent cross-border payments, including securities settlement, by making use of wCBDC. These investigations were in response to the G20 cross-border payments programme. Common systems that include numerous wCBDC have been shown to be operationally practical and capable of bringing about efficiencies by the Jura, Dunbar, and mBridge projects.

The Hub’s efforts focused on specific design challenges and included how to use API to distribute and settle retail CBDC (Rosalind), ensure cyber-secure open and accessible retail CBDC architecture (Sela), implement and operate CBDC platforms that are secure and resilient, offline and online (Polaris) and how to develop a CBDC system that preserves transaction privacy, is resilient to quantum computer attacks and can handle large transaction volumes (Tourbillon).

Private sector innovations adapting to the digital era

CBDC have the potential to revolutionise payments, particularly in countries with limited bank service access. Stablecoins, meanwhile, are digital assets guaranteed by fiat currency that can be used to eliminate the requirement for fiat currency when making payments. Integrating CBDC and stablecoins could result in a more efficient system for international remittances. By leveraging the benefits of both asset classes, it would be possible to process payments with greater speed and security.

Additionally, the integration of these two categories of digital assets could reduce costs for both businesses and consumers, making international transactions more cost-effective. This joined-up system could benefit from enhanced transparency and traceability—the use of CBDC and stablecoins could reduce the risk of money laundering and other financial crimes, in addition to making it simpler to monitor payments. This new financial system would be more dependable and secure as transactions could be monitored in real time.

Finally, integrating CBDC and stablecoins could also enable more efficient and cost-effective access to financial services for those in developing countries. By providing an alternative to traditional banking, these digital assets can open up new opportunities for people who have previously been excluded from the formal banking system.

The merging of CBDC and stablecoins could also offer the framework for a customer-centric digital banking system. By capitalising on the benefits offered by both asset classes, individuals would have the opportunity to access financial services in a prompt, secure, and cost-efficient manner, irrespective of their geographical location or socio-economic standing.

Furthermore, this approach has the potential to facilitate the development of new products customised to meet the unique requirements of particular clients. It has the potential to integrate many functionalities like smart contracts, decentralised applications, and tokenisation technologies.

Enabling seamless transactions

Cryptocurrency and blockchain-based systems have begun to reshape the payment infrastructure. Users can now send and receive payments across borders with minimal friction, significantly reducing the time required for international transfers. In addition, numerous businesses are using digital tokens to construct new payment infrastructure, such as fiat-pegged stablecoins. These tokens can be used to facilitate low-cost and dependable cross-border payments, eliminating the additional exchange rates and transaction fees associated with conventional payment methods.

By incorporating these innovative technologies into existing payment infrastructures, businesses are able to provide consumers with faster and more secure services. Ripple, for instance, is developing a blockchain-based platform that enables near-instantaneous remittances at lower transaction costs than conventional methods. This not only expedites transactions for consumers, but also enables merchants to enter new markets with more efficient payment methods. In addition, these technologies can be used in conjunction with existing payment networks, such as Visa and Mastercard, to enhance system interoperability and provide a more seamless transaction experience.

Further, the use of crypto-based payment solutions enables businesses to surmount a number of the obstacles associated with traditional banking and financial services. Due to the dearth of interoperability between payment systems, for instance, users are typically unable to transfer funds across international borders without incurring significant fees or waiting for lengthy periods of time for their transactions to clear. With crypto-based payment solutions, users can now send funds internationally swiftly, securely, and seamlessly, at a reduced cost and level of effort.

Fintech‘s rise: DeFi and tokenised assets

As the DeFi industry expands, more traditional assets are tokenised and made available on decentralised exchanges. This presents an exceptional opportunity to leverage the benefits of blockchain technology without jeopardising the safety or liquidity of investments.

Tokenisation has grown in popularity as a means for investors to diversify and manage their portfolios in ways that were previously impossible. Tokenisation has also made it simpler and cheaper for investors to enter and exit positions rapidly. Due to the tokenised assets‘ decentralised character, they can be traded directly between users without the need for expensive intermediaries. This has made the market more accessible to investors, as they can now gain access to a broader spectrum of assets with minimal effort and expense.

Tokenisation has produced new use cases for digital assets. For instance, tokenised securities such as stocks and bonds can be used in fractional ownership schemes, that enable users to invest small quantities over time. Tokenised real estate can be used to crowdfund property investments, giving investors access to the real estate market at a fraction of the cost.

DeFi has become increasingly prominent in recent years, providing a range of financial services and products based largely on public blockchains such as Ethereum. These services and products enable users to gain access to loans, derivatives, stable currencies and more without relying on conventional financial institutions. Unbanked and underbanked individuals now have access to financial services previously unavailable to them.

DeFi also provides users with numerous benefits, including reduced transaction costs, speedier settlements, and enhanced security. In addition, DeFi protocols are open-source and permissionless, ensuring that anyone, anywhere in the world, has unrestricted access to these financial services.

The combination of tokenisation and DeFi promises to create an open, transparent, secure, and universally accessible new financial system. DeFi and tokenisation can also provide numerous other opportunities, for instance, broaden access to alternative investments such as venture capital, private equity, and real estate, that are typically reserved for institutional investors.

It could also facilitate the development of new financial instruments, such as derivatives for crypto assets, which would increase market liquidity. In addition, by permitting users to construct their own tokens, it could serve as a platform for new forms of crowdfunding and peer-to-peer lending. All of these options could contribute to the development of a more efficient, transparent, and accessible financial system, which would be advantageous for both investors and entrepreneurs.

“DeFi is the future of finance,” said Vitalik Buterin, co-founder of Ethereum who I met at the Palau Blockchain Conference recently. Tokenisation is providing raw-fuel for that future.

Convergence of TradFI and DeFI taking shape

The convergence of TradFI and DeFi is beginning to take shape. This convergence is being driven by advancements in technology, as well as an increased demand for decentralised financial services. Both TradFi and DeFi have distinct benefits and prospective applications, but they also overlap in a number of areas and could be combined to create more efficient, cost-effective, and secure solutions. It has become apparent that the two models are not mutually exclusive; rather, they complement each other and can work together to create an efficient financial system.

TradFI has traditionally been the traditional go-to for institutional investors and other large financial entities. It is a more secure and reliable platform, but can be costly to access. DeFi, on the other hand, promises to bring increased transparency and accessibility to the world of finance by leveraging blockchain technology. By combining the two models, users can access the benefits of both.

For example, users can take advantage of decentralised exchanges to easily purchase and trade assets on a secure platform, while still being able to access the same services as traditional finance in terms of buying securities or derivatives. They can also use DeFi protocols to manage their risk exposure, such as through automated margin trading or synthetic asset generation. Additionally, users can benefit from the increased liquidity provided by DeFi protocols and the cost savings associated with using a blockchain-powered platform.

CBDC are an example of this convergence because they establish a link between traditional banking systems and blockchain-based solutions. CBDC enable financial institutions to issue digital tokens that clients can use to conduct transactions. This could reduce the cost of transfers, allow for faster payments than with physical currency, and provide greater security via decentralised networks. Additionally, CBDC could be used to facilitate more efficient and secure international payments. This would enable businesses of all sizes to access global markets, thereby reducing costs and fostering global economic growth.

Furthermore, CBDC have the potential to improve monetary instruments. CBDC could serve as an alternative to conventional methods of implementing monetary policy, such as quantitative easing and interest rate adjustments. This could allow central banks to manage their respective economies more efficiently by taking more targeted and timely action when necessary, and quickly.

Obstacles in scalability, governance and security

However, there are still numerous obstacles to overcome before these technologies can reach their full potential. These include issues with scalability, governance, and security. Despite these obstacles, however, it appears that the integration of TradFI and DeFi will result in a more efficient and secure digital financial system.

This could involve the harmonisation of financial systems across nations, allowing central banks to more effectively coordinate their actions and react swiftly in times of crisis. Creating a global network of payment systems that can facilitate cross-border transactions and permit the free movement of capital across borders could be the final step here.

.png)

.webp)