- China's credit card sector is becoming a profitable source to stimulate the bank's retail income

- China Merchant Bank has seen a shift in retail loans originated by credit cards

- China CITIC Bank has embraced big data to enhancing its marketing and branding capabilities

China experienced its slowest growth in 2015, raising genuine concerns about its impact on the local economy as well as on international financial markets. One concern was the debt-to-gross-domestic product ratio which reached 249% by the end of September 2015 compared to only 164% in 2008 according to BIS data. Meanwhile, the debt ratio in the Eurozone was 270% and 248% in the US, intensifying concerns about China’s debt ratio approaching danger levels. Strictly speaking, what matters is the risk of widespread corporate defaults in China provided defaults of other debts are relatively low. To confront a changing external environment, banks in China have adopted lower interest rate policies and therefore faced pressure on interest income. The near completion of interest rate liberalisation, a decline in shadow banking, and weak loan demand have all contributed to difficult market conditions for commercial banks in 2015. One solution to this problem is to strengthen retail banking models to relieve the dependence on interest income and open up non interest businesses.

As the expansion of household debt was a key factor in the sub -prime crisis for the United States, there is public concern in China as to whether household debt, an indispensable component of retail lending profits, will increase threats to the banking industry and Chinese economy. However, household debts constitute a lower portion of the GDP ratio because of high down payments in China even though the growth rate of household debt exceeds that of corporate lending. In recent years, household debt has not been overextended and the contribution of mortgages to the retail lending industry has been stable. Banks are exploring the potential in the retail banking sector especially in retail lending structures, and looking to identify what customers really need. For example, it can be observed that there is a shift to personal loans increasingly being originated by credit cards.

China’s credit card sector expecting improvements

An increasing number of Chinese are using credit cards for smaller ticket personal loans, however existing regulated interest rate policies for credit cards cannot meet the needs of the changing economic environment in China. First, fixed pricing of credit card interest rates by regulations is undifferentiated and inflexible failing to meet the more personalised and diversified needs of cardholders. Secondly, the single fixed interest rate approach restricts development of the credit card business, undermining the prospects for the credit card market. Thirdly, an increasing number of disputes between cardholders and credit card issuers have occurred, and a framework of cardholder protection needs to be introduced.

China’s commercial banks have not developed a clearly defined profit model for their credit card business and could learn from the experience of banks in other countries. Some banks use a method of “spread income”, encouraging customers into overdraft positions earning interest after the interest-free period. Other banks rely on profits from payments including instalment fees, penalty interest income, annual fees and cash withdrawal fees. The Chinese authorities are planning to take measures to intervene; a recently published notice indicates that credit card overdraft fees or interest rates will be lowered which will slightly decrease income in the short term. Meanwhile, banks can ease restrictions on parts of the business by facilitating customer classification and management. This should stimulate operating income in the long run.

China Merchants Bank

China Merchants Banks, in the face of rising competition, put forth a clear strategic objective for the next five years to place high priority on data processing and analysis capability in 2012. Using this data, in 2014, the Bank reinvigorated itself by strengthening its internal management, promoted process re-engineering, optimizing he organisational structure of corporate finance, as well as the organisational structure of retail finance at the head office and officially commenced the reform on operational systems of the branches. The bank keeps consolidating and expanding its retail banking business combining together the concept of customer, product, channel and brand. By building a holistic business management system, good customer structure, and multi-channel platforms, China Merchants Bank has established a leading position in the retail banking market.

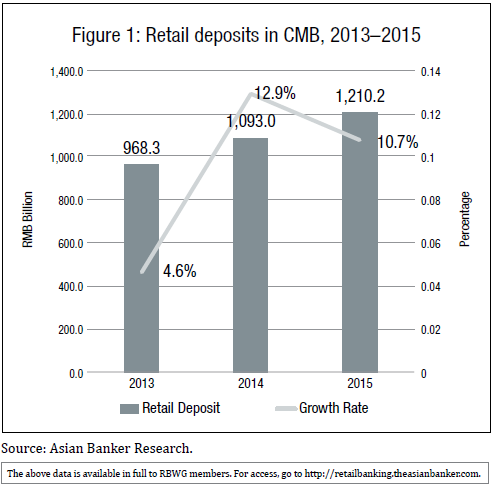

Retail deposits have seen a two-digit growth rate since 2013

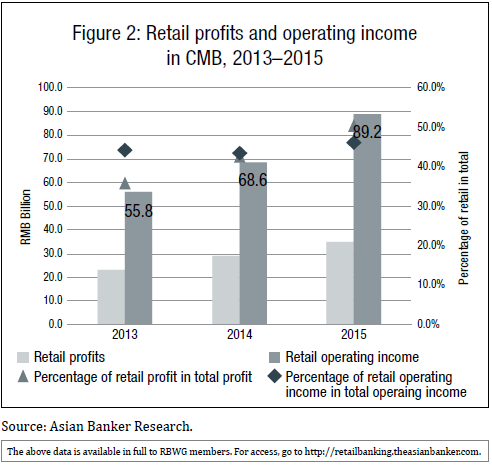

In 2015, the bank’s retail business earned pre-tax profits of RMB34.8 billion ($5.4 billion), amounting to 46.3% of total pre-tax profit. The business also posted RMB89.0 billion ($13.7 billion) in net operating income, which accounted for 46.4% or almost one half of the bank’s net operating income for 2015 (Figure 2). Retail operations again exhibited a strong performance in 2015, with pre-tax profits up 19.5% and net operating income by 29.9%, reflecting a solid, high-quality retail customer base from core businesses including wealth management, private banking and consumer finance.

Retail banking exhibited strong performance in 2015

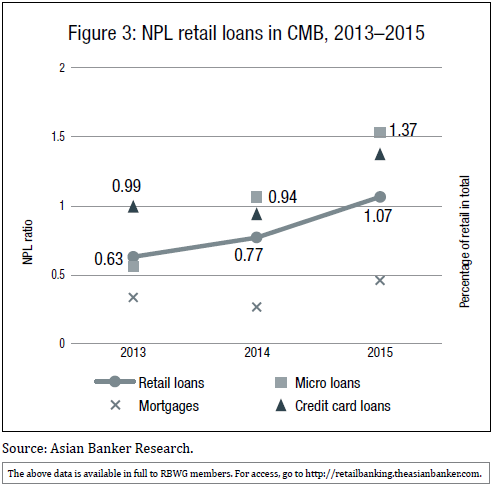

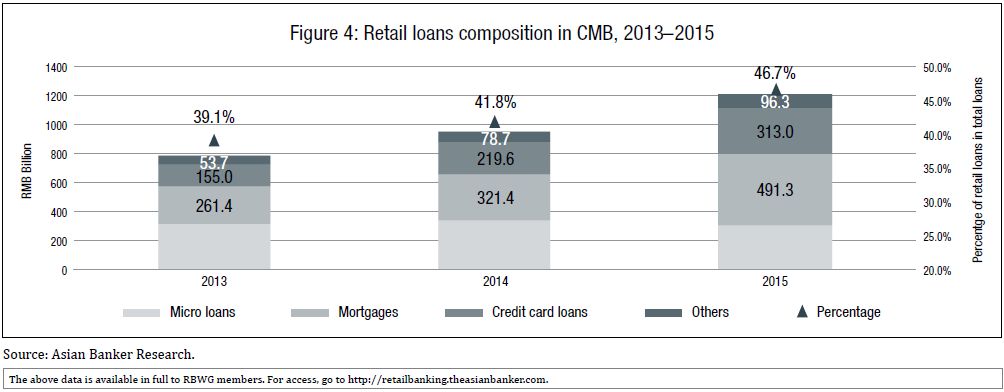

In terms of lending, retail loans have been steadily increasing since 2013. Retail loans increased from RMB785.5 billion ($ 128.8 billion) in 2013 to RMB955.3 billion ($147.4 billion) in 2014, and further to RMB1,209.5 billion ($ 186.7 billion) by the end of 2015. The retail loan balance amounted to almost half of total loans in 2015. Mortgages and credit card loans saw the most change as the retail loan structure of the bank was optimized. With regard to the composition of retail loans, the growth of micro loans steadily slowed while both mortgages and credit card loans increased. As a result of the economic downturn and weaker individual solvency, the retail NPL ratio was 1.07% in 2015, 0.30 percentage points over the previous year (Figure 3).

Retail NPL ratio was in a comparatively low position in the last three years

As at the end of 2015, the balance for mortgages was RMB491.3 billion ($ 75.8 billion), representing 40.6% of retail loans, and a 52.9% growth rate in 2014 (Figure 4). Meanwhile, the bank actively became the third bank in China to securitise mortgage loans to a scale of RMB7.2 billion ($ 1.1 billion), 1.5 % of its mortgage book. Since mortgages are usually held for long periods in China, stagnant mortgages at the bank could bring liquidity risk and lower the efficiency of fund use. Hence, mortgage asset securitization is an important tool to boost the bank’s credit loans thereby aiding development of the real economy.

The bank has seen a shift in retail loans increasingly being originated by credit cards

The bank has also continued to build its risk management system covering its front, middle and back office. The bank has adopted a centralised loan approval process covering more than 70% of its retail loans, enabling the bank to offer an automatic approval process for the housing loans business. After years of endeavour, China Merchants Bank has developed diversified risk management methods and continually optimised a standardised, data-based, and modelled risk management system. Innovations like the Cloud Mortgage PAD Platform and online peer-to-peer lending products led to the bank building “light” retail credit operating platforms, thus enhancing operational efficiency.

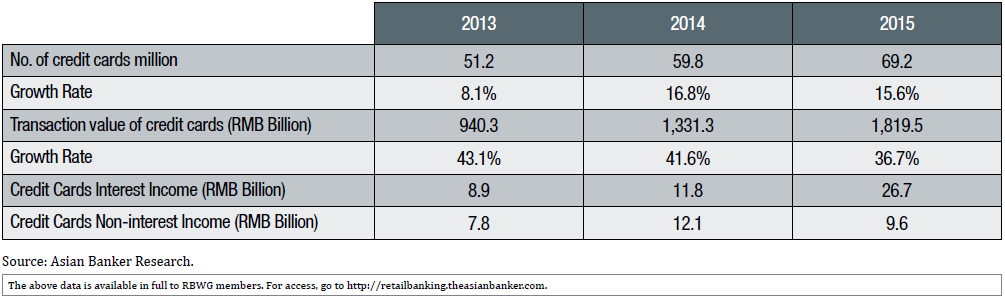

In 2015, the bank issued 69.17 million credit cards showing a moderate growth rate of 15.6% compared to 2014. The total transaction value of credit cards in 2015 was RMB1, 819.5 billion ($280.8 billion), an increase of 36.7% over 2014. By 2015, interest income from credit cards had increased from RMB 8.9 billion ($1.4 billion) in 2013 to RMB26.7 billion ($4.1 billion). Non-interest income from credit cards was RMB9.6 billion ($1.5 billion) in 2015 compared with RMB7.8 billion ($1.2 billion) in 2013. With such a large increase in total credit card loans, the non-performing loan ratio of the credit cards business reached 1.37%, up by 0.43 percentage point in 2014 but still was under control (Table 1).

Credit cards becoming a driving source for retail profits

Changes in strategy have largely been responsible for the bank’s strong retail performance especially given the deteriorating economic conditions, interest rate cuts and financial disintermediation. The bank has faced intense competition for customers as new financial services models and organizations like mobile banking, internet banking, P2P lending have emerged. It has achieved an outstanding competitive advantage over its peers by detecting spending needs of customers and designing products well ahead of its competitors.

To boost the bank’s internet finance businesses, strategies involving the development mobile phonebased retail business services to raise the e-bank channel replacement ratio, and improved credit card services have been adopted. The bank has developed a “flow, platform, data” overall layout and keeps broadening its electronic banking channels using the idea of a “light” operating platform. To further strengthen the link between internet and mobile banking, the bank released CMB Life 5.0 for over 20 million users making a successful transformation from a simple payment tool to an open, multi-functional platform. The bank created an “online application and offline verification” process to enhance the efficiency of cross-selling across the retail banking segment.

For its credit card business, CMB undertook initiatives to build multi-dimensional credit card products targeted at different customer segments. For example, they introduced co-branded credit cards with popular internet online games and social media companies, offered Diamond Credit Cards for high-end customers and AllCurrencies MasterCard for those who travel overseas. All of these strategies have contributed to boosting credit card lending and optimising retail lending, thus improving the bank’s balance sheet position for retail banking.

China CITIC Bank

2015 was the second year of the full implementation of China CITIC Bank’s retail transformation. The bank was one of the most improved banks in China providing better customer experience, sustainable earnings growth and solid branding in retail banking. Retail customers increased to 57.9 million and retail deposits amounted to RMB465.5 billion ($71.8 billion) during the year.

China CITIC Bank has a detailed integrated marketing strategy for grouping its customers. The bank has focused on brand building in terms of product allocation, marketing. China CITIC Bank has deep insight into its customer base and puts emphasis on four customer segments; female customers, middle and old age customers, young whitecollar workers and overseas customers.

There has been a dramatic increase in China’s upper middle class whose affluent families are targeted as customers by the commercial banks. China CITIC bank has developed a unique offering to these customers by developing a range of products and services for customers needing international banking services; the bank was quick to identify the growing tendency of Chinese parents to send their children overseas at a young age.

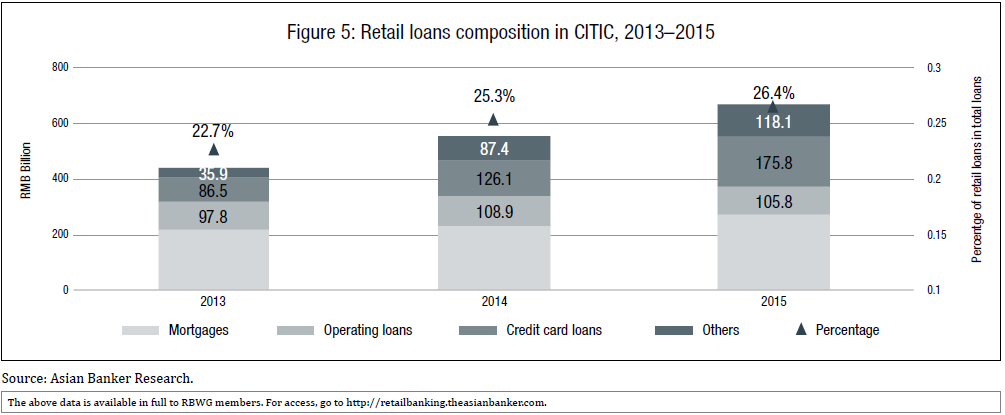

In 2015, the balance of retail loans was RMB668.6 billion ($103.2 billion), an increase over the previous year’s RMB114.1 billion ($17.6 billion) representing a 20.6 percent growth rate (Figure 5). Retail loans grew faster than corporate loans and made up 26.4 percent of total loans. An analysis of the composition of retail loans at the bank revealed that only credit card loans increased as a percentage of total retail loans during the last three years, while the weighting of mortgages and operating loans fluctuated. To promote new business growth, the bank has proactively created new products covering auto loans, internet credit loans and secured loans. Aimed at the property market, the bank designed comprehensive mortgage loan packages to open up both consumer and commercial business opportunities and took risk control measures to increase the quantity of business it could handle. To support this, it improved its systems, building in automation and developing a new online retail credit management system.

Only credit card loans obtained an increasing percentage in total retail loans in the last three years

The bank integrated its search and online capabilities, and embraced big data thereby actively enhancing its marketing and branding capabilities. This has enabled the bank to introduce the first family credit card account in China, breaking the traditional business operating model of separate accounts and credit cards for individuals. The account enables families to transfer points and benefits among family members under a joint account called “Account +”. This is a new model in China introducing the idea that accounts and cards can be linked, even amongst family members.

The bank currently operates or is an active partner in nine mobile Internet platforms. Logins to its own platform reached 3.63 million and the cumulative overall social platform user logins exceeded 30 million in 2015. The bank became the first financial institution to break the 10 million user barrier on mobile QQ and Wechat platforms. During 2015, the bank continued to manage credit card services with Baidu, Alibaba, Tencent, Jingdong and other partners, carrying out a series of internet and mobile banking innovations and further consolidating its leading position within the industry for combining credit card services with internet finance. By implementing these innovations and strategies, revenues from credit cards at CITIC bank were RMB19.48 billion ($3 billion) representing a 46.6% growth rate, representing a 15.6% of total operating income for the bank.

.png)

.webp)