.jpg)

The impact of behavioral shift toward ‘anytime’ and ‘anywhere’, complemented by the increased usage of mobile devices; and a host of network infrastructure services are driving demand for faster payments from corporate and retail banking customers. Corporate customers at the same time are also demanding more granularity and transparency with respect to their payment credits and debits, in order to make informed cash and working capital decisions. For banks to keep up with the expectations of 24/7 instant payments, all participants must subscribe to a common industry standard which holds the promise to eventually attain a critical mass, or sufficient market reach. Underpinning this is the ISO 20022 XML standard, the emerging global standard for payments messaging, that promises to simplify corporate-to-bank communications for faster processing and improved reconciliation. With the launch of domestic real-time payment systems such as Single Euro Pay

ments Area Instant, New Payments Platform in Australia, and The Clearing House RealTime Payments in the US, the impetus for cross-border payments to achieve efficiencies is even greater. The latest Asian Banker survey of payment trends across Asia-Pacific highlights the use and availability of cost competitive electronic platforms/channels and wider uptake of common messaging systems as key emerging themes.

The fast consumerisation of corporate payments Consumer experiences are reshaping corporate expectations and their ability to transact in real-time, omni-channel environment, 24x7. To meet the corporates’ expectations of greater speed and efficiency through automation and digitalisation, regional banks have focused their attention to the roll-out of integrated payment solutions that leverage new and emerging technologies.

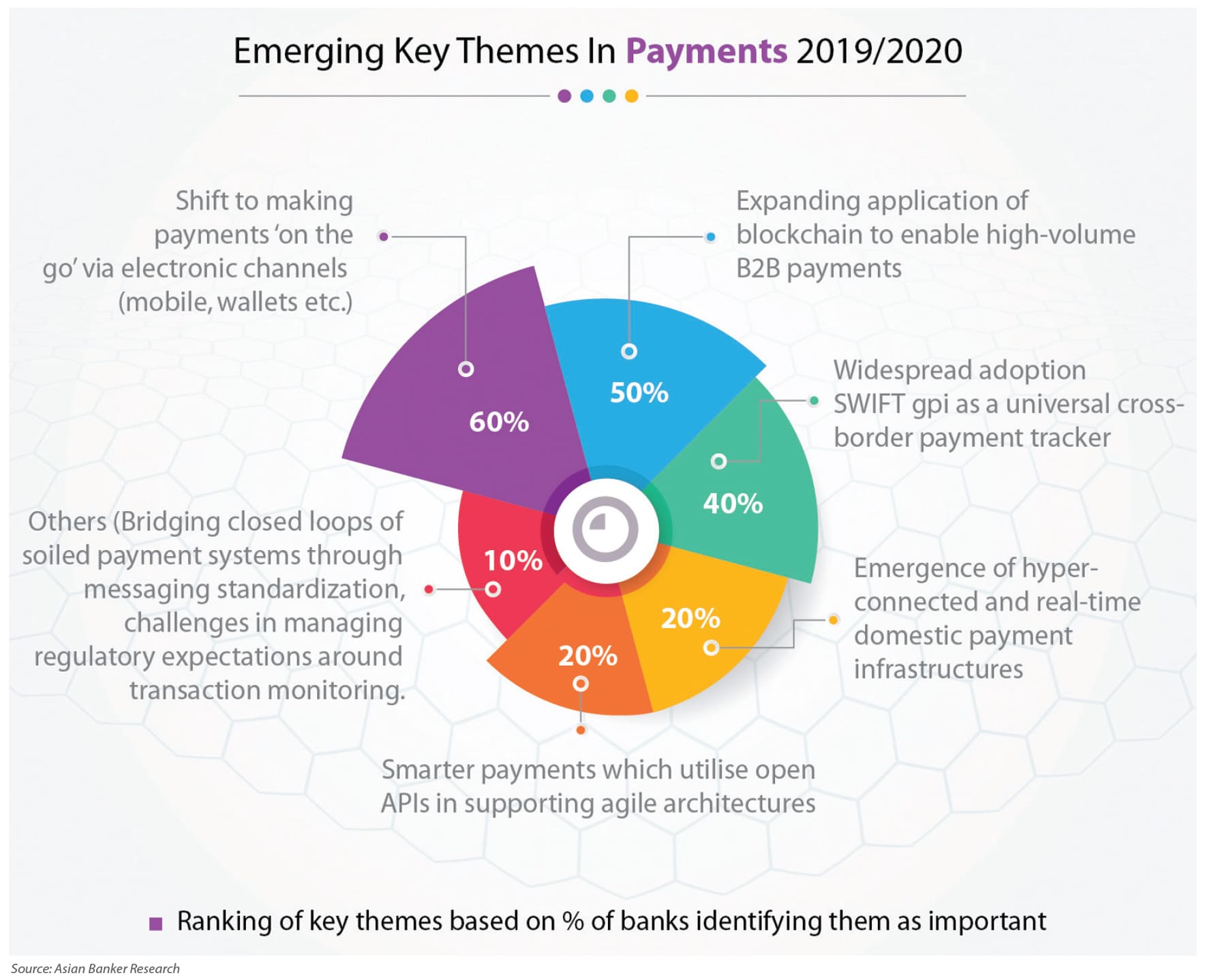

The focus on distributed ledger as an underlying technology and its potential to enhance efficiency, trust, transparency and reach in cross-border payments has gained prominence. Although commercialisation still remains far, the industry is seeing a consortium of international banks to collaborate or partner with networks such as Ripple’s real-time gross transfer system, based on its own digital asset, the XRP. That said, there is a case for expanding application of blockchain technology to enable high-volume business-tobusiness payments. Bank of China (BOC) continues to strengthen technological innovation and expand the application scenario of the bank’s blockchain payment system. It partnered with China UnionPay to build a unified port for mobile integrated financial services where BOC’s cardholders will be able to use a QR code to spend, transfer and trade on a cloud flash payment application. While Yes Bank’s solutions leverage wallets to application programming interface (API) networks and partnerships with agile fintechs and start-ups, it has advocated for blockchain technology as a means to save significant transaction costs. It partnered with Ripple to help make remittances in North America, the Middle East and UK, more seamlessly. Significant growth of merchants of direct banks and small-volume overseas remittance companies is driving competition in digital remittance market in South Korea. Woori Bank completed the second successful trial of cross-border remittance in partnership with Ripple, and aims to commercialise the transaction in the latter part of this year. There is also a continuous drive to convert costly and cumbersome cash and cheque payments to electronic payments, following the regulatory changes allowing banks to use digitised images, scans or photographs of cheques for processing, rather than the original paper document. Singapore-based banks launched relevant APIs that leverage PayNow Corporate, Singapore’s enhanced fund transfer service that links SGD Corporate Account to the institution’s Unique Entity Number. OCBC Bank, for instance eliminates issuance of paper cheques with API, to provide swift and easy disbursement of award monies to students. The interoperability between the bank and the partner corporate’s system through API triggers real-time payment instruction, eliminating reconciliation errors and bulk handling of cheques. Amidst intensifying competition within the ride-hailing and e-wallet space in Southeast Asia, UOB Singapore facilitated instant payments and efficient cash-outs for drivers and merchants. It enabled straightthrough processing via API connectivity and FAST clearing infrastructure, to enhance the pay-out experience for drivers and merchants. SWIFT’s gpi continues to gain traction as improved standard for cross-border payments The adoption of banks to SWIFT’s gpi service has been growing since its launch in early 2017. A major milestone was reached with the 270% year-on-year growth in gpi adoption with over $40 trillion transferred over the service by the end of 2018. On an average, SWIFT gpi is carrying over $300 billion a day in 148 currencies across 1,100 country corridors. Standard business rules captured in multilateral service level agreements between participating banks and a cloud solution that links every party in the payment chain have been driving the uptake. Our annual survey on payment trends highlights multiple connectivity challenges including lack of interoperability, infrastructure reachability and, existence of cross jurisdictional views arising from multiple parties on a single payment transaction. Around 30 banks out of 72 that have committed to gpi service, belong to the Asia Pacific region. Underpinned by strong and growing economic ties, banks are looking to deliver tangible improvements to their client’s crossborder needs. Importantly, 10 of the live gpi banks are Chinese while 17 others are in the process of going live, and would represent 86% of cross-border payment traffic in mainland China. A key player in the One Belt One Road project, Bank of China is committed to improve the overall banking experience by creating predictable settlement times, transparent bank fees and FX rates. It is leveraging the gpi tracker cloud platform to shorten the supply cycles and improve the shipping of goods on the customers’ end. To make its remittance services competitive, Woori Bank in South Korea highlighted the expansion of its international network and affiliate partnerships with member banks using the SWIFT gpi remittance service. With the gpi service, the bank aims to cut charge fees and lower the time required for digital channel remittances. However, the missing piece in the

jigsaw is really the availability of information throughout the processing of a payment transaction. A recent, significant development in this area has been the drive to migrate crossborder transactions to the ISO 20022 standards. Ready to be rolled out by 2021, the wider industry adoption will provide richer data and streamline communication for financial institutions for enhanced fraud detection and improved service integration. On one hand, regulations such as PSD2 is boosting competition and transparency while on the other, emergence of real-time payment systems is likely to add further

Corporate user-payment experience and payments infrastructure modernisation emerged as among the top themes in 2019 Figure 1. Emerging Key Themes in Payments 2019/2020 based on % of banks identifying them as important

challenge to regulatory compliance related to anti-money laundering and transaction monitoring. As one of the foremost supporters of SWIFT’s gpi service, Deutsche Bank outlined pressure on payments from stringent regulations. It incorporates gpi capability into its app stores, allowing customers to track the status of payment through the Autobahn app using Cash Inquiry. Moreover, taking a risk-based approach to know-yourcustomer (KYC) diligence, it has been instrumental in pushing the uptake of the SWIFT KYC registry, that promotes exchange of data between the registered market participants.

Source: Asian Banker Research

While these may appear to be game-changing initiatives, moving stakeholders closer to the reality of second-to-second tracking of payments and same-day use of funds, true goals would only be realised on achieving a critical mass. What corporates and their treasury centres really demand is a 360-degree view of all their payments in a multibank environment from their treasury management system. The recently launched enhanced gpi service for corporates is expected to relieve them of the need to adapt their systems for each individual bank they work with TAB.

.png)

.png)

.png)

.webp)