- A 5% increase in the household debt to gross domestic production (GDP) ratio over a three-year period is expected to lead to a 1.25% drop in real GDP growth three years ahead

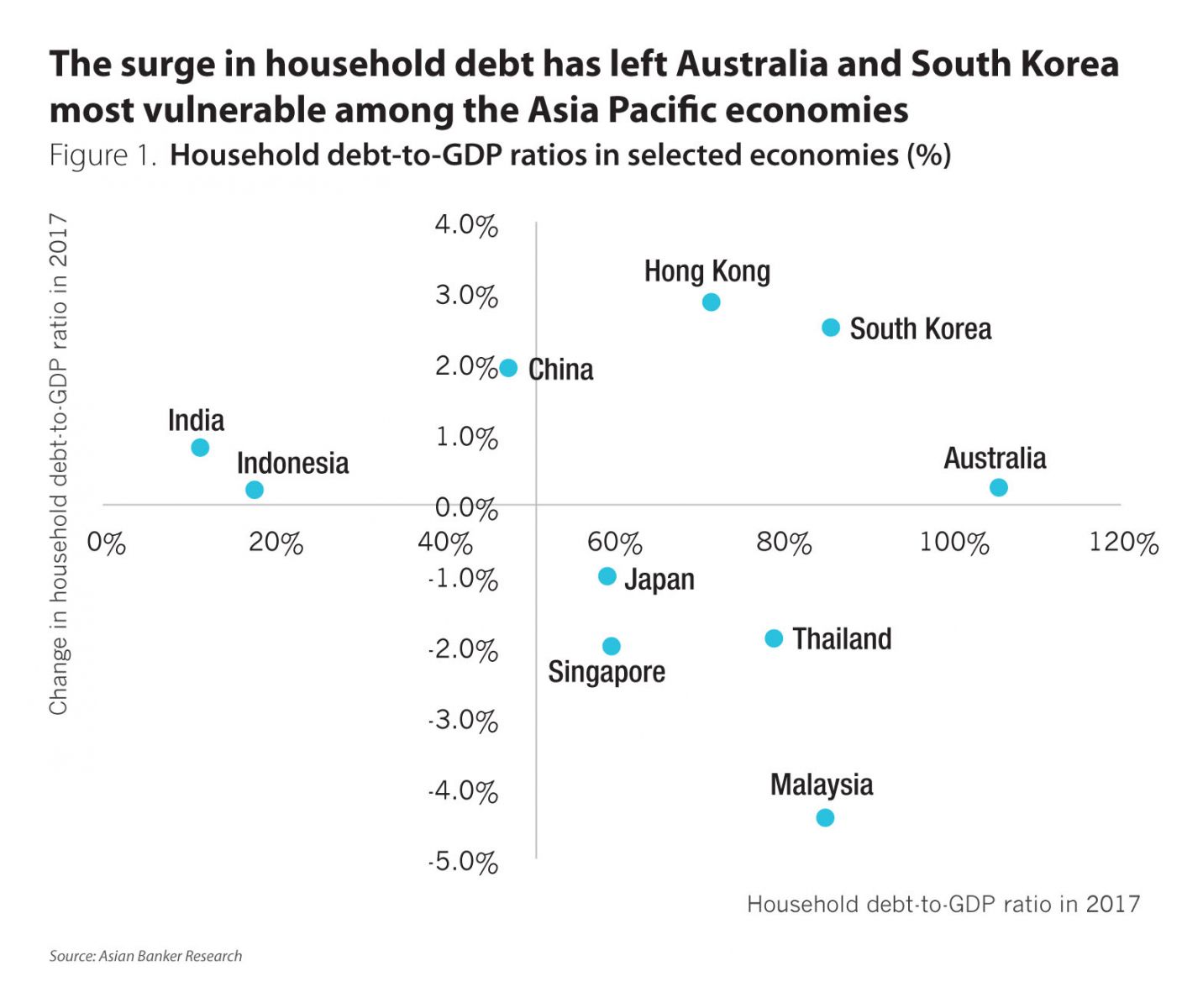

- Household debt-to-GDP ratios in Australia and South Korea are not only much higher than other economies, but also rising, which places these two countries at risk

- More attention has been paid to China, as the indebtedness of Chinese households has been growing rapidly, although it is still at relatively low levels of GDP

Many economies have experienced a dramatic increase in household debt over the past decade, leaving them vulnerable to future shocks. Household debt comprises debt incurred by resident households of the economy, and mortgage loans account for the bulk of household debt. Several international organisations and central banks in many economies have warned against the risks to economic growth and financial stability of the massive household debt. The surge in household indebtedness has an impact on households’ ability to deal with the unanticipated deterioration in market conditions or household economic circumstances, such as lower housing prices, higher interest rates or lower income.

While an increase in household debt might boost economic growth in the short term, the positive effects are reversed in three to five years, according to a report from the International Monetary Fund (IMF). The IMF said that a 5% increase in the household debt to gross domestic production (GDP) ratio over a three-year period is expected to lead to a 1.25% drop in real GDP growth three years ahead.

The household debt-to-GDP ratios in Australia and South Korea are not only much higher than other economies, but also rising, which places these two countries at risk (Figure 1). Countries like Malaysia and Thailand has seen a decline in their household debt as a share of GDP, thanks to the measures taken to curb the build-up of household debt. However, their household debt-to- GDP ratios are still among the highest in the region. On average, advanced economies tend to have higher ratios of household debt to GDP than emerging markets. The levels of household debt in India, Indonesia and China are the lowest among these ten economies. More attention has been paid to China, as the indebtedness of Chinese households has been growing rapidly, although it is still at relatively low levels of GDP.

Australia

The record high household debt has made Australia’s economy less resilient to future shocks, and also poses risks to the stability of the banking system. However, Australia has less external financing, floating exchange rates and highly developed financial system, which will help reduce risks associated with rising household debt.

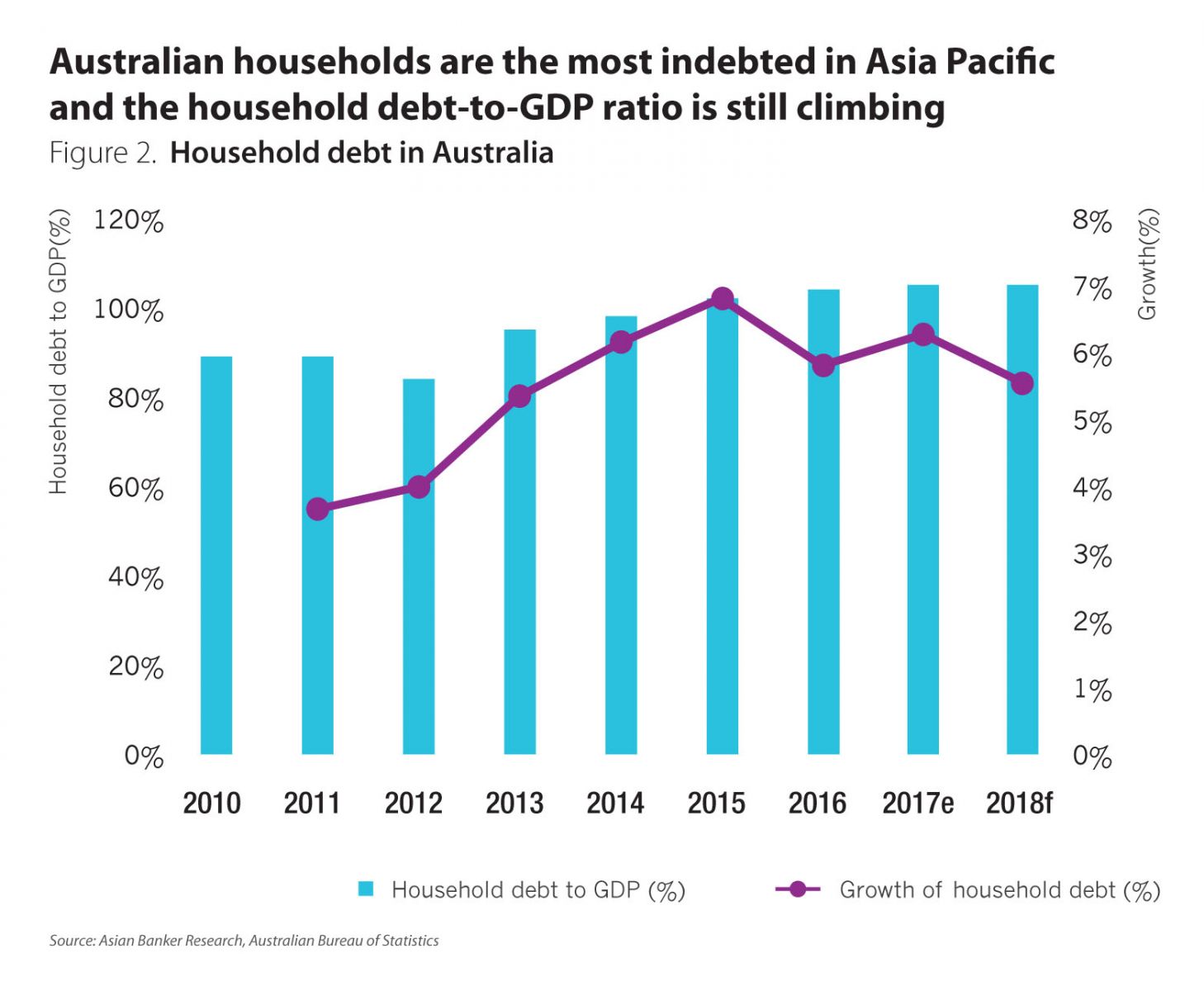

The households’ ability to deal with the unexpected macroeconomic shocks is negatively affected, especially when Australia’s debt-to-income ratio (Figure 2) is also among the highest in the world. According to the Survey of Income and Housing released by the Australian Bureau of Statistics, 29% of the households were classed as “over-indebted” in terms of their debt-to-income ratio or debt-to-asset ratio in 2015-2016, up from 21% in 2003- 2004. In addition, mortgage loans dominate household debt and adjustable-rate mortgages are most common in Australia. Owner-occupied mortgages and loans for investment homes accounted for 56.3% and 36.5% of the total household debt in the country, respectively.

The Reserve Bank of Australia (RBA) left the cash rate on hold at a record-low1.5%, due to rising levels of household debt and persistently weak wages growth. If RBA raises interest rates, highly indebted households could struggle to repay their debts and reduce their spending. Thus, rising household debt also makes it harder for RBA to control monetary policy.

Main driving factors of the heavy household debt are low interest rates, tax settings around housing investment and housing boom. The negative gearing and the capital gains tax concessions enable investors to deduct any losses associated with the investment from their salary and wage income, which encourages leveraged and speculative real estate investment. Housing prices surged, due to the demand from overseas investor and strong population growth. In addition, intensified competition among Australian lenders seems to have led to a relaxation of loan standards.

Australian financial regulators have taken a series of measures to cool down red-hot property market and curb ballooning household debt. For example, foreign investors are banned from buying existing properties. Meanwhile, the increase in house building and transport investment put further downward pressure on prices and rental levels. A near-term crash in the housing market is not expected. Sydney housing market has begun to soften and Melbourne housing market is showing consistent signs of cooling. However, many banks still offer owner-occupied mortgage loan borrowers record low rates, which remains a cause for concern.

Malaysia

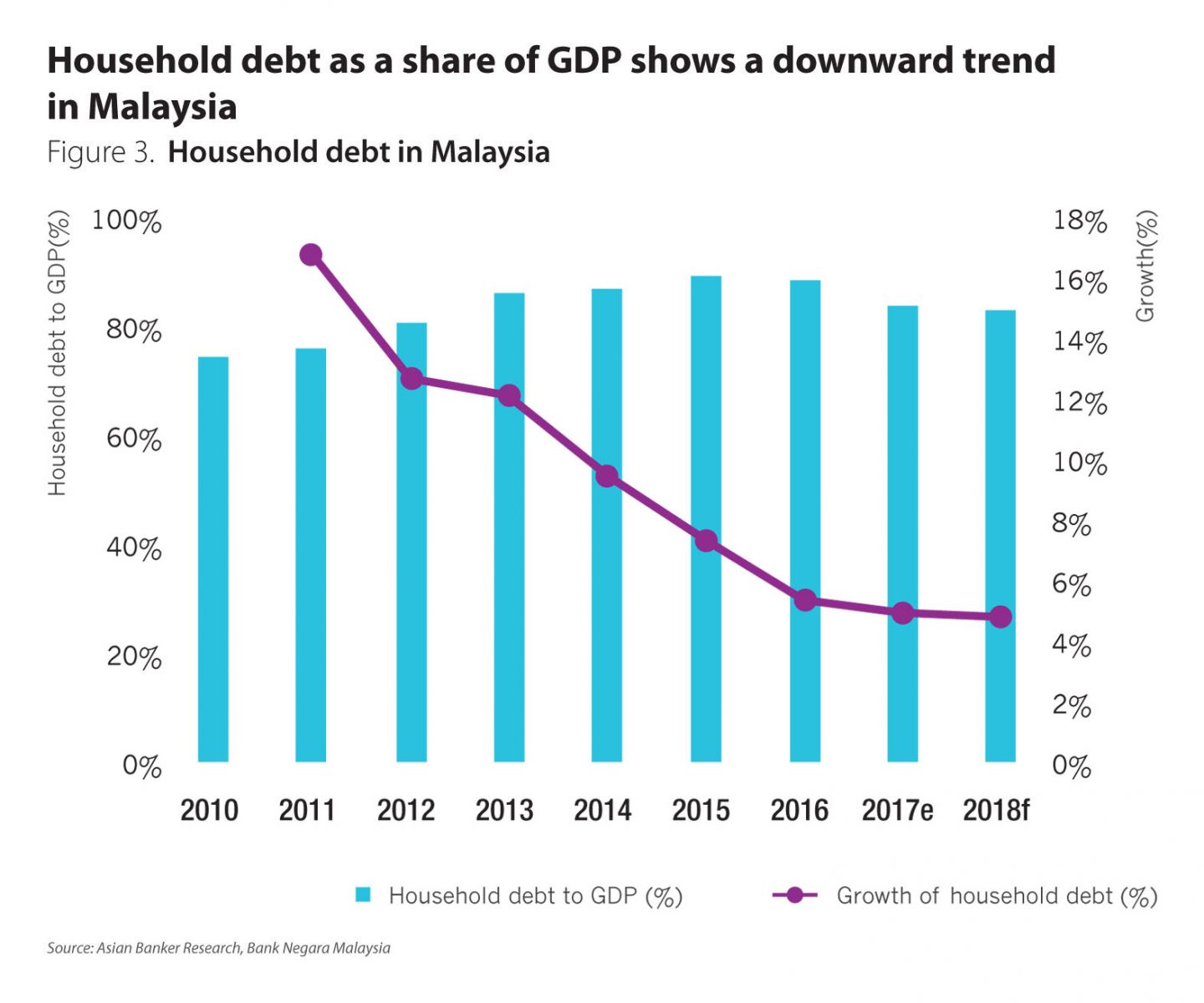

As a percentage to GDP, the level of debt borne by Malaysian households has eased gradually to 84.6% as of September 2017 from 89.1% in 2015 (Figure 3). This is because the GDP growth has outpaced the growth of household debt. The household debt in Malaysia has risen at a slower pace during the past few years. Malaysia’s economic growth has accelerated, mainly supported by stronger private consumption, better labour market conditions and improved external sector.

The household debt in Malaysia is expected to remain at prudent levels, owing to macro-prudential measures taken by the government to contain household debt growth and the improved labour market conditions. Most households have the adequate ability to repay their debts. Malaysia’s central bank said that the majority of new households have prudent debt service ratios of below 60%, and the share of borrowings by vulnerable debtors was 20.6% of all household debt as of September 2017, down from 21.9% in 2016.

Despite the slight decline, Malaysia’s household debt to GDP ratio remains one of highest in the region. Households earning below $761.13 (MYR3,000) per month in urban areas are still struggling to repay their debts amid rising living costs. More needs to be done to slow down household debt further, such as better regulation of the housing market to eliminate speculation and more policies to encourage repayment.

South Korea

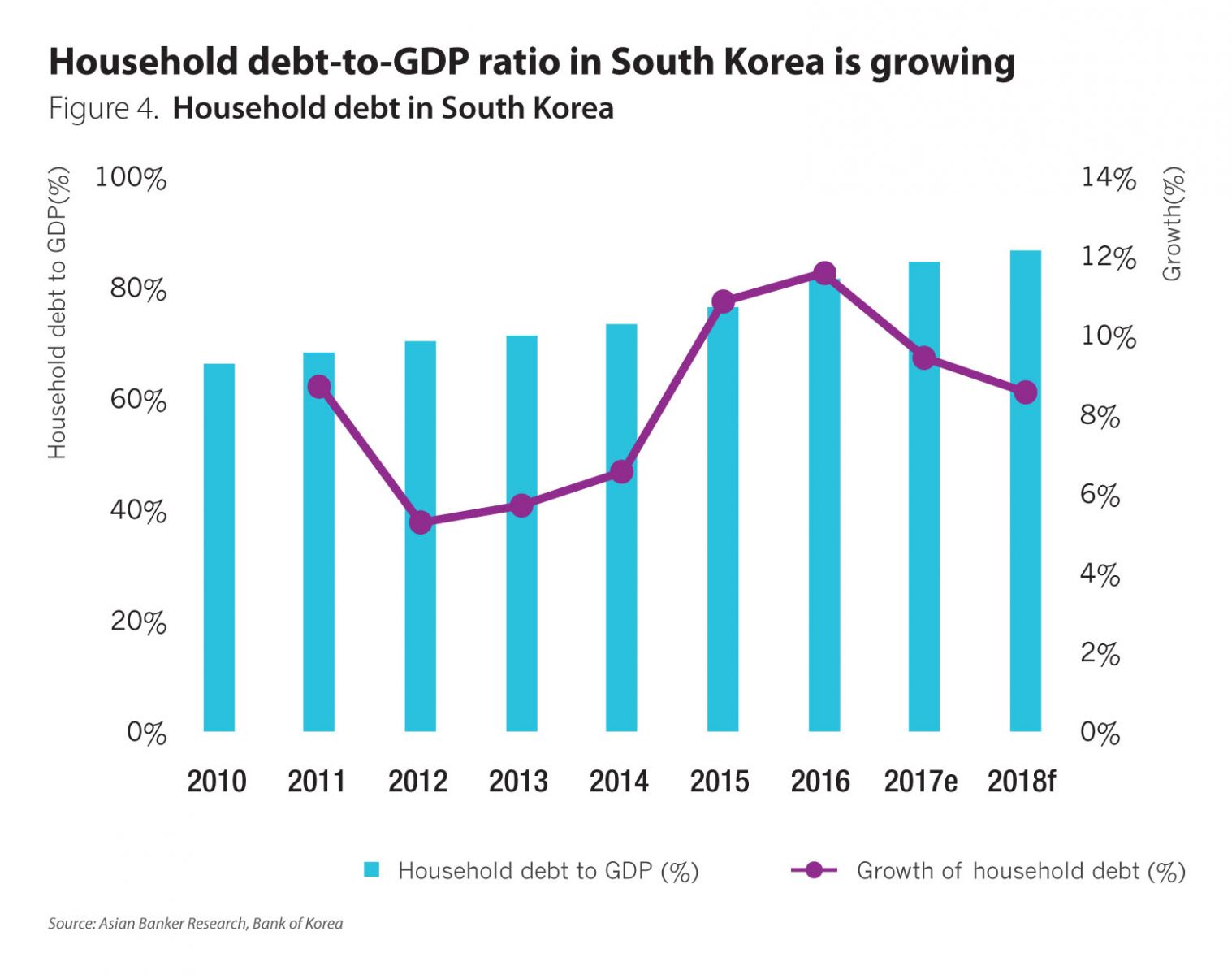

The South Korean household debt reached around $1.4 trillion as of the end of 2017 (Figure 4), equal to about 85% of the country’s nominal GDP. Although several measures have been taken to tackle the household debt problem in South Korea, the household debt-to-GDP ratio continues to rise. The heavy household debt in South Korea is unlikely to cause a systemic risk immediately, as the ratio of household loans classified as substandard or below is still at a low level and the quality of household debt has improved. However, ballooning household debt holds back private consumption and poses a potentially serious risk to the economy.

The household debt expanded by more than 10% annually in 2015 and 2016, up from around 6% between 2012 and 2014, largely driven by low interest rate and the relaxation of mortgage loan requirements in 2014. The South Korean government eased up on loan-to-value ratio and debt-to-income ratio to help the sluggish domestic economy, which ended up in more mortgage borrowing and speculations and soaring household debt.

The government tightened mortgage rules further in 2017 in a bid to cool down the real estate market and curb soaring household debt. The new mortgage rules make it harder for owners of multiple homes to take out mortgage loans. For example, loan limits for borrowers applying for mortgages on second homes have been tightened starting 2018, with lenders required to include principal balance of the borrowers’ existing debt for their credit analysis.

The Bank of Korea (BOK) kept the base rate unchanged at a record low of 1.25% since June 2016. It is widely expected that the BOK will tighten its monetary policy in the coming months as the economy improves. If the BOK raises the benchmark interest rate, debt repayment burdens for vulnerable homes will increase and consumer spending will decrease.

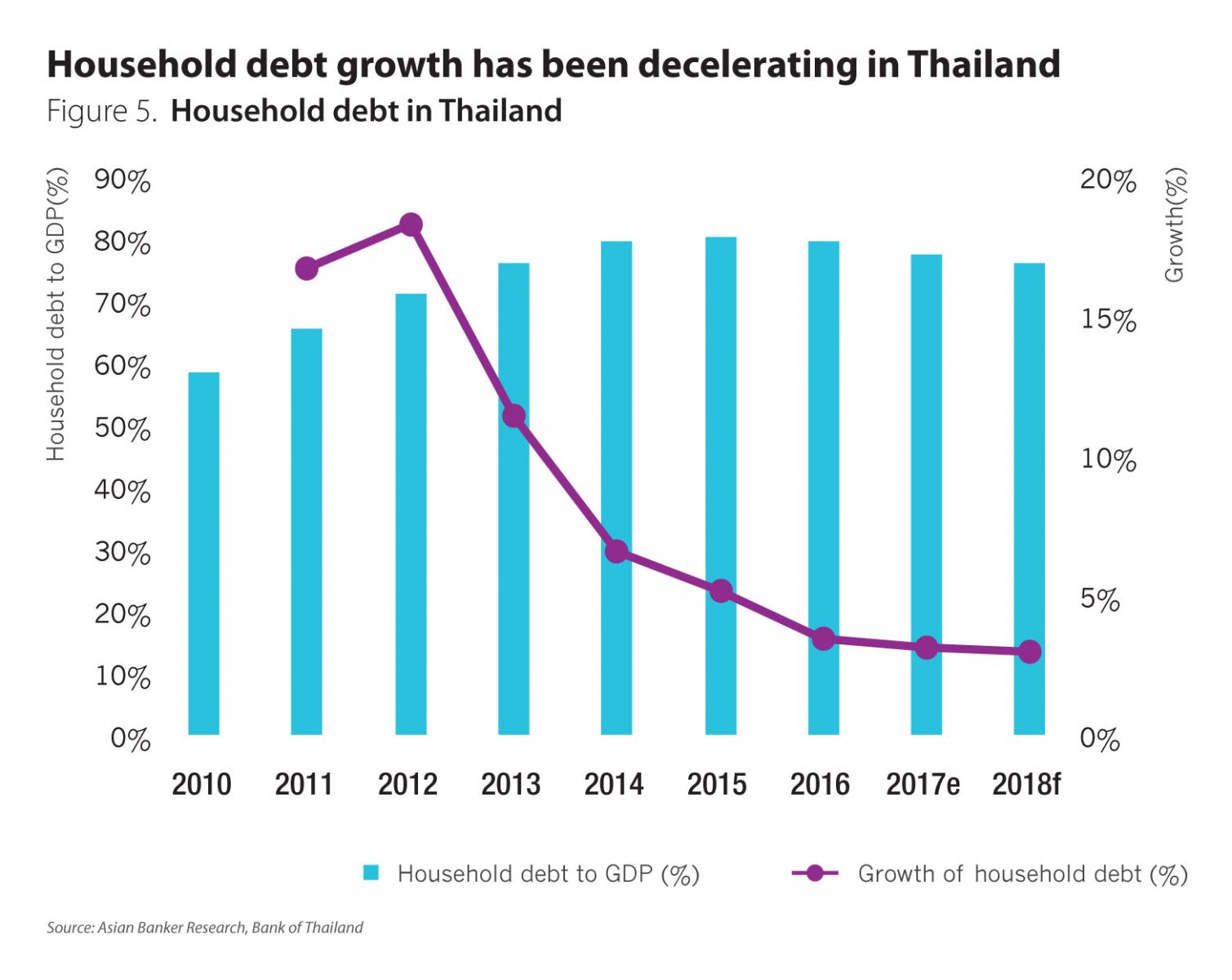

Thailand

The household debt as a share of GDP in Thailand fell gradually from a record high of 81.2% at the end of 2015 (Figure 5), mainly owing to strong economic growth and tightened regulations regarding unsecured consumer lending. The household debt in Thailand continues to grow in real terms, albeit at a slower pace. The ratio of household debt to GDP stood at 78.3% at the end of September 2017, which was still among the highest in the region.

Personal loans taken out by young newly-employed workers is one of the key reasons for the high household debt in the country. Thai households have better access to unsecured personal loans than other categories of retail lending. Young first jobbers are the major new borrowers of personal loans, but they tend to default more.

Due to the concerns over household debt burden and rising bad debts, the Bank of Thailand has tightened controls on credit cards and unsecured personal loans. Under the new rules effective from 1 September 2017, credit card interest rate is lowered from a maximum of 20% to 18% and only individuals earning at least $1,492 (THB50,000) a month can get a maximum credit limit of five times their monthly salary. However, it applies only to new customers, and thus the effect is not expected to be harsh.

The Bank of Thailand has left its benchmark interest rate unchanged at 1.5% for more than two years in an effort to aid economic recovery. High household debt will keep low-income earners in a vulnerable position and continue to weigh on private consumption. Meanwhile, loan quality pressure persists, partially due to the surge in lending to vulnerable households, which will remain a challenge to stability of Thai financial system.

Thanks to the steps taken to battle high household debt, some economies have seen some signs of the improvements. However, concerns persist. The high household indebtedness has already led to increasing debt repayment burdens and affected private consumption and asset quality of banks in some countries. Going forward, more needs to be done to reduce any potential risk to the financial system and economic growth.

.png)

.webp)